Part 1: What Is the Repo Rate and How Does the RBI Use It?

Defining the Repo Rate

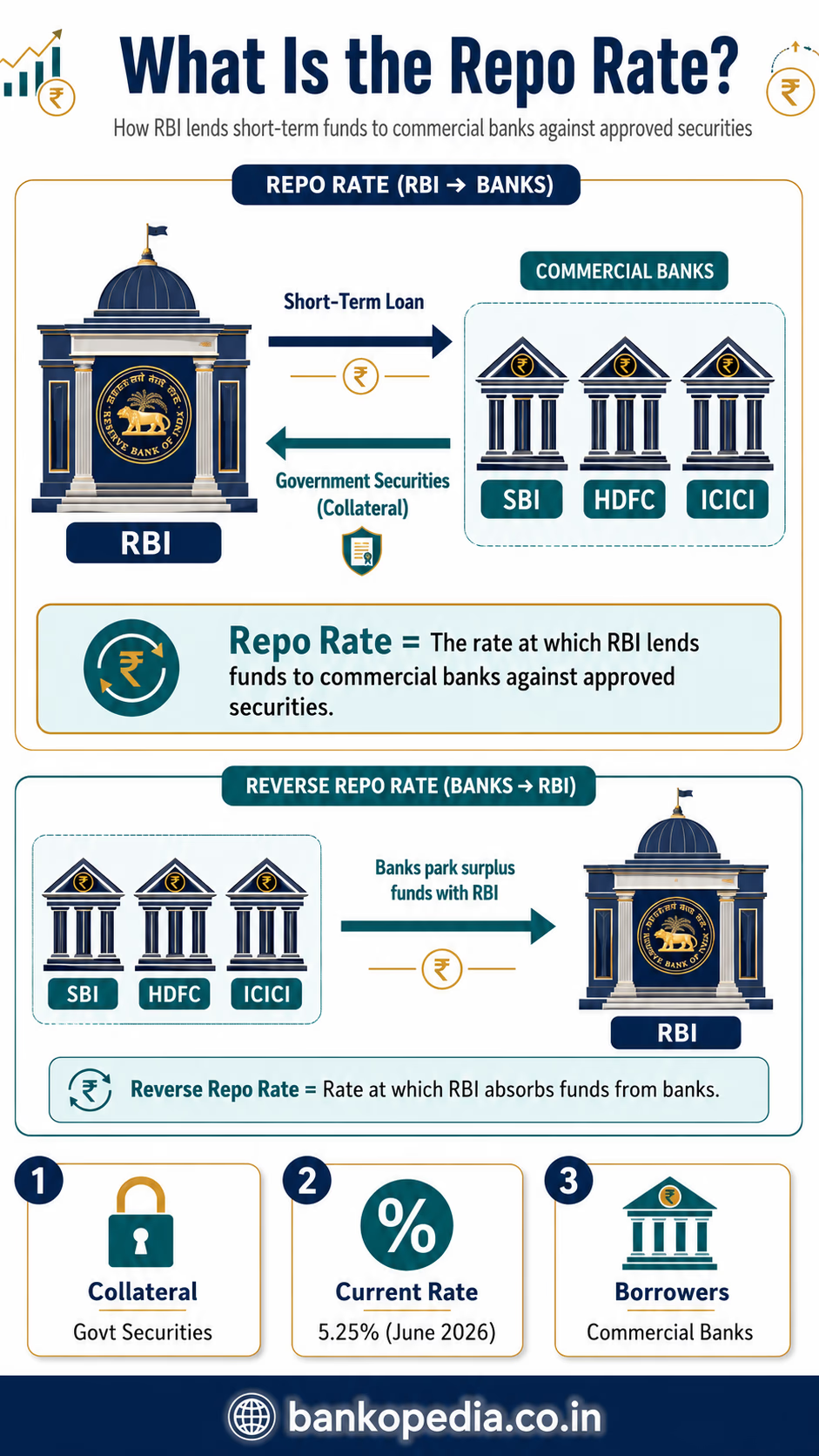

The "repo rate"—short for repurchase agreement rate—is the foundational interest rate at which the Reserve Bank of India lends short-term funds to commercial banks (like SBI, HDFC, ICICI, etc.) against approved collateral, typically government securities.

