India's securitisation market crossed a historic milestone in FY2025, with total issuance reaching ₹2.35 lakh crore — the highest figure ever recorded in the country's financial history, representing a 24% surge over the ₹1.9 lakh crore clocked in FY2024. This is not merely a statistical footnote; it signals a structural deepening of India's credit markets, where banks and non-banking financial companies (NBFCs) are increasingly converting their loan books into tradeable instruments to unlock liquidity, optimise capital usage, and expand their lending capacity.

For bank officers, housing finance company (HFC) executives, and JAIIB/CAIIB aspirants, understanding the mechanics of Asset-Backed Securities (ABS) and Mortgage-Backed Securities (MBS) is no longer optional. These instruments sit at the intersection of credit, capital markets, and regulation — three domains that every senior banking professional must navigate with confidence.

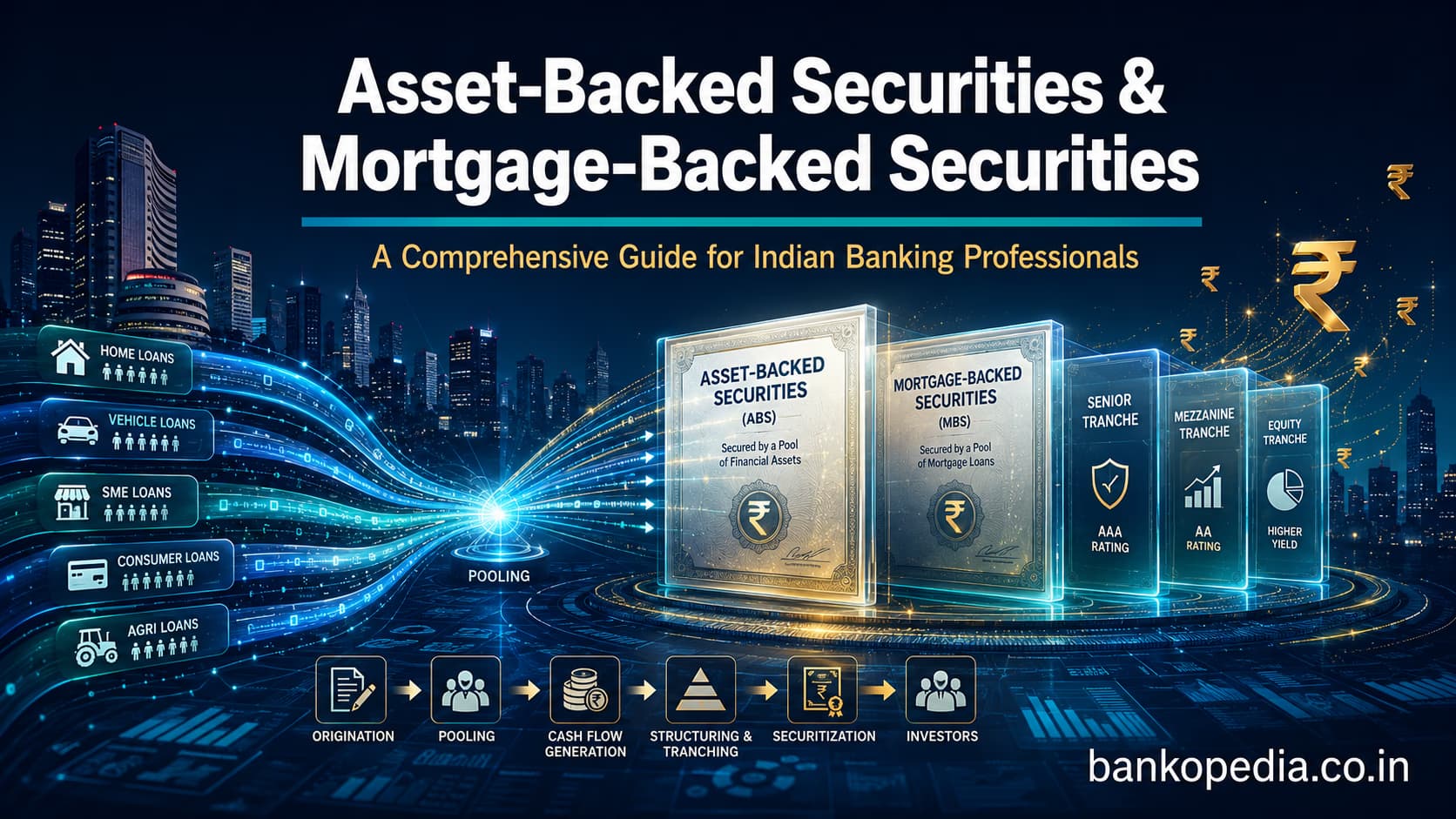

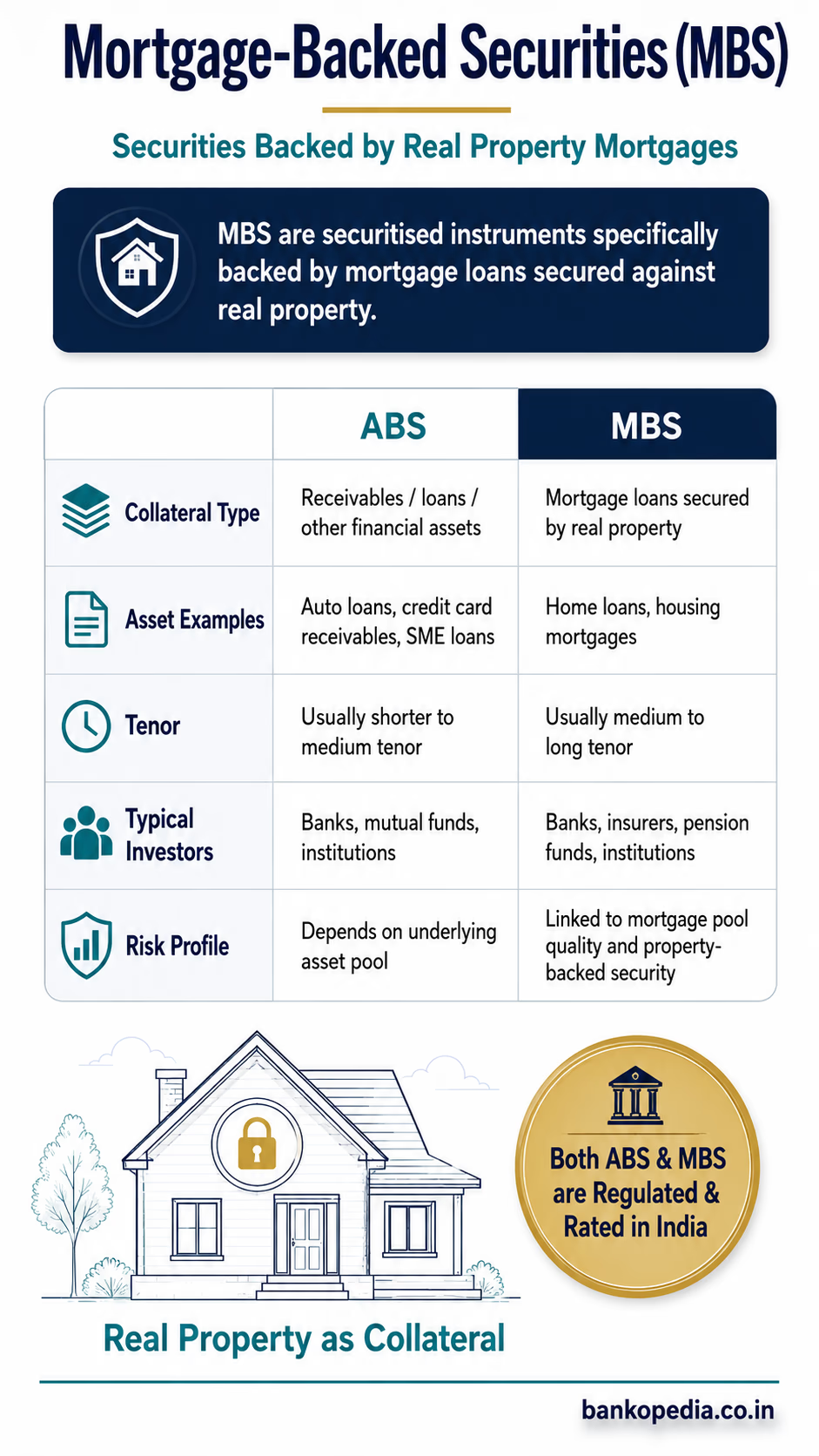

At the broadest level, both ABS and MBS are types of securitised debt instruments: financial securities whose cash flows are derived from an underlying pool of loans or receivables. The distinction lies in the collateral. ABS is backed by non-mortgage financial assets — vehicle loans, gold loans, microfinance receivables, SME loans. MBS, by contrast, is specifically backed by mortgage loans secured against real property. In India, both categories are regulated, rated, and increasingly attracting institutional investor interest.

