Priority Sector Lending in India: Complete Guide

For anyone seeking to understand how India's banking system serves its most vulnerable and economically critical segments, priority sector lending India explained is an indispensable starting point. Priority sector lending (PSL) is one of the most consequential regulatory frameworks governing Indian banks — a policy mechanism that compels scheduled commercial banks, regional rural banks, small finance banks, and foreign banks to direct a mandated portion of their credit toward sectors that markets alone would chronically underserve. From the marginal farmer in Vidarbha to the textile entrepreneur in Tiruppur, PSL shapes who gets credit, at what scale, and under what conditions. This article examines PSL's rationale, its regulatory architecture as defined by the Reserve Bank of India (RBI), the mechanics of compliance, and the ongoing debate about whether the framework needs fundamental reform.

What Is Priority Sector Lending and Why Does It Exist in India?

Priority sector lending is a directed credit policy through which the RBI mandates that banks allocate a specified percentage of their Adjusted Net Bank Credit (ANBC) — or credit equivalent of off-balance-sheet exposures, whichever is higher — to designated sectors of the economy. These sectors are deemed "priority" not because they are financially the most lucrative for banks, but because they represent areas of national development importance where commercial credit markets have historically failed to deliver adequate or affordable finance.

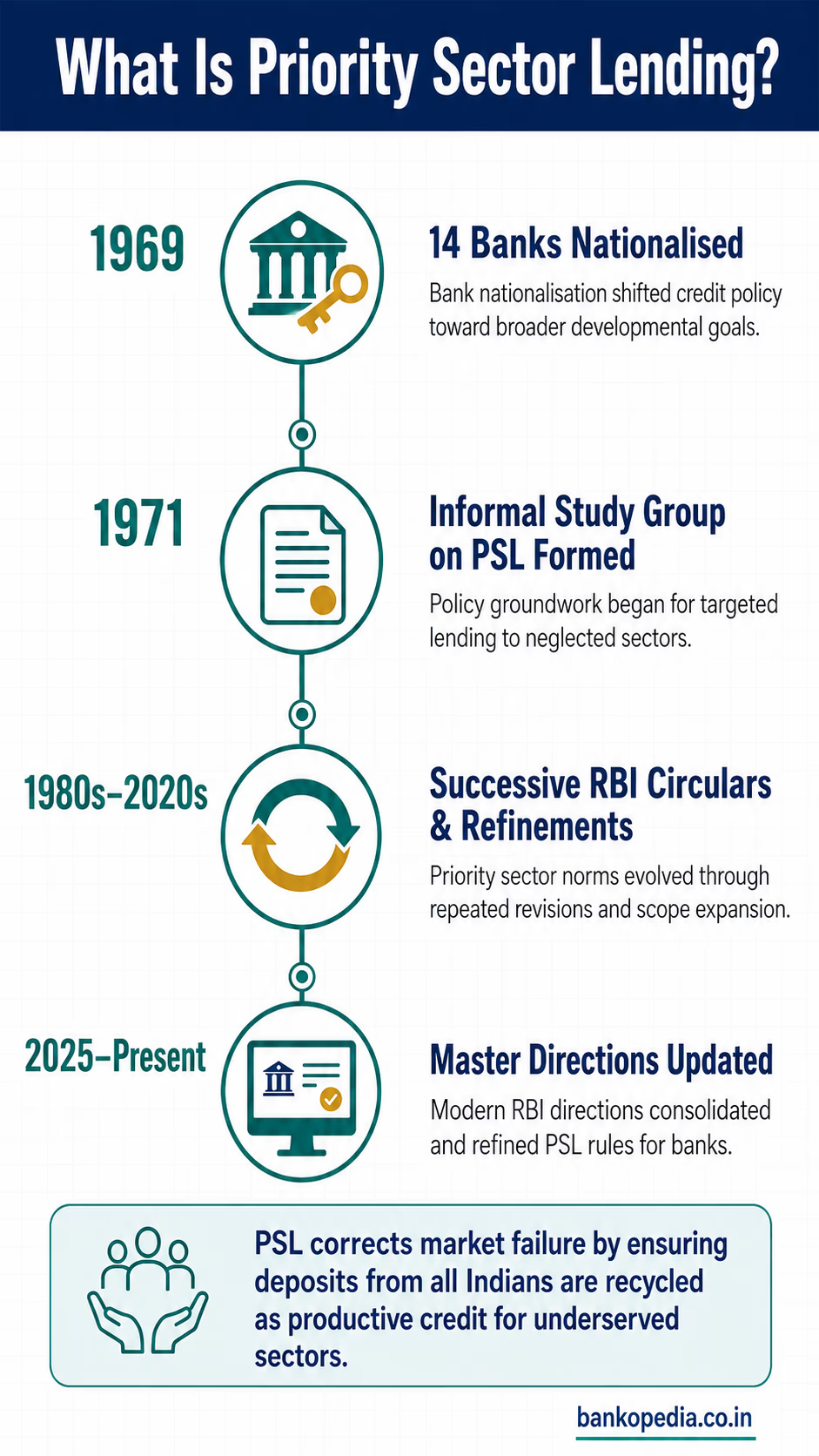

The origins of PSL trace back to the late 1960s and early 1970s, a period of intense policy focus on bank nationalisation and social banking. Following the nationalisation of 14 major commercial banks in 1969, the government and the RBI sought to use the banking system as a direct instrument of development finance. The concept was formalised after the recommendations of the Informal Study Group on Statistics Relating to Advances to the Priority Sector, set up in 1971, and subsequently refined through successive RBI circulars and committee reports.

The philosophical underpinning of PSL is straightforward: left to their own commercial logic, banks will concentrate lending in urban centres, toward large corporations and high-net-worth individuals, ignoring agriculture, small enterprises, and economically weaker sections. PSL corrects this market failure by regulatory mandate, ensuring that the deposit base — which is sourced from all segments of society, including rural and semi-urban depositors — is partially recycled back into the broader economy as productive credit.

PSL also serves as a key enabler of financial inclusion, complementing other RBI initiatives such as the Jan Dhan Yojana, the Pradhan Mantri MUDRA Yojana, and the Kisan Credit Card scheme. NABARD, the apex development finance institution for agriculture and rural development, plays a critical role in refinancing banks' PSL portfolios and in channelling credit through cooperative banks and regional rural banks (RRBs).