In simpler terms, commercial banks are businesses. Like any business, they sometimes face a temporary shortfall of cash or liquidity mismatches. When banks need immediate liquidity to meet their daily regulatory requirements or to fund sudden credit demands, they borrow money from the RBI. The repo rate is the cost of that borrowing.

Conversely, the reverse repo rate is the interest rate that banks earn when they have surplus funds and park them with the RBI. By adjusting these two rates, the RBI makes borrowing either more expensive or cheaper for banks, which directly influences how much banks charge you for loans or pay you for deposits.

The Dual Objectives: Inflation vs. Growth

The RBI uses the repo rate as its primary monetary policy instrument to achieve two broad, often conflicting, objectives:

Controlling Inflation: Keeping the rising prices of everyday goods and services in check so that the purchasing power of the Indian Rupee does not rapidly erode.

Supporting Economic Growth: Ensuring that borrowing costs are low enough to encourage businesses to expand, hire more workers, and produce more goods, while simultaneously encouraging consumers to spend.

These two goals typically pull in opposite directions. This dynamic trade-off is the core reason the MPC’s bi-monthly decisions are watched so intensely by economists, banking professionals, and retail investors. When inflation runs hot, the RBI raises the repo rate. When the economy is sluggish and inflation is tamed, the RBI cuts the repo rate.