What Is Securitisation?

Securitisation is the financial process of converting a pool of illiquid loan assets into tradeable securities that can be sold to investors in the capital markets. The core principle is elegantly simple: a lender holds thousands of individual loans on its balance sheet, each generating small but predictable cash flows. By bundling these loans together, structuring the pool, and issuing securities backed by those cash flows, the lender transforms an illiquid asset into a liquid, marketable instrument.

The process rests on three pillars: pooling (aggregating loans of similar type, tenor, and credit quality), tranching (dividing the pool's cash flows into layers with different risk-return profiles), and selling (transferring the securities to capital market investors).

Why do lenders securitise? The motivations are multiple and powerful. First, capital relief: when loans are removed from the balance sheet through a true sale, the originating bank or NBFC frees up regulatory capital that would otherwise be tied against risk-weighted assets (RWA). Second, liquidity: loans are inherently illiquid, but securities can be traded. Securitisation converts a five-year vehicle loan into an instrument an insurance company or mutual fund can buy and potentially sell. Third, risk transfer: the originator distributes the credit risk of the underlying pool to investors better positioned to bear it. Fourth, business model enablement: NBFCs with limited access to deposit funding use securitisation as a core funding tool, enabling them to originate more loans than their own equity capital would otherwise permit.

Asset-Backed Securities (ABS) — Explained

Asset-Backed Securities (ABS) are financial instruments whose interest and principal payments are sourced from a defined pool of non-mortgage financial assets. The assets are legally transferred to a Special Purpose Vehicle (SPV), which then issues securities to investors backed by those cash flows.

In the Indian context, the assets that commonly back ABS transactions span a wide range:

Vehicle loans: Commercial vehicle (CV), passenger vehicle (PV), two-wheeler, tractor, and construction equipment (CE) loans — the largest ABS asset class in India, accounting for approximately 48% of total securitisation volumes in H1 FY2025.

Gold loans: Short-duration, high-quality collateral pools originated by NBFCs such as Muthoot Finance and Manappuram.

Microfinance (MFI) loans: Unsecured group loans to borrowers at the base of the pyramid, though this segment faced significant stress in FY2025.

Personal loans: Unsecured consumer credit originated by banks and digital NBFCs.

SME and business loans: Loans to small businesses, including working capital facilities.

Loan Against Property (LAP): A hybrid between ABS and MBS — property-secured but not strictly residential mortgage loans under NHB guidelines.

Invoice discounting: Receivables from trade credit, increasingly being structured into ABS.

To illustrate with a concrete example: a large NBFC has originated ₹500 crore of commercial vehicle loans. Each loan is disbursed to a truck operator, secured against the vehicle, at 13–15% interest. The NBFC pools these loans, transfers them to an SPV, and the SPV issues Pass-Through Certificates (PTCs) of ₹500 crore to investors. Each month, as borrowers repay their EMIs, the SPV passes those cash flows — after deducting servicing fees — to PTC holders as interest and principal. The NBFC has converted a ₹500 crore illiquid loan book into ₹500 crore of fresh liquidity.

Mortgage-Backed Securities (MBS) — Explained

Mortgage-Backed Securities (MBS) are a sub-category of ABS where the underlying pool consists exclusively of loans secured by mortgages on real property. The distinction from general ABS is both legal and structural: the collateral is immovable property, loan tenors are significantly longer (10–25 years for home loans), and regulatory oversight involves the National Housing Bank (NHB) in addition to RBI and SEBI.

MBS in India is divided into:

Residential Mortgage-Backed Securities (RMBS): Backed by pools of individual home loans — salaried individuals and self-employed professionals who have taken loans to purchase or construct residential property.

Commercial Mortgage-Backed Securities (CMBS): Backed by loans secured against commercial real estate — offices, malls, warehouses. CMBS is still nascent in India compared to RMBS.