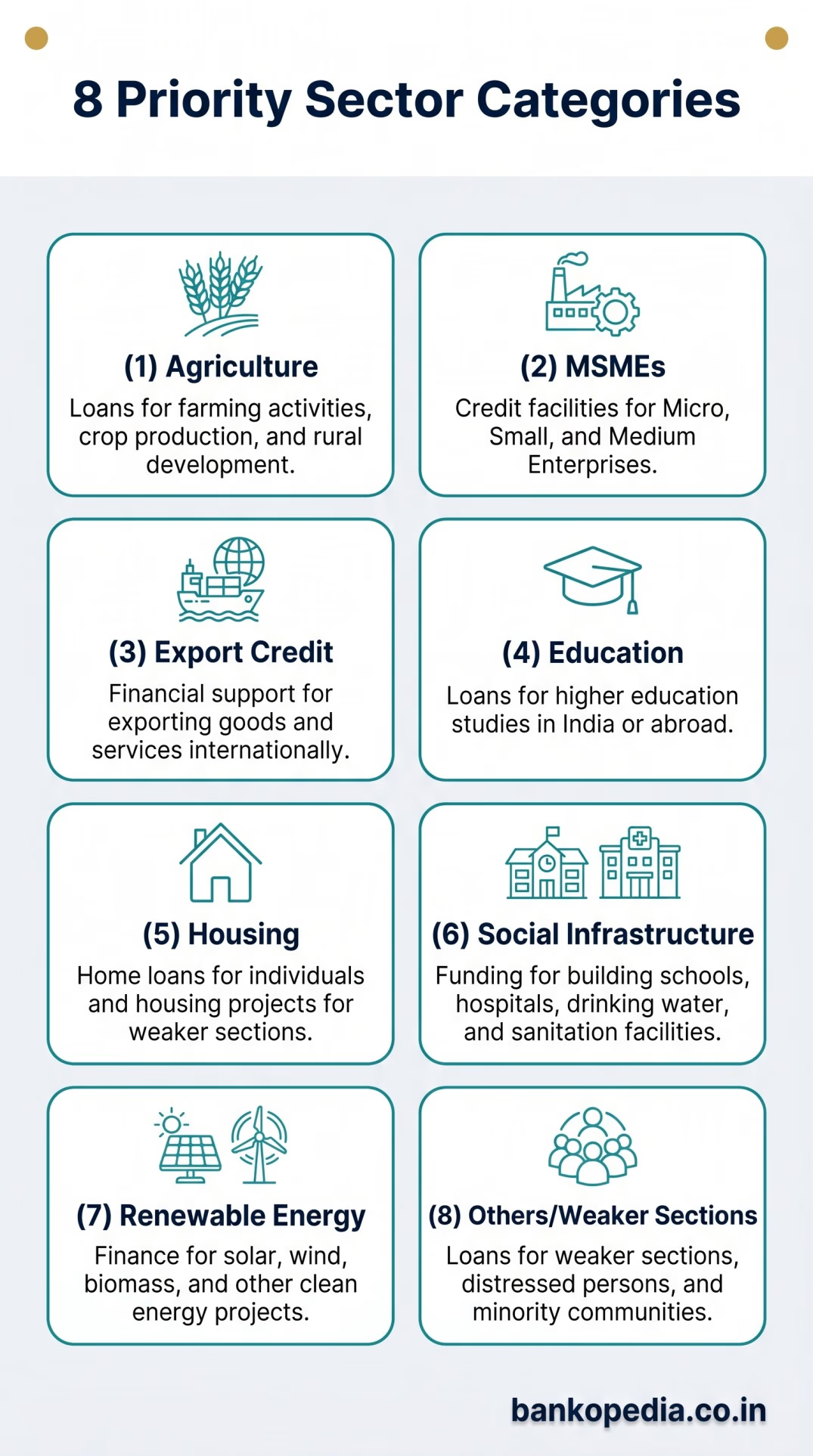

RBI's PSL Categories: Agriculture, MSME, Housing, and More

The RBI's Master Directions on Priority Sector Lending, last comprehensively updated in 2025 and periodically revised thereafter, define eight broad categories that qualify as priority sector advances. Understanding each category is essential for banking professionals managing PSL portfolios.

1. Agriculture

Agriculture is the largest and most structurally important PSL category. It encompasses farm credit (including short-term crop loans, term loans for allied activities), infrastructure development (irrigation, warehousing, cold chain), and ancillary services. Within agriculture, the RBI distinguishes between loans to small and marginal farmers — those holding up to 2 hectares of land — and other farmers. Small and marginal farmers attract a separate sub-target, recognising their heightened vulnerability to credit exclusion.

Agricultural credit flows through multiple channels: direct lending by commercial banks, NABARD refinancing, and indirect lending through cooperative credit institutions. Kisan Credit Cards, which provide revolving credit for crop cultivation, input purchases, and post-harvest expenses, form a large component of agricultural PSL.

2. Micro, Small, and Medium Enterprises (MSMEs)

MSMEs are the backbone of India's non-agricultural economy, contributing approximately 30% of GDP and employing over 110 million people. PSL credit to MSMEs covers loans for manufacturing enterprises and service enterprises, as defined under the MSMED Act, 2006 and subsequently revised by the Atmanirbhar Bharat package in 2020. The 2020 revision raised MSME investment and turnover thresholds significantly, expanding the universe of eligible borrowers.

PSL guidelines also include a specific provision for Khadi and Village Industries under the MSME bracket, reflecting their importance to rural artisanal employment.

3. Export Credit

Export credit — both pre-shipment and post-shipment — qualifies as priority sector lending up to specified limits, recognising India's strategic interest in promoting export-led growth and providing affordable working capital to exporters.