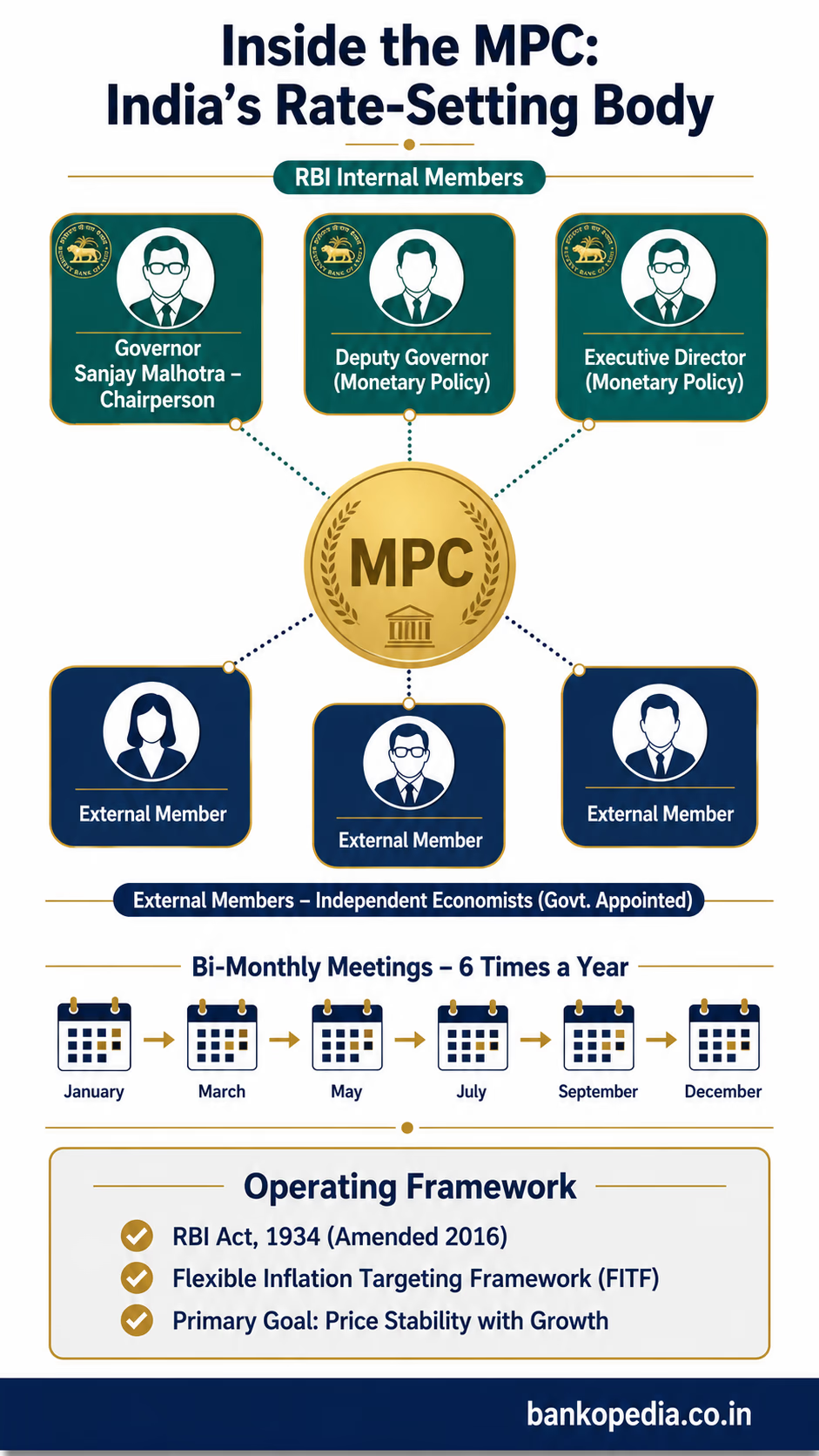

The Monetary Policy Committee (MPC) and Its Mandate

To institutionalize this process, the MPC was constituted under the RBI Act, 1934 (as amended in 2016). The committee comprises six members:

Three internal members from the RBI, including the Governor who acts as the Chairperson (currently Governor Sanjay Malhotra).

Three external members, who are independent economists and experts appointed by the Government of India.

The MPC operates under a Flexible Inflation Targeting Framework (FITF). Its primary mandate is to maintain Consumer Price Index (CPI) retail inflation at a target of 4%, with a permissible tolerance band of ±2% (meaning inflation can technically fluctuate between 2% and 6% without triggering a statutory failure). The committee meets at least four times a year, though typically it meets bi-monthly (every two months).

When inflation spikes above the 6% upper tolerance band, the MPC is essentially forced to hike the repo rate. This makes borrowing more expensive, which cools down consumer demand and business expansion, eventually pulling prices down. Conversely, when growth slows or inflation is comfortably near the 4% target, the MPC may cut rates to stimulate lending and consumption. A "pause"—as we are seeing in mid-2026—signals that the committee is carefully watching incoming macroeconomic data before committing to a definitive tightening or easing cycle.

The repo rate does not operate in a vacuum. It sits squarely at the center of the Liquidity Adjustment Facility (LAF) corridor. As of June 2026, the key rates in this corridor are:

Standing Deposit Facility (SDF) Rate (5.00%): The lower bound of the corridor. This is the rate at which the RBI absorbs uncollateralized excess liquidity from banks. It effectively replaced the fixed reverse repo rate as the floor of the LAF corridor.

Repo Rate (5.25%): The anchor policy rate.

Marginal Standing Facility (MSF) Rate (5.50%): The upper bound. This is a penal rate at which banks can borrow overnight funds from the RBI against government securities when liquidity dries up completely.

This narrow 50-basis-point corridor (from 5.00% to 5.50%) ensures that short-term money market rates remain tightly anchored close to the repo rate, giving the RBI immense and precise control over systemic liquidity and the overarching cost of credit in the Indian banking system.

Part 2: How a Repo Rate Change Flows Down to Your Bank Loan EMI

This is where the abstract world of macroeconomics intersects with the concrete reality of your personal budget. The transmission mechanism—the chain of events linking an RBI rate decision to your monthly Equated Monthly Installment (EMI)—is intricate but profoundly impactful.

The EBLR Regime: Faster and More Transparent Transmission

Prior to October 2019, monetary transmission in India was notoriously sluggish. Banks priced their retail loans based on opaque internal benchmarks like the Base Rate or the Marginal Cost of Funds-based Lending Rate (MCLR). When the RBI cut the repo rate, banks were notoriously slow and reluctant to pass on the benefits to borrowers, often citing that their own cost of deposits had not yet fallen. However, when the RBI hiked rates, banks were remarkably quick to increase EMIs.

To fix this asymmetric transmission, the RBI introduced a sweeping reform. It mandated that all new floating-rate retail loans (home loans, auto loans, personal loans) and MSME loans disbursed after October 1, 2019, must be linked to an External Benchmark Lending Rate (EBLR). Banks were given a choice of external benchmarks, but almost all major banks chose the RBI’s repo rate, leading to the creation of the Repo-Linked Lending Rate (RLLR).

Under the RLLR regime, transmission is mechanical, transparent, and almost instantaneous. If the MPC announces a 25 basis point (0.25%) cut in the repo rate on a Friday, your bank's RLLR will automatically fall by exactly 25 basis points by the start of the next reset period (usually the 1st of the following month).