A landmark milestone in India's MBS history: LIC Housing Finance Limited issued Pass-Through Certificates backed by a pool of residential home loans, subsequently listed on the National Stock Exchange (NSE). These PTCs were rated AAA(SO) by both CRISIL and CARE Ratings, with a coupon of approximately 7.26% and a maturity of around 20 years. The "SO" suffix stands for "Structured Obligation," indicating the rating applies to the transaction structure rather than to the issuer's creditworthiness.

The National Housing Bank (NHB) has been an active promoter of the RMBS market — publishing guidelines on mortgage standardisation and participating in RMBS structures as a guarantor or credit enhancer. The macroeconomic rationale: a liquid RMBS market allows HFCs to recycle capital continuously, enabling more affordable housing loans — a critical objective under the "Housing for All" agenda.

MBS as a share of total securitisation volumes has been declining — from 33% in FY2023 to 17% in FY2024 — as vehicle loan ABS expands more rapidly. Reviving RMBS depth remains a policy priority.

The Securitisation Structure: Step by Step

Step 1 — Pool identification. The originator selects performing loans meeting defined eligibility criteria: minimum seasoning, maximum LTV, geographic diversification, and payment track record. The pool is stress-tested for historical default rates and prepayment behaviour.

Step 2 — True Sale to the SPV. The originator sells the pool to a Special Purpose Vehicle (SPV) — typically a trust under the Indian Trusts Act, 1882. This must constitute a true sale: loans are legally owned by the SPV and cannot be reclaimed by the originator's creditors in insolvency. This bankruptcy remoteness is the foundational structural protection for investors.

Step 3 — Securities issuance. The SPV issues either Pass-Through Certificates (PTCs) or structures a Direct Assignment (DA) depending on the transaction type.

Step 4 — Tranching. Securities are divided into: senior (highest credit quality, first claim on cash flows, typically AAA-rated), mezzanine (intermediate risk-return, rated AA or A), and junior/equity tranche (first-loss, absorbs initial defaults, typically retained by the originator under MRR requirements).

Step 5 — Credit Enhancement. Structural protections to achieve investment-grade ratings:

Over-collateralisation (OC): Pool size larger than securities issued (e.g., ₹550 crore of loans backing ₹500 crore of PTCs).

Cash collateral: A funded reserve account held by the SPV trustee.

Third-party guarantee: A bank or insurer guarantees a portion of pool performance.

Excess spread: Difference between pool interest earned and PTC coupon paid, accumulating as a first-loss buffer.

Step 6 — Rating. Assigned by CRISIL, ICRA, CARE Ratings, or India Ratings & Research, with the "SO" suffix denoting a structured obligation.

Step 7 — Placement with investors. Rated PTCs are placed with mutual funds, insurance companies, provident funds, pension funds, banks, and Foreign Portfolio Investors (FPIs).

Key Parties and Their Roles

Party | Role | Indian Examples |

|---|

Originator | Creates underlying loans; initiates securitisation | Shriram Finance, HDB Financial Services, LIC Housing Finance, SBI, HDFC Bank |

SPV Trustee | Holds loan pool on behalf of investors; enforces cash flow waterfall | IDBI Trusteeship, Beacon Trusteeship, Vistra ITCL |

Servicer | Collects EMIs; remits to SPV; manages delinquencies | Usually the originator; sometimes a third-party servicer |

Rating Agency | Assigns structured obligation ratings to tranches | CRISIL, ICRA, CARE Ratings, India Ratings & Research |

Investors | Purchase PTCs or acquire pools via DA | Mutual funds, LIC, GIC, NPS funds, banks, FPIs |

Regulator | Oversees compliance, SPV governance, investor protection | RBI (banks/NBFCs), NHB (HFCs/MBS), SEBI (listed instruments) |

PTCs vs Direct Assignments — The Indian Distinction

India's securitisation market has a structural peculiarity that sets it apart from most global markets: the dominance of Direct Assignments (DAs) over listed PTCs.

Pass-Through Certificates (PTCs) are rated, listed, tradeable securities issued by the SPV. A PTC investor holds a certificate entitling them to a proportional share of pool cash flows, passed through net of fees. PTCs are governed by SEBI's securitised debt instrument regulations and can be listed on BSE or NSE.

Direct Assignment (DA) is a bilateral transaction in which the originator assigns a pool of loans directly to a single buyer — almost always a bank — without creating a tradeable security. DA volumes have historically represented 60–70% of total Indian securitisation, primarily because banks use DA to meet Priority Sector Lending (PSL) targets: by purchasing eligible loan pools (agriculture, MFI, MSME) from NBFCs, banks count those loans toward their PSL quota — NBFCs get liquidity, banks get PSL compliance.