4. Education

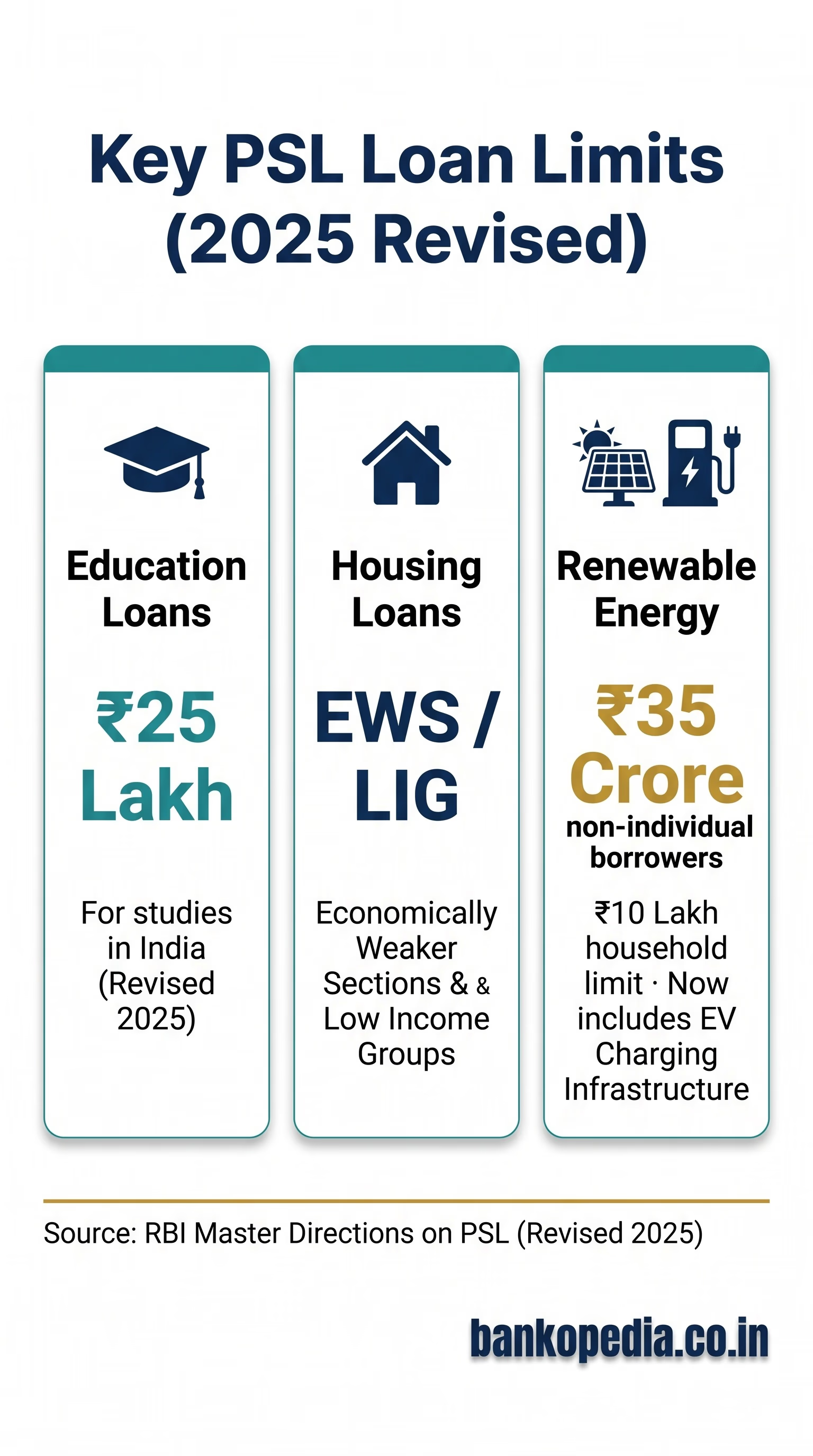

Loans to individuals for educational purposes, including vocational courses, qualify as PSL. The revised RBI guidelines set the ceiling for education loans at ₹25 lakh for studies in India and a higher limit for overseas education, subject to periodic RBI revision.

