Capital Adequacy Norms for Indian Banks: RBI & Basel III Framework Explained

The stability of India's banking system rests on a carefully constructed regulatory architecture, and at its very heart lie the capital adequacy norms for Indian banks mandated by the RBI. These norms determine how much capital a bank must hold relative to its risk-weighted assets — acting as a financial shock absorber that protects depositors, maintains systemic confidence, and ensures that credit can continue to flow even during periods of economic stress. In early 2026, the Reserve Bank of India issued the Commercial Banks – Prudential Norms on Capital Adequacy (Third Amendment) Directions, 2026, further refining the regulatory contours that Indian banks must navigate. Against the backdrop of developments like AU Small Finance Bank's filing for a universal bank licence, IDBI Bank's ongoing divestment deliberations, and stressed asset management activities such as SBI Cards selling ₹1,800 crore in bad loans to Integro Finserv, the importance of robust capital buffers has never been more evident.

What Is Capital Adequacy and Why Does RBI Mandate It?

Capital adequacy, in its simplest form, is a bank's capacity to absorb unexpected losses without becoming insolvent. A bank collects deposits from the public, lends those funds to borrowers, and invests in various financial instruments. Every one of these activities carries risk — the risk that borrowers default, that markets fall, or that operational systems fail. Capital adequacy norms ensure that a bank maintains a minimum cushion of its own funds (capital) to absorb such losses before they begin to erode depositor money.

The Reserve Bank of India mandates these norms under its powers derived from the Banking Regulation Act, 1949, and its role as India's apex banking regulator. The RBI's regulatory mandate is not merely technical compliance — it is fundamentally about preserving public trust in the financial system. When banks are well-capitalised, they can withstand credit shocks, market downturns, and liquidity stress without requiring taxpayer-funded bailouts or triggering contagion across the financial system.

The logic is straightforward: a bank with adequate capital is:

More resilient during economic downturns, as it can absorb loan losses without breaching solvency thresholds.

More creditworthy in the eyes of counterparties and international markets, enabling cheaper access to wholesale funding.

More trustworthy for depositors, who rely on the implicit assurance that their savings are protected.

Better positioned to continue lending, thereby supporting economic activity rather than amplifying downturns.

Capital adequacy is measured through the Capital to Risk-weighted Assets Ratio (CRAR), also commonly referred to as the Capital Adequacy Ratio (CAR). This metric expresses a bank's eligible capital as a percentage of its total risk-weighted assets (RWAs). The higher the CRAR, the more financially resilient the bank is considered to be.

A well-capitalised banking system is the first line of defence against financial instability. Capital adequacy norms are not a regulatory burden — they are the foundation of sustainable banking.

Understanding Basel III: Tier 1, Tier 2 Capital and CET1

India's capital adequacy framework is anchored to the Basel III standards developed by the Basel Committee on Banking Supervision (BCBS), an international body that sets global regulatory benchmarks for banks. After the 2008 global financial crisis exposed critical weaknesses in earlier frameworks — Basel I and Basel II — the BCBS introduced Basel III in 2010 as a comprehensive reform package. The RBI began phased implementation of Basel III for Indian banks from April 2013.