The 2021 RBI Master Directions imposed MHP and MRR on DAs as well, harmonising the regulatory floor across both structures.

Regulatory Framework in India

RBI Master Directions on Securitisation of Standard Assets, 2021 — the foundational text for banks and NBFCs:

Minimum Retention Requirement (MRR): Originator must retain a minimum 10% of the pool (first-loss/junior tranche), aligning incentives with pool performance and preventing the "originate-to-distribute" moral hazard behind the 2008 US financial crisis.

Minimum Holding Period (MHP): Loans must be held for a minimum period before securitisation — typically 6 months for tenor above 24 months, 3 months for shorter-tenor loans.

True sale requirements: Ensuring legal isolation of the pool from the originator's balance sheet.

Clean-up call: Allows originator to buy back the pool when outstanding balances fall below 10% of original pool size.

RBI (AIFI Securitisation Transactions) Directions, 2025 extend a similar framework to All-India Financial Institutions: EXIM Bank, NABARD, SIDBI, NHB, and NaBFID — bringing development finance institutions into the securitisation perimeter and potentially opening infrastructure loans and MSME credit to capital markets.

SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, amended May 2025 — expanded the eligible investor base and streamlined disclosure requirements to develop a more active secondary market.

RBI Draft Framework for Securitisation of Stressed Assets, April 2025 — proposes enabling securitisation of loans with delinquency exceeding 89 days past due, effectively creating a structured market for NPL pools and potentially unlocking significant bank balance sheet capacity.

Indian Market: Size, Growth, and Asset Mix

Year | Total Volume | Growth |

|---|

FY2023 | ~₹1.7 lakh crore | — |

FY2024 | ₹1.9 lakh crore | ~12% YoY |

FY2025 | ₹2.35 lakh crore | +24% YoY (record high) |

Asset Class | Share (H1 FY2025) | Trend |

|---|

Vehicle loans (CV, PV, tractor, 2W, CE) | ~48% | Growing; structurally dominant |

Mortgage-backed (RMBS/LAP) | ~17% | Declining as share |

Microfinance (MFI) loans | ~11% | Declining due to sector stress |

Business/SME loans | ~11% | Doubled — strong growth |

Gold loans | ~5–6% | Steady |

Personal loans & others | ~8% | Growing |

The microfinance segment's decline is particularly notable. The median Monthly Collection Ratio (MCR) for MFI pools dropped to approximately 86% in December 2024, compared to ~98% a year earlier — a stark deterioration driven by borrower over-indebtedness in several states. Key originators include Shriram Finance, Bajaj Finance, Mahindra Finance, HDB Financial Services, Tata Capital, and large HFCs such as LIC Housing Finance and PNB Housing Finance for RMBS transactions.

Benefits of ABS and MBS

For originators (banks, NBFCs, HFCs):

Capital optimisation: Removing loans through a true sale reduces RWA and improves capital ratios — critical for NBFCs under RBI's scale-based regulation (SBR) framework.

Liquidity generation: Converts locked loan assets into deployable cash, enabling more origination without additional equity.

Balance sheet de-risking: Reduces concentrated sectoral exposures without exiting origination relationships.

Funding diversification: Reduces dependence on bank credit lines and deposits, both subject to regulatory caps.

For investors (mutual funds, insurance, pension funds):

Higher yields: AAA-rated PTCs typically price 50–150 bps over equivalent-maturity G-Secs.

Asset diversification: Provides exposure to retail credit otherwise inaccessible to capital market investors.

Duration matching: Long-tenor RMBS suits insurance and pension fund liability structures for natural ALM alignment.

For the broader economy:

More credit flows to productive sectors — housing, commercial transport, agriculture.

Deepens India's corporate bond market with rated, diversified instruments.

Long-term downward pressure on borrowing costs as originators access cheaper, diversified funding.

Risks and Challenges

Prepayment risk is especially acute in MBS. When rates fall, borrowers refinance, causing mortgage pools to amortise faster than projected — forcing reinvestment at lower yields. India's limited interest rate swap market makes hedging this considerably more difficult than in the US.

Credit/default risk in the underlying pool is fundamental. MFI pools in FY2025 illustrate this clearly — widespread borrower stress caused collection ratios to deteriorate sharply, leading to subordinate tranche losses and investor caution.