5. Housing

PSL housing loans target economically weaker sections (EWS) and low-income groups (LIG), not the high-value mortgage market. Eligible housing loans under PSL cover construction and purchase of dwelling units up to specified cost and loan amount limits — limits that have been periodically raised to reflect urban real estate inflation. Loans to housing finance companies (HFCs) for on-lending to individuals also qualify, subject to conditions.

6. Social Infrastructure

Bank loans for schools, health care facilities, drinking water projects, and sanitation facilities in Tier II to Tier VI centres (population below 1 lakh) qualify under this category, underscoring PSL's role in financing public goods.

7. Renewable Energy

Loans for solar energy systems, biomass-based power generators, wind mills, micro-hydel plants, and non-conventional energy-based public utilities are classified as PSL, with an individual loan cap of ₹35 crore for borrowers other than individuals. The individual household limit for renewable energy under PSL remains at ₹10 lakh; the revised guidelines also extend PSL coverage to include expansions for electric vehicle (EV) charging infrastructure, reflecting the sector's growing developmental importance.

8. Others

This residual category includes loans to weaker sections — SC/ST communities, women borrowers, minority communities, differently abled persons, self-help groups (SHGs), distressed farmers, and beneficiaries of government poverty alleviation schemes. It also includes advances to state-sponsored organisations for SC/ST development.