Fixed vs. Floating Rate Loans

Understanding the nature of your loan agreement is crucial to knowing how the repo rate will affect you.

Fixed-Rate Loans: These loans lock in a specific interest rate at the time of disbursement. Personal loans and vehicle loans frequently fall into this category. Borrowers with fixed-rate loans are completely insulated from MPC decisions. Whether the repo rate crashes to 3% or skyrockets to 8%, their EMI remains exactly the same until the end of the loan tenure.

Floating-Rate Loans: Most home loans and large business loans in India are floating-rate. These borrowers are fully exposed to rate movements. As the RLLR fluctuates, so does the cost of their loan.

The Mathematics of Transmission: Rate Hikes vs. Rate Cuts

How do banks actually adjust your loan when the repo rate changes? They typically manipulate either the tenure of the loan or the EMI amount.

The Rate Hike Scenario: When the repo rate increases, the RLLR increases. To prevent immediate payment shock to the borrower, banks typically keep the EMI amount identical but extend the remaining tenure of the loan. For example, a 20-year home loan might be quietly extended to 22 years. However, if the borrower is older and the extended tenure crosses their retirement age (the bank's tenure ceiling), the bank has no choice but to forcefully increase the monthly EMI amount.

The Rate Cut Scenario: When the repo rate falls, the RLLR decreases. The bank will typically reduce the loan tenure while keeping the EMI the same, allowing the borrower to become debt-free faster. Alternatively, borrowers can actively request their bank to lower their monthly EMI amount instead, freeing up cash flow for daily expenses.

The Rate Pause Scenario: When the MPC holds the rate steady—as seen currently in mid-2026 at 5.25%—EMIs for existing floating-rate borrowers remain unchanged. This provides much-needed budget certainty for households.

Example Calculation

Let’s quantify this impact using a hypothetical standard home loan.

Principal Outstanding: ₹50 Lakh

Remaining Tenure: 20 Years (240 months)

Initial Interest Rate: 8.50%

If the RBI cuts the repo rate by 50 basis points (0.50%), the new interest rate becomes 8.00%.

Parameter | At 8.50% Interest Rate | At 8.00% Interest Rate | Savings / Impact |

Monthly EMI | ₹43,391 | ₹41,822 | ₹1,569 saved per month |

Total Interest Paid | ₹54,13,879 | ₹50,37,281 | ₹3,76,598 saved over tenure |

As demonstrated, even a fractional shift in the repo rate translates to hundreds of thousands of rupees saved or lost over the life of a standard Indian home loan.

Processing Fees, Spreads, and Credit Risk

It is vital to understand that banks do not lend money at the absolute repo rate. Your final lending rate is constructed as:

Effective Interest Rate = Repo Rate + Bank’s Operating Margin + Credit Risk Premium (Spread)

While the repo rate component moves up and down symmetrically with RBI announcements, the spread is permanently fixed on the day your loan is sanctioned. If you have a poor CIBIL credit score (e.g., 650), your bank might charge a spread of 3.50%. If the repo rate is 5.25%, your final rate is 8.75%. If your neighbor has an excellent CIBIL score (e.g., 800), their spread might only be 2.00%, giving them a final rate of 7.25%.

The MCLR Overhang and Legacy Loans

What about older loans? A significant stock of loans originated between 2016 and 2019 are still stuck on the older MCLR framework. Under MCLR, the interest rate is reset only periodically (usually once a year). If the RBI cuts rates in January, an MCLR borrower whose reset date is in November will not see any benefit for 10 months. Furthermore, MCLR transmission is often partial, as it depends on the bank's internal cost of funds rather than the pure external repo rate. The RBI consistently urges borrowers on older Base Rate or MCLR regimes to pay a small switching fee and migrate their loans to the more transparent EBLR/RLLR regime.

Part 3: Impact on Fixed Deposits, Savings Accounts, and Debt Mutual Funds

The repo rate’s influence extends far beyond borrowers. It is the invisible hand that shapes the returns on a vast array of savings and investment instruments, making it deeply relevant to depositors, retirees, and capital market participants.

Fixed Deposits (FDs): The Most Direct Beneficiary

Fixed Deposits remain the bedrock of savings for the Indian middle class, particularly senior citizens. The relationship between the repo rate and FD rates is highly correlated, though not instantly mechanical.

