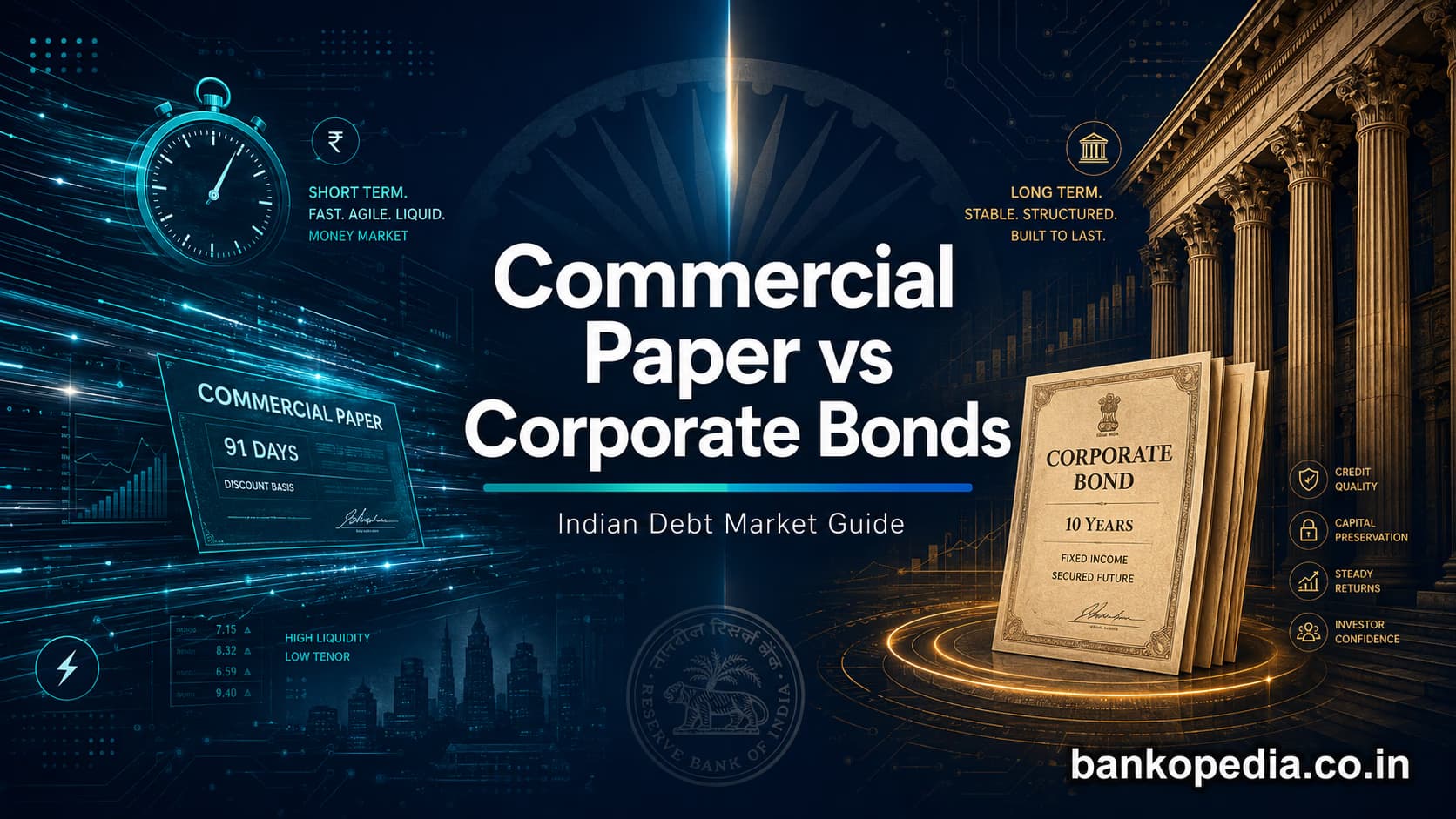

Commercial Paper vs Corporate Bonds India Difference: A Comprehensive Guide for Finance Professionals

India's debt capital markets have grown significantly in depth and breadth over the past decade, offering corporates a widening spectrum of instruments to raise funds beyond traditional bank credit. Among the most actively used are commercial paper (CP) and corporate bonds — two instruments that, while both falling under the broad umbrella of debt financing, serve fundamentally different purposes and attract distinct issuer and investor profiles. Understanding the commercial paper vs corporate bonds India difference is not merely an academic exercise; it is a practical necessity for treasury managers, CFOs, institutional investors, and banking professionals who operate in today's dynamic fixed-income landscape. Indeed, recent market data confirms that India Inc raised more through CPs vis-à-vis corporate bonds in FY27 so far, underscoring the renewed appetite for short-term instruments amid evolving liquidity conditions and interest rate expectations.