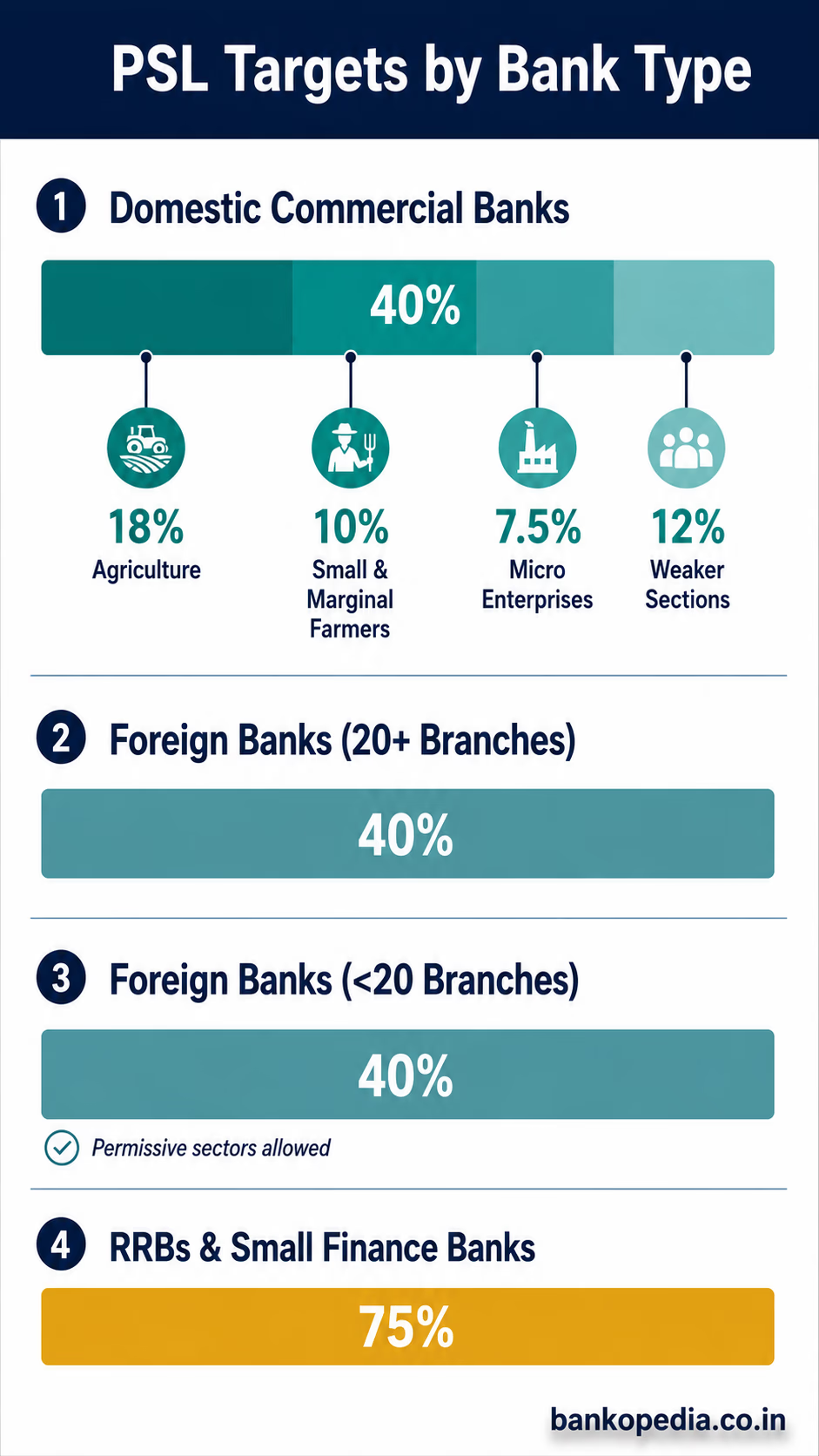

PSL Targets and Sub-Targets for Scheduled Commercial Banks

The RBI prescribes differentiated PSL targets depending on the type of bank. These targets are expressed as a percentage of ANBC or credit equivalent of off-balance-sheet exposures, whichever is higher, computed as of March 31 of the previous year.

Domestic Scheduled Commercial Banks (excluding RRBs and Small Finance Banks)

Total PSL target: 40% of ANBC

Agriculture: 18% of ANBC, of which at least 10% must flow to small and marginal farmers

Micro enterprises: 7.5% of ANBC

Weaker sections: 12% of ANBC

Foreign Banks with 20 or More Branches

Total PSL target: 40% of ANBC (aligned with domestic banks since 2020, phased in over time)

Permitted to meet targets through indirect means including investments in eligible instruments

Foreign Banks with Fewer Than 20 Branches

Regional Rural Banks (RRBs)

Small Finance Banks (SFBs)

Non-achievement of PSL targets carries financial consequences. Banks falling short must deposit the shortfall amount into the Rural Infrastructure Development Fund (RIDF) maintained with NABARD, or into other funds designated by the RBI such as those for housing, micro-enterprises, and social infrastructure. These funds carry below-market interest rates, effectively penalising underperforming banks through an opportunity cost mechanism.

Priority sector lending is not charity — it is directed finance with developmental purpose. The targets create a floor for inclusion, not a ceiling for ambition." — A view commonly echoed among RBI's development finance literature

Priority Sector Lending Certificates (PSLCs): How Banks Trade Shortfalls