When Rates Rise: Borrowing from the RBI becomes expensive for commercial banks. To raise capital to lend out, banks are incentivized to turn to retail depositors. They compete for your money by aggressively raising FD interest rates. During the aggressive tightening cycle of 2022-2023, peak FD rates surged from around 5.00% to over 7.50%, a massive boon for conservative savers.

When Rates Fall: Banks can borrow cheaply from the RBI or the money markets. They no longer desperately need retail deposits, so they systematically slash the interest rates offered on new FDs.

FD Laddering Strategy: Smart investors use a technique called "laddering." Instead of locking all their money into one 5-year FD, they split it into multiple FDs maturing at different intervals (e.g., 1 year, 2 years, 3 years). This ensures liquidity and allows them to continuously reinvest at prevailing interest rates, averaging out the impact of repo rate volatility over time.

Savings Accounts: Muted but Real Impact

The RBI fully deregulated savings account interest rates in 2011, meaning banks are entirely free to set their own rates. In practice, the giant legacy banks (like SBI or HDFC) maintain their basic savings rates stubbornly low, typically in the 2.70%–3.50% range, regardless of what the MPC does. However, aggressively expanding smaller banks, Small Finance Banks (SFBs), and Neo-banks often offer 6.00% to 7.00% on savings accounts to aggressively capture market share. While savings rates do eventually trend up or down with the repo rate, they are highly "sticky" and far less responsive than FD rates or loan EMIs.

Debt Mutual Funds: An Inverse Relationship

For investors participating in the capital markets through Debt Mutual Funds—regulated by SEBI—understanding the repo rate is absolutely critical to avoid destroying capital. There is a universal, fundamental law of finance that governs this space: Bond prices and interest rates share an inverse relationship.

When the Repo Rate Rises: The government and corporations start issuing new bonds offering higher interest yields. Consequently, the older bonds sitting in a mutual fund's portfolio (which pay a lower interest rate) suddenly look unattractive to buyers. Their market price drops. This drop in bond prices leads to a fall in the Net Asset Value (NAV) of the debt mutual fund, causing temporary capital erosion for the investor.

When the Repo Rate Falls: The exact opposite happens. New bonds offer terrible yields. Suddenly, the older, high-yielding bonds currently held by the mutual fund become highly sought after. Their market price surges, rapidly pushing up the NAV of the fund and delivering windfall capital gains to the investor.

To manage this risk, SEBI categorizes debt funds by "duration":

Long-Duration and Gilt Funds: Highly sensitive to interest rate changes. If you are deeply convinced the RBI is about to aggressively cut rates, these funds will deliver massive returns. If you are wrong and the RBI hikes rates, these funds will suffer severe losses.

Liquid and Short-Duration Funds: Invest in very short-term paper (like 91-day Treasury Bills). They are relatively immune to repo rate shocks and provide stable, predictable returns regardless of MPC decisions.

Dynamic Bond Funds: The fund manager actively shifts the portfolio between short-term and long-term bonds based on their proprietary reading of the RBI's future moves.

Part 4: Historical Repo Rate Changes and Their Effect on the Indian Economy

A review of the RBI’s rate history over the past two decades reveals a clear pattern: monetary policy does not exist in isolation. It is deeply intertwined with global crises, domestic food shocks, capital flows, and geopolitical warfare. Tracking the rate history gives us a masterclass in macroeconomic management.

1. The Post-GFC Easing Cycle (2008–2010)

When the Global Financial Crisis (GFC) triggered the collapse of Lehman Brothers in 2008, global credit markets froze. To protect the Indian economy from a catastrophic recession, the RBI embarked on an aggressive, emergency rate-cutting cycle. The repo rate was slashed dramatically from 9.00% in October 2008 to 4.75% by April 2009. Combined with government fiscal stimulus, this flood of cheap money kept India's GDP growth above 6%, even as the US and Europe contracted. The cheap credit fueled an massive boom in real estate, corporate infrastructure, and consumer lending.