What Is Commercial Paper and How Does It Work?

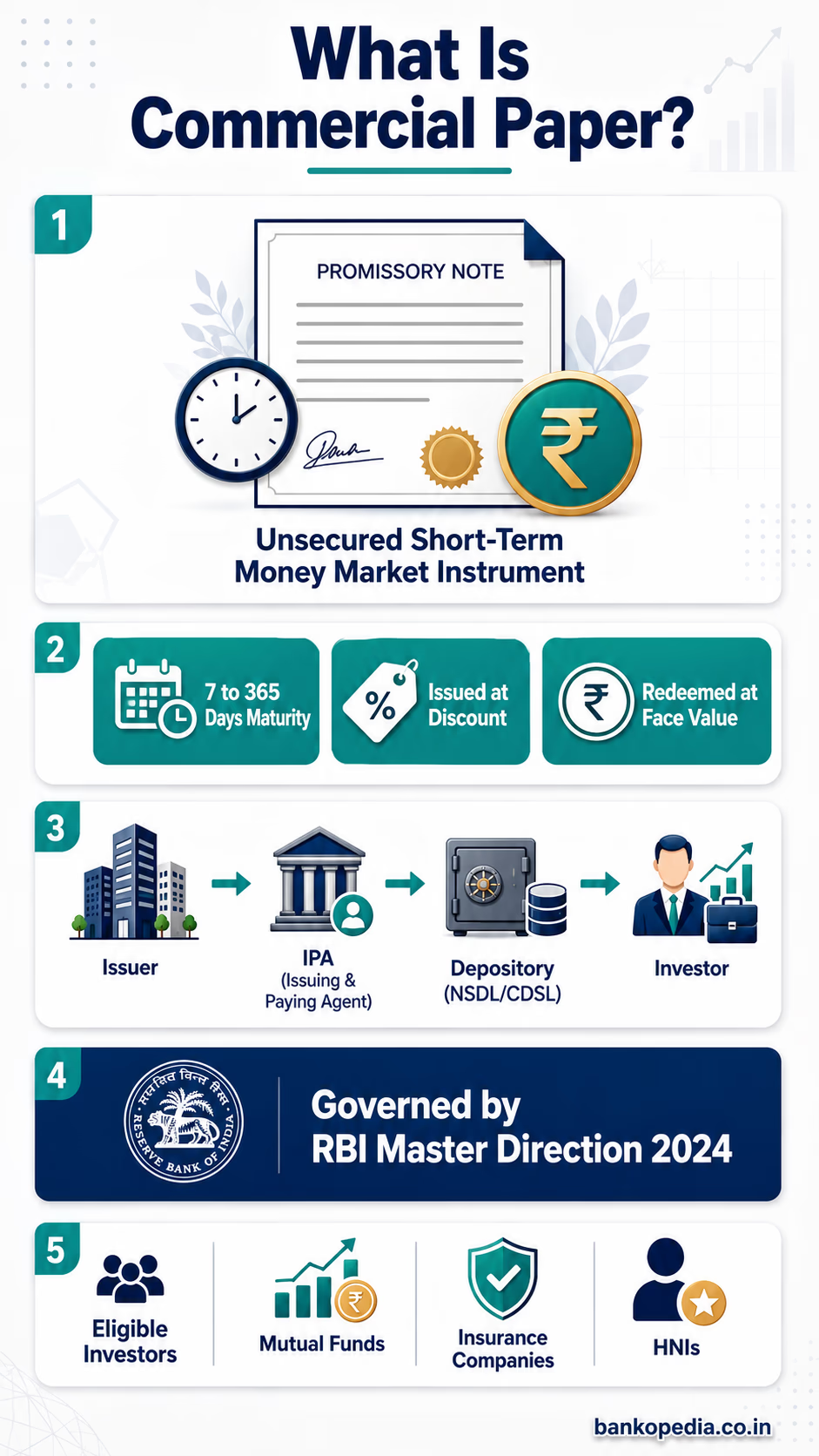

Commercial paper is an unsecured, short-term money market instrument issued in the form of a promissory note by eligible entities to meet their immediate working capital requirements or bridge financing needs. In India, commercial paper is governed by the Reserve Bank of India (RBI) under its Master Direction – Reserve Bank of India (Commercial Paper and Non-Convertible Debentures of original or initial maturity up to one year) Directions, 2024, which came into effect on April 1, 2024. The regulatory framework has evolved considerably since CPs were first introduced in India in 1990, with the RBI periodically refining eligibility norms, credit rating requirements, and operational guidelines.