One of the most innovative additions to India's PSL framework has been the introduction of Priority Sector Lending Certificates (PSLCs), operationalised by the RBI in April 2016. PSLCs allow banks that exceed their PSL targets to monetise their surplus by selling certificates to banks that fall short, creating a market-based mechanism for meeting obligations without requiring the buyer bank to actually originate priority sector loans.

How the PSLC Mechanism Works

A bank that has lent, say, 22% of its ANBC to agriculture against a target of 18% can issue PSLCs — specifically, PSLC-Agriculture certificates — representing the surplus 4%. A bank struggling to meet its agriculture sub-target can purchase these certificates on the RBI's e-Kuber trading platform. The seller bank continues to hold the underlying loans on its balance sheet; only the PSL classification benefit is transferred to the buyer. Transactions are settled in cash, with the price reflecting demand-supply dynamics on the trading platform.

There are four categories of PSLCs:

PSLC-SF/MF: Small and marginal farmers sub-target

PSLC-Agriculture: Broader agriculture target

PSLC-Micro Enterprises: Micro enterprise sub-target

PSLC-General: The overall 40% PSL target

The PSLC market has grown substantially since inception. Trading volumes have crossed tens of thousands of crores of rupees annually, reflecting both the genuine difficulty some banks face in originating specific PSL categories and the comparative advantage enjoyed by banks with deep rural networks, cooperative linkages, or microfinance portfolios. Small finance banks and RRBs are frequently net sellers of PSLCs, while some private sector and foreign banks are consistent buyers.

Critics note that while PSLCs improve compliance optics, they do not necessarily expand actual credit to underserved communities — a point that feeds into the broader reform debate.