Liquidity risk: India's PTC secondary market is thin. Most PTCs are placed privately and held to maturity, making price discovery unreliable and deterring new investor categories.

Servicer risk: If the originator (who typically services the pool) faces financial distress, collection quality can deteriorate even if the pool is fundamentally performing. RBI Directions require contingency servicer arrangements.

The 2008 US lesson: CDOs built on layers of subprime MBS were rated AAA based on flawed correlation assumptions. When US home prices fell simultaneously across all geographies, the diversification premise collapsed. India's safeguards — MRR ensuring originator skin-in-the-game, MHP preventing originate-and-dump, dominance of secured assets — provide meaningful protection. But structural complexity itself remains a risk: when products are opaque, credit deterioration can be disguised until it becomes severe.

Challenges Specific to India's Securitisation Market

Thin secondary market for PTCs: Most PTCs are held to maturity. The absence of active secondary trading limits price discovery and deters new investor categories.

State-level stamp duty on assignment of receivables: Rates vary significantly across states; adds 0.1–0.5% to transaction costs — a persistent structural impediment.

Non-standardised mortgage documentation: Uniform underwriting standards, property valuation methodology, and title insurance are still absent. NHB's standardisation push is ongoing.

Originator concentration: The top 10 originators dominate volumes. Mid-size banks, co-operative banks, and RRBs are largely absent from the market.

Limited FPI participation: Despite permissions under the Voluntary Retention Route (VRR), actual foreign investor participation in PTCs remains minimal.

Cost of credit enhancement: Over-collateralisation, cash collateral, and first-loss tranches add to the all-in funding cost, reducing attractiveness in certain rate environments.

Recent Developments and Future Outlook

RBI AIFI Directions, 2025: Brings NABARD, SIDBI, NHB, EXIM Bank, and NaBFID into the securitisation framework. NaBFID could become a significant originator of infrastructure loan ABS backed by roads, ports, and renewable energy projects.

SEBI SDI Amendments, May 2025: Broader investor eligibility and streamlined disclosures for listed PTCs to develop active secondary market participation.

RBI Stressed Asset Securitisation Framework (draft, April 2025): If finalised, could attract global distressed debt investors to India, accelerating resolution of legacy NPL portfolios.

NSE listing of LIC Housing Finance MBS: First live price discovery for long-tenor RMBS, building investor familiarity with the product class.

PMAY-driven affordable housing push: As home loan origination scales in Tier 2/3 cities, HFCs will require securitisation to sustain origination pace. RMBS volumes are positioned for meaningful recovery over the next 3–5 years.

Key Terms Glossary

Term | Meaning |

|---|

SPV | Special Purpose Vehicle — a legally isolated trust holding the loan pool and issuing securities |

PTC | Pass-Through Certificate — a rated, tradeable security issued by SPV entitling holder to pool cash flows |

DA | Direct Assignment — bilateral pool transfer from originator to single buyer without public issuance |

MRR | Minimum Retention Requirement — 10% of pool retained by originator (RBI Master Directions 2021) |

MHP | Minimum Holding Period — mandatory loan seasoning before securitisation (3–6 months) |

RMBS | Residential Mortgage-Backed Securities |

CMBS | Commercial Mortgage-Backed Securities |

Originator | The lender who created the underlying loans and initiates the securitisation |

Servicer | Entity (usually originator) that collects repayments and manages the pool on behalf of the SPV |

Tranching | Dividing pool cash flows into senior, mezzanine, and junior layers with different risk-return profiles |

Credit Enhancement | Structural features (OC, cash collateral, guarantees) protecting senior tranche investors from pool losses |

AAA(SO) | Highest rating for a Structured Obligation — extremely low default probability for that tranche |

JAIIB/CAIIB Relevance

For JAIIB candidates, ABS and MBS concepts are testable under Paper 2: Banking Technology and Financial Institutions and Paper 3: Principles and Practices of Banking — financial markets, capital market instruments, and bank balance sheet management.

For CAIIB candidates, this topic is directly examinable under Advanced Bank Management (ABM) — capital management, RWA, off-balance-sheet transactions, and financial innovation — and under Bank Financial Management (BFM) — ALM and funding strategy. Regulatory framework questions on MRR, MHP, true sale requirements, and the PTC vs DA distinction are frequently tested at the CAIIB level.