Eligibility to Issue Commercial Paper

Not every entity can access the CP market. Under the RBI's 2024 Master Directions, the eligibility framework has been modernised and is as follows:

Companies (incorporated under the Companies Act) are eligible to issue CPs provided their existing borrowal accounts — that is, fund-based facilities from banks or NBFCs — are classified as Standard Assets. The earlier requirement of a minimum tangible net worth of ₹4 crore for companies has been removed under the 2024 framework.

Other body corporates, co-operative societies, and limited liability partnerships (LLPs) are eligible subject to a minimum net worth of ₹100 crore, as prescribed under the 2024 Master Directions.

Primary dealers (PDs) and satellite dealers

All-India financial institutions (AIFIs) permitted by the RBI

Non-banking financial companies (NBFCs) meeting prescribed net owned fund criteria

Certain other entities as notified by the RBI from time to time

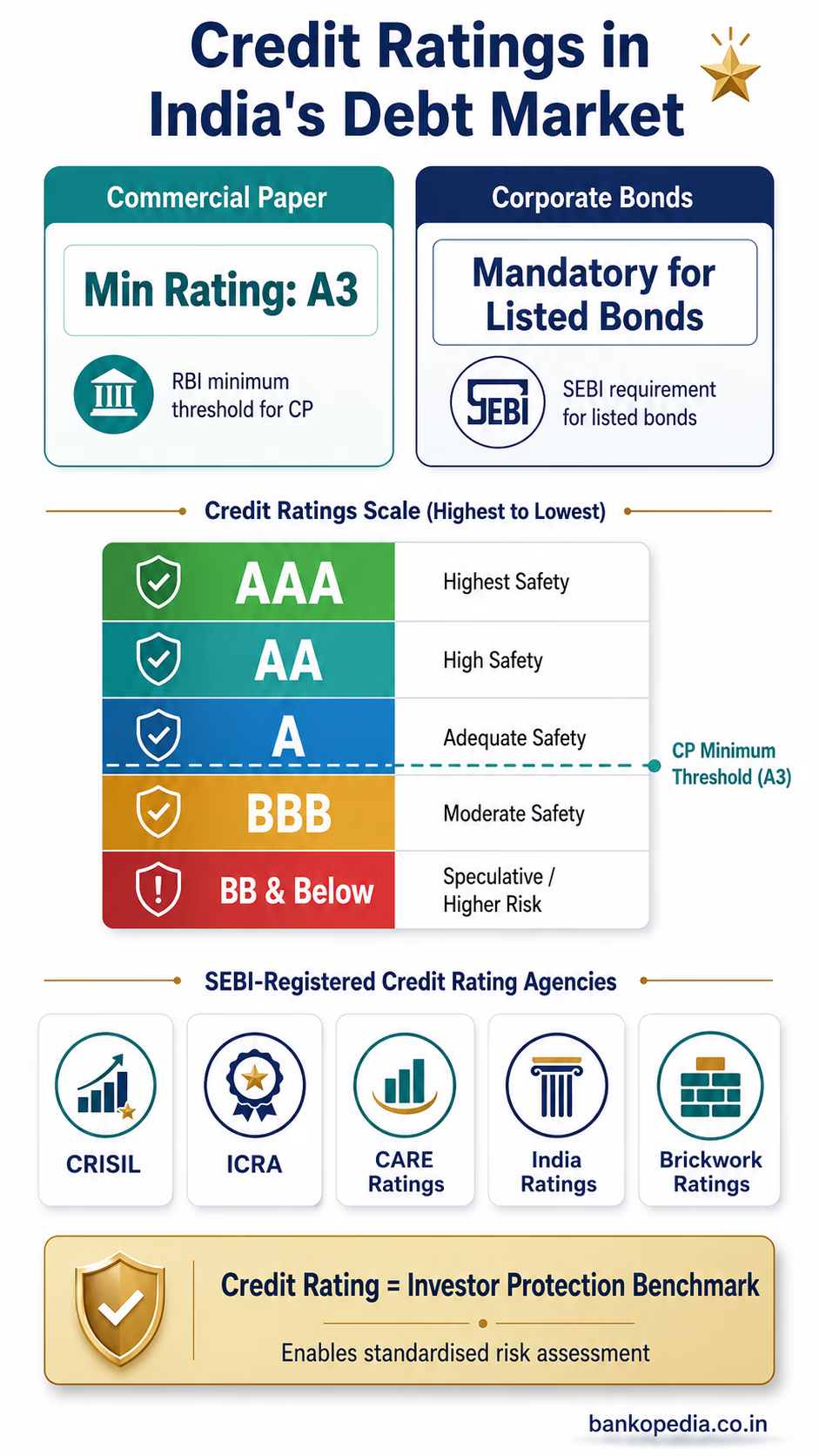

Crucially, the issuer must have a minimum credit rating of A3 (or equivalent) as assigned by a SEBI-registered credit rating agency such as CRISIL, ICRA, CARE, India Ratings, or Brickwork Ratings. This mandatory rating requirement ensures a minimum threshold of creditworthiness and provides investors with a standardised risk benchmark.

Maturity and Denomination

CPs have a minimum maturity of 7 days and a maximum maturity of up to 1 year from the date of issue. They are issued in denominations of ₹5 lakh and multiples thereof, making them primarily accessible to institutional investors, mutual funds, insurance companies, and large HNI portfolios. CPs are issued at a discount and redeemed at face value — the difference representing the return to the investor. There is no coupon payment mechanism as such; the yield is embedded in the discount structure.

Issuance Mechanics

Issuers typically work with an Issuing and Paying Agent (IPA) — usually a scheduled commercial bank — who facilitates the issuance process, verifies documentation, and ensures settlement. CPs must be issued in dematerialised form through depositories (NSDL or CDSL), enhancing transparency and operational efficiency. The secondary market for CPs operates through over-the-counter (OTC) trades, though liquidity can be uneven depending on issuer quality and prevailing money market conditions.

"Commercial paper effectively allows blue-chip corporates and well-rated NBFCs to bypass bank credit lines for short-term needs, often at a lower cost — particularly when banking system liquidity is comfortable and money market rates are benign."

Corporate Bonds: Features and Issuance Process

Corporate bonds are medium-to-long-term debt securities issued by companies to raise capital for a variety of purposes — project financing, capital expenditure, refinancing of existing debt, or general corporate purposes. Unlike commercial paper, corporate bonds carry a defined coupon (interest rate), a fixed tenor typically ranging from 2 years to 30 years or more, and are governed primarily by SEBI's regulations under the SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021.