Criticism, Reforms, and the Road Ahead for PSL Policy

Despite its developmental intent, PSL has attracted sustained criticism from economists, bankers, and policymakers. The framework is simultaneously accused of being too rigid, too leaky, and too blunt a tool for the sophisticated credit challenges India faces in the 2020s.

Key Criticisms

Asset Quality Concerns: Agricultural loans, particularly those extended under political pressure during election cycles, have historically been among the most stressed assets in bank portfolios. Loan waivers — a state-level political instrument — further distort credit culture in rural markets, creating moral hazard and discouraging timely repayment.

PSLCs Masking Non-Performance: While PSLCs are a market-based innovation, they allow banks to show PSL compliance without genuinely expanding financial access. A large urban-focused private bank can simply purchase PSLCs rather than building the branch networks or product capabilities needed to serve small farmers.

Definitional Drift: Over successive revisions, PSL categories have expanded in scope — higher loan amount limits for housing, broader MSME definitions, renewable energy — in ways that increasingly capture commercially attractive segments rather than genuinely underserved borrowers.

Operational Burden: Tracking PSL compliance, computing ANBC quarterly, maintaining sub-target records, and managing PSLC purchases imposes significant compliance costs on smaller banks with limited technology infrastructure.

The EAC-PM's Call for Reform

The Economic Advisory Council to the Prime Minister (EAC-PM) has recently flagged the need for structural changes in priority sector lending to enhance efficiency and provide greater flexibility to banks. The EAC-PM's position reflects growing recognition that a one-size-fits-all target framework may not be optimal in an era of diverse banking models, fintech-enabled credit delivery, and rapidly shifting sectoral priorities. Proposals under discussion include outcome-linked PSL credits — rewarding banks not merely for disbursement volume but for verifiable credit outcomes such as increased agricultural productivity or MSME employment generation.

Technology and the Future of PSL

The integration of Account Aggregator frameworks, GST data, and digital public infrastructure offers new possibilities for targeted PSL delivery. Rather than directing credit by broad sector classifications, future PSL frameworks could use real-time income and cash flow data to identify genuinely underserved borrowers regardless of sector label. NABARD has been piloting tech-enabled agricultural credit scoring models that could reduce lender risk and encourage voluntary priority sector lending beyond mandated floors.

The rapid growth of fintech lenders and co-lending arrangements between banks and NBFCs — a framework explicitly supported by the RBI — also creates new channels for PSL delivery. Co-lending leverages the last-mile reach of NBFCs and microfinance institutions with the low-cost funds of banks, potentially delivering better credit access at lower risk.

Global Comparisons

India's PSL framework is more prescriptive than most comparable economies. The United States has its Community Reinvestment Act (CRA), which requires banks to serve low-to-moderate income communities but does not mandate specific percentage targets. Many Southeast Asian nations use tax incentives rather than mandatory quotas to encourage development lending. As India's banking sector matures, a gradual shift from hard quotas toward incentive-compatible mechanisms — while maintaining a regulatory floor — may represent the most balanced path forward.

Conclusion: PSL as Living Policy, Not Static Mandate

Priority sector lending remains one of India's most important instruments of developmental banking, channelling trillions of rupees annually toward agriculture, small businesses, affordable housing, and economically weaker communities. Its regulatory architecture — built over five decades, refined through successive RBI Master Directions, and supplemented by market mechanisms like PSLCs — reflects the complex balancing act between commercial banking viability and social obligation.

For banking professionals, PSL compliance is not merely a regulatory checkbox but a strategic consideration that affects balance sheet composition, credit risk, NABARD relationships, and reputational standing. For policymakers, the EAC-PM's push for greater efficiency and flexibility signals that the framework must evolve — embracing technology, outcome measurement, and incentive design — without abandoning its foundational commitment to inclusive credit.

As India aspires to become a developed economy by 2047, the question is not whether priority sector lending should exist, but how it should be redesigned to deliver credit where it genuinely matters, efficiently and sustainably. The answer will shape not just bank balance sheets, but the livelihoods of hundreds of millions of Indians who depend on affordable credit to build their futures.