2. The Inflation-Fighting Cycle (2010–2014)

The massive stimulus of 2008 came at a cost: skyrocketing inflation. Driven by global oil prices spiking above $100 a barrel, domestic food shortages, and excessive government spending, India faced a debilitating inflation crisis. Prices were rising by double digits. To break the back of inflation, the RBI entered a painful tightening cycle, hiking the repo rate all the way up to 8.50% by October 2011 and holding it high for years. This crushed inflation, but it also induced a severe credit squeeze, stalling infrastructure projects, devastating MSMEs, and creating the initial wave of Non-Performing Assets (NPAs) in the banking sector.

3. The Rajan-Era Reforms and Gradual Easing (2014–2019)

Under the leadership of Governor Raghuram Rajan, the RBI formally adopted the modern Flexible Inflation Targeting framework. With inflation finally structurally subdued and global oil prices collapsing in 2014, the RBI began a prolonged, highly calibrated easing cycle. Between January 2015 and October 2019, the repo rate was methodically reduced from 8.00% down to 5.15%. This era was characterized by a massive formalization of credit, the introduction of the MCLR/EBLR frameworks, and a surge in retail borrowing.

4. The COVID-19 Emergency Cuts (2020)

The outbreak of the COVID-19 pandemic and the ensuing national lockdown represented an unprecedented existential threat to the economy. In response, the RBI executed a breathtaking rescue operation. In off-cycle meetings, the repo rate was slashed by an incredible 115 basis points, dragging the rate down to a historic, all-time low of 4.00% by May 2020. Alongside a moratorium on EMI payments and massive liquidity injections, these rock-bottom rates prevented a total collapse of the banking system. The hyper-cheap liquidity triggered a massive bull run in the Indian stock markets and fueled a historic boom in housing sales.

5. The Inflation Shock and Aggressive Tightening (2022–2023)

The post-pandemic recovery was violently interrupted by the outbreak of the Russia-Ukraine war in early 2022. Global supply chains ruptured, and commodity prices—particularly crude oil, wheat, and fertilizer—exploded. Indian retail inflation breached the RBI's 6% upper tolerance limit. The RBI pivoted aggressively. In one of the fastest tightening cycles in history, the MPC hiked the repo rate by 250 basis points across six consecutive meetings between May 2022 and February 2023, driving the rate up to 6.50%. Millions of Indian homeowners suddenly found their loan tenures extending by 5 to 7 years, causing widespread distress but successfully wrestling headline inflation back into the safe zone.

6. The Post-Peak Easing to 5.25% (2024-2025)

As the shockwaves of the Ukraine conflict subsided and global supply chains normalized through 2024, domestic inflation steadily retreated. Recognizing that a 6.50% rate was unnecessarily punishing an economy that needed to grow, the RBI initiated a gradual easing cycle. Through a series of measured cuts spanning late 2024 and 2025, the central bank successfully guided the repo rate down from its 6.50% peak to 5.25%, providing massive relief to borrowers while keeping the rupee stable.

Part 5: The Current Macroeconomic Reality (June 2026 Context)

Fast forward to June 2026, and the macroeconomic landscape has shifted yet again, forcing the RBI to recalibrate its approach in the face of immense external volatility.

The June 5, 2026 MPC Decision

In its most recent bi-monthly meeting concluded on June 5, 2026, the Monetary Policy Committee, led by Governor Sanjay Malhotra, voted unanimously to keep the benchmark repo rate unchanged at 5.25%. Crucially, the MPC retained its official policy stance as "Neutral."

A "neutral" stance is highly significant in central banking parlance. It indicates that the RBI is not locked into a predetermined path of either cutting rates or hiking rates. Instead, the committee will be nimble, reacting purely to incoming macroeconomic data.

Why the Pause? The Global Geopolitical Shock

The primary driver behind this pause is not domestic overheating, but severe global instability. The sudden escalation of the US-Iran war in the Middle East has profoundly destabilized global energy markets. With the Indian basket of crude oil surging to an average of $110 per barrel over the past two months, India—which imports over 80% of its oil—is facing an imported inflation crisis.

The partial pass-through of these higher global crude oil prices into domestic petrol and diesel prices began in May 2026. Because fuel is a universal input cost for transporting food and manufactured goods, this is causing a ripple effect across the broader CPI basket. Furthermore, global supply chain disruptions have driven up the prices of critical industrial inputs like commercial LPG, metals, plastics, and rubber.

Revised RBI Projections for FY27

In light of these shocks, the RBI has had to temper its optimism for the Indian economy:

Inflation Outlook: The RBI sharply revised its CPI inflation projection for the financial year 2026-27 (FY27) upward to 5.1%, a full 50 basis points higher than its previous estimate of 4.6%.