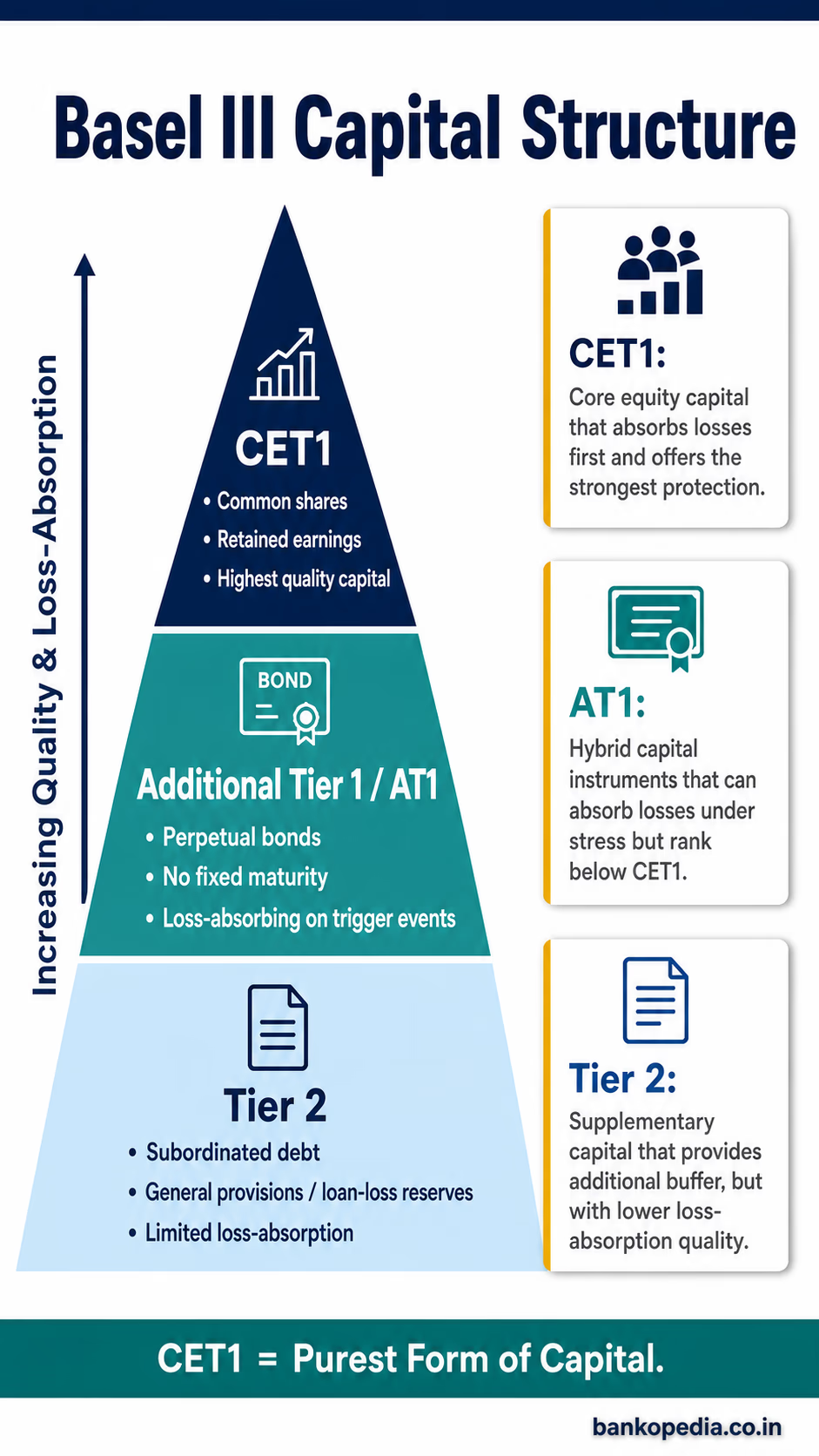

The Three-Tier Capital Structure

Basel III classifies a bank's capital into distinct tiers based on the quality and permanence of the capital instruments:

Tier 1 Capital (Going-Concern Capital)

Tier 1 capital is the highest quality of capital — funds that are permanently available to absorb losses while the bank continues to operate. It is further divided into:

Common Equity Tier 1 (CET1): This is the purest form of capital and includes paid-up equity share capital, share premium, statutory reserves, retained earnings, and other disclosed free reserves, minus regulatory deductions such as goodwill and deferred tax assets. CET1 is the most loss-absorbing form of capital and is therefore subject to the highest minimum requirement.

Additional Tier 1 (AT1) Capital: Instruments that qualify as AT1 include perpetual non-cumulative preference shares and perpetual debt instruments that meet specific criteria — they must have no fixed maturity, must be able to absorb losses through write-down or conversion to equity, and dividend or coupon payments must be fully discretionary. AT1 bonds have been a subject of significant regulatory attention in India, especially after global events such as the Credit Suisse AT1 bond write-down in 2023.