Growth Outlook: Concurrently, the RBI downgraded its real GDP growth forecast for FY27 from 6.9% down to 6.6%. The growth engine is facing headwinds from weak global business sentiment, trade disruptions, and high freight costs.

As Governor Malhotra noted, while domestic private consumption and fixed investment remain resilient, the Indian economy cannot fully insulate itself from the spillover effects of a major Middle Eastern conflict. By holding the rate at 5.25%, the RBI is walking a tightrope: ensuring borrowing costs are low enough to support the downgraded 6.6% growth target, while refusing to cut rates further out of fear that it would add domestic fuel to the $110-a-barrel inflationary fire.

Part 6: Strategic Advice for Borrowers, Savers, and Businesses

Understanding the mechanics of the repo rate is intellectually rewarding, but its true value lies in practical application. In the current June 2026 environment of a neutral 5.25% rate amidst global geopolitical chaos, here are actionable strategies for different stakeholders:

For Home Loan Borrowers

Audit Your Loan: If you are on an RLLR-linked floating rate, your EMI or tenure has remained stable recently. However, with the RBI raising its inflation forecast to 5.1%, the era of easy rate cuts is over for now. Prepare for the possibility of a rate hike if oil prices spiral further.

Aggressive Prepayment: If you have surplus cash, right now is an excellent time to make lump-sum prepayments against your principal. Every rupee paid toward the principal permanently reduces the interest burden, insulating you against future rate shocks.

Refinance Legacy Loans: If you are still trapped in an old Base Rate or MCLR regime from a decade ago, immediately contact your bank to switch to the RLLR framework. The transparency is worth the nominal switching fee.

For Fixed Deposit and Savings Investors

Pause Long-Term Lock-ins: With the RBI on a neutral pause and inflation risks tilted upward, do not lock all your capital into 5-year or 10-year FDs at current rates. If the Middle East crisis forces the RBI to hike rates later in 2026, you will be trapped in low-yielding assets.

Embrace Laddering: Utilize short-to-medium-term FDs (12 to 24 months) and ladder your maturities. This gives you the flexibility to reinvest at higher rates if the macro environment worsens.

Explore Alternatives: Consider highly-rated corporate deposits or government-backed schemes like the Senior Citizen Savings Scheme (SCSS) or Post Office Time Deposits, which often offer a significant premium over standard commercial bank FDs.

For Debt Mutual Fund Investors

Avoid High Duration Risk: Governor Malhotra explicitly warned that global bond markets remain under severe pressure. Until crude prices stabilize, investing in 10-year Gilt funds or long-duration funds is highly speculative and dangerous.

Focus on the Short End: Compress your portfolio duration. Deploy your capital into short-duration funds, corporate bond funds, or liquid funds. These strategies prioritize capital preservation while generating stable accrual income, protecting you from NAV erosion if interest rates suddenly spike.

For MSMEs and Corporate Borrowers

Hedge Your Forex: With the Rupee facing depreciation pressure against the US Dollar (trading near 95.24 post the June MPC meeting), businesses engaged in importing must aggressively utilize currency hedging tools.

Lock in Fixed Rates: If you are planning capital expenditure (buying machinery, expanding factories), and can secure a fixed-rate business loan at current levels, take it. The global supply-side shocks mean that the cost of capital is more likely to go up than down in the near term.

Conclusion

The repo rate is, at its core, the master lever of the Indian economy. Whether you are an EMI-paying homeowner in Delhi, a retiree living on FD interest in Chennai, or a treasury manager navigating bond markets in Bengaluru, the decisions made by the RBI’s Monetary Policy Committee ripple through every corner of your financial life.

The June 2026 decision to hold rates at 5.25% with a neutral stance serves as a stark reminder that domestic monetary policy is deeply tethered to global realities. In a world fraught with geopolitical conflict, volatile crude oil prices, and supply chain disruptions, the RBI has chosen stability and caution over aggressive action.

For the everyday Indian, staying acutely informed about the MPC’s rationale, mastering the transmission mechanisms of your bank, and proactively managing your personal balance sheet is no longer optional. In an increasingly complex and interconnected macroeconomic landscape, financial literacy regarding the repo rate is the absolute prerequisite for long-term wealth creation and stability.