Tier 2 Capital (Gone-Concern Capital)

Tier 2 capital provides a secondary layer of protection, primarily relevant when a bank is in resolution or winding up. It includes instruments like subordinated debt (with a minimum maturity of five years), general provisions and loan-loss reserves (up to a prescribed limit), and certain hybrid instruments. Unlike CET1, Tier 2 capital is not designed to absorb losses on a going-concern basis but rather ensures that depositors and senior creditors are protected if a bank fails.

Minimum Capital Requirements Under Basel III

The Basel III framework prescribes the following minimum ratios:

CET1 Ratio: Minimum 4.5% of Risk-Weighted Assets

Tier 1 Capital Ratio: Minimum 6% of Risk-Weighted Assets

Total Capital Ratio (CRAR): Minimum 8% of Risk-Weighted Assets

Capital Conservation Buffer (CCB): An additional 2.5% of RWAs, to be maintained in CET1, bringing the effective minimum CET1 requirement to 7%.

Beyond these minimums, Basel III also introduced the Countercyclical Capital Buffer (CCyB), which regulators can activate during periods of excessive credit growth to build additional buffers against systemic risk. The RBI has the authority to set the CCyB rate for Indian banks; currently it remains at 0%, though this can be activated if credit conditions warrant.

For Domestic Systemically Important Banks (D-SIBs) — institutions whose failure could pose a risk to the broader financial system — additional capital surcharges apply. In India, the RBI designates D-SIBs annually. Currently, State Bank of India (SBI), HDFC Bank, and ICICI Bank are classified as D-SIBs and must maintain higher capital buffers commensurate with their systemic importance.

RBI's Prudential Norms on CRAR for Commercial Banks

While Basel III provides the international baseline, the RBI's own prudential guidelines — issued under the Reserve Bank of India (Commercial Banks – Prudential Norms on Capital Adequacy) Directions — translate these global standards into binding domestic requirements. The RBI has consistently applied more conservative thresholds than the Basel III minimums, reflecting India's unique financial landscape, the dominance of public sector banks, and the need to maintain depositor confidence.

Prescribed Minimum CRAR for Indian Banks

Under the RBI's Basel III guidelines, Indian commercial banks (excluding small finance banks and payment banks) must maintain:

Minimum CET1 Ratio: 5.5% of RWAs (higher than Basel III's 4.5%)

Minimum Tier 1 Capital Ratio: 7% of RWAs

Minimum Total CRAR: 9% of RWAs (higher than Basel III's 8%)

Capital Conservation Buffer: 2.5% of RWAs in CET1

Effective Minimum CET1 (including CCB): 8% of RWAs

For Small Finance Banks (SFBs), the RBI mandates a higher minimum CRAR of 15%, reflecting the higher credit risk associated with their target borrower segments — micro and small enterprises and underserved populations. This is particularly relevant in the context of AU Small Finance Bank's application for a universal bank licence. If AU SFB transitions to a universal bank, it would move to the standard CRAR framework applicable to commercial banks, while also needing to demonstrate sustained capital health across multiple business cycles.

The Third Amendment Directions, 2026

The Reserve Bank of India (Commercial Banks – Prudential Norms on Capital Adequacy) Third Amendment Directions, 2026 represent the RBI's continued calibration of the capital framework to align with the evolving Basel III finalisation standards (sometimes referred to as "Basel IV" in market parlance). Key areas typically addressed in such amendments include the standardisation of risk weights for various asset classes, revisions to the internal ratings-based (IRB) approaches, output floors that prevent banks from using internal models to derive capital requirements significantly below standardised approach results, and enhanced disclosure requirements under Pillar 3 of the Basel framework.

These amendments reflect the RBI's proactive stance in ensuring Indian banks remain aligned with international best practices, particularly as the global financial system grows more interconnected and the risks faced by Indian banks — from cybersecurity to climate-related financial risk — grow more complex.

Risk-Weighted Assets: The Denominator That Matters

A critical aspect of CRAR computation is the calculation of Risk-Weighted Assets (RWAs). Not all assets carry equal risk, and the Basel framework rightly differentiates between them. A government security (sovereign debt) carries a zero risk weight, while a personal loan to an individual may carry a 100% or higher risk weight. A mortgage loan secured by property would attract a risk weight between 35% and 100% depending on the loan-to-value ratio.

The RBI periodically revises risk weights to reflect changing credit realities. For instance, in November 2023, the RBI sharply increased risk weights on consumer credit (to 125%) and bank credit to NBFCs (to 125%), signalling concern over the rapid growth in these segments. Such macro-prudential interventions directly affect banks' CRAR and consequently their lending capacity, making risk weight calibration a powerful monetary policy tool in the RBI's arsenal.

How Capital Adequacy Ratios Affect Lending and Depositor Safety

Capital adequacy is not merely a regulatory checkbox — it has direct, tangible consequences for how banks lend, price credit, and protect the people whose money they hold.

Impact on Lending Capacity

A bank's ability to extend credit is directly constrained by its capital position. Every new loan it books increases its risk-weighted assets, which in turn reduces its CRAR if capital does not grow commensurately. A bank operating close to its minimum CRAR threshold has limited headroom to expand its loan book. This is why recapitalisation of public sector banks — including the government's periodic capital infusions into banks like Bank of Baroda, Punjab National Bank, and others — is essential for supporting credit growth in the broader economy.

The ongoing deliberations around the IDBI Bank divestment are also partly a capital adequacy story. A well-capitalised, privately managed IDBI Bank with a stronger equity base could potentially expand its lending footprint significantly, contributing to credit availability for retail and MSME borrowers.

Pricing of Credit

Banks with higher capital buffers tend to have lower funding costs, as they are perceived as lower risk by depositors and wholesale market participants. This allows them to price loans more competitively. Conversely, undercapitalised banks may face higher funding costs and must price loans at wider spreads to maintain profitability — ultimately making credit more expensive for borrowers.

Protecting Depositors

The fundamental purpose of capital adequacy norms is depositor protection. India's Deposit Insurance and Credit Guarantee Corporation (DICGC) insures deposits up to ₹5 lakh per depositor per bank — a safety net for small depositors. However, for larger depositors, institutional investors, and the broader financial system, the first line of protection is the bank's own capital buffer. A bank with a CRAR of 15% is far better placed to absorb a sudden spike in non-performing loans without threatening depositor funds than one scraping the 9% minimum.

Events such as SBI Cards selling ₹1,800 crore in stressed assets to Integro Finserv illustrate how asset quality management and capital adequacy are interlinked. By removing bad loans from its books, SBI Cards reduces its risk-weighted assets and, in doing so, either improves its capital ratio or frees up capital to support new lending.

Systemic Stability and the Broader Financial Ecosystem

Capital adequacy requirements also safeguard the wider financial ecosystem. Banks are deeply interconnected with NBFCs, insurance companies, mutual funds, and other financial intermediaries. A bank failure can trigger cascading defaults across the system. The RBI's designation of D-SIBs and the additional capital surcharges they must maintain is a recognition of this systemic interconnectedness.

The entry of new entities like MobiKwik — which has received RBI's approval for an NBFC licence and plans to launch an in-house lending arm — will also bring capital adequacy considerations into play. NBFCs are regulated by the RBI under a separate but related framework, with minimum capital requirements and leverage norms that parallel the principles underpinning bank capital regulation.

Conclusion: Capital Adequacy as the Bedrock of a Sound Banking System

Capital adequacy norms are not static regulations etched in stone — they are a living, evolving framework that the RBI continuously refines to reflect changing economic realities, global standards, and domestic risk conditions. From the foundational CET1 requirements under Basel III to the additional buffers for systemically important banks, from the conservative floors set by the RBI above international minimums to the periodic recalibration of risk weights, India's capital adequacy architecture is both comprehensive and adaptive.

For banking professionals, understanding CRAR, Tier 1 and Tier 2 capital, and the implications of the RBI's prudential directions is not optional — it is fundamental to sound risk management, strategic planning, and regulatory compliance. As Indian banks navigate a landscape marked by rapid digitalisation, rising credit demand, MSME financing imperatives, and the integration of new financial players, maintaining robust capital buffers will remain the cornerstone of institutional resilience and public trust.

Whether you are a treasury officer managing capital planning, a credit analyst assessing a bank's financial strength, or a depositor evaluating the soundness of your bank, capital adequacy ratios offer one of the most telling windows into an institution's financial health — and the RBI's role in enforcing these standards remains indispensable to India's economic stability.