Public vs. Private Placement

In India, corporate bonds can be issued either through a public issue (open to retail and institutional investors, requiring a detailed prospectus filed with SEBI) or through a private placement. Under Section 42 of the Companies Act, 2013, a private placement is restricted to a maximum of 200 persons in a financial year — however, it is important to note that Qualified Institutional Buyers (QIBs) and employees receiving stock options are explicitly excluded from this count. In practice, the overwhelming majority of corporate bond issuances in India are subscribed by QIBs such as mutual funds and insurance companies, meaning the effective reach of a private placement can extend well beyond 200 participants when institutional buyers are involved. This is a pattern that regulators and market participants have long been focused on changing in order to deepen retail participation in the bond market.

Credit Rating and Listing

SEBI mandates that publicly issued corporate bonds must carry a credit rating from at least one SEBI-registered rating agency. For privately placed bonds that are listed on recognised stock exchanges (BSE or NSE), rating requirements also apply. The listing of corporate bonds provides a measure of liquidity and price transparency, though the secondary market for corporate bonds in India remains relatively thin compared to G-Sec markets — a structural challenge that RBI and SEBI have been working to address through initiatives like the Electronic Book Mechanism (EBP platform) for debt securities.

Secured vs. Unsecured Bonds

Corporate bonds may be secured (backed by specific assets or a charge on the company's assets) or unsecured. Secured bonds provide bondholders with recourse in the event of default and typically command a lower yield premium. Debenture trustees — regulated by SEBI — play a critical role in monitoring the security cover and protecting bondholder interests throughout the life of the instrument.

Key Structural Features

Coupon structure: Fixed, floating (linked to MIBOR, repo rate, or T-bill yields), or zero-coupon

Redemption provisions: Bullet repayment, amortising, or with put/call options

Green and sustainability-linked bonds: A growing segment in India, with SEBI's green bond framework gaining traction

Infrastructure bonds: Eligible for tax benefits under Section 80CCF historically, though current provisions vary

Key Differences in Maturity, Cost, and Eligibility

While both instruments are debt obligations of the issuer, the commercial paper vs corporate bonds India difference becomes starkly apparent when one examines maturity profiles, cost dynamics, issuer eligibility, and structural characteristics side by side.

Maturity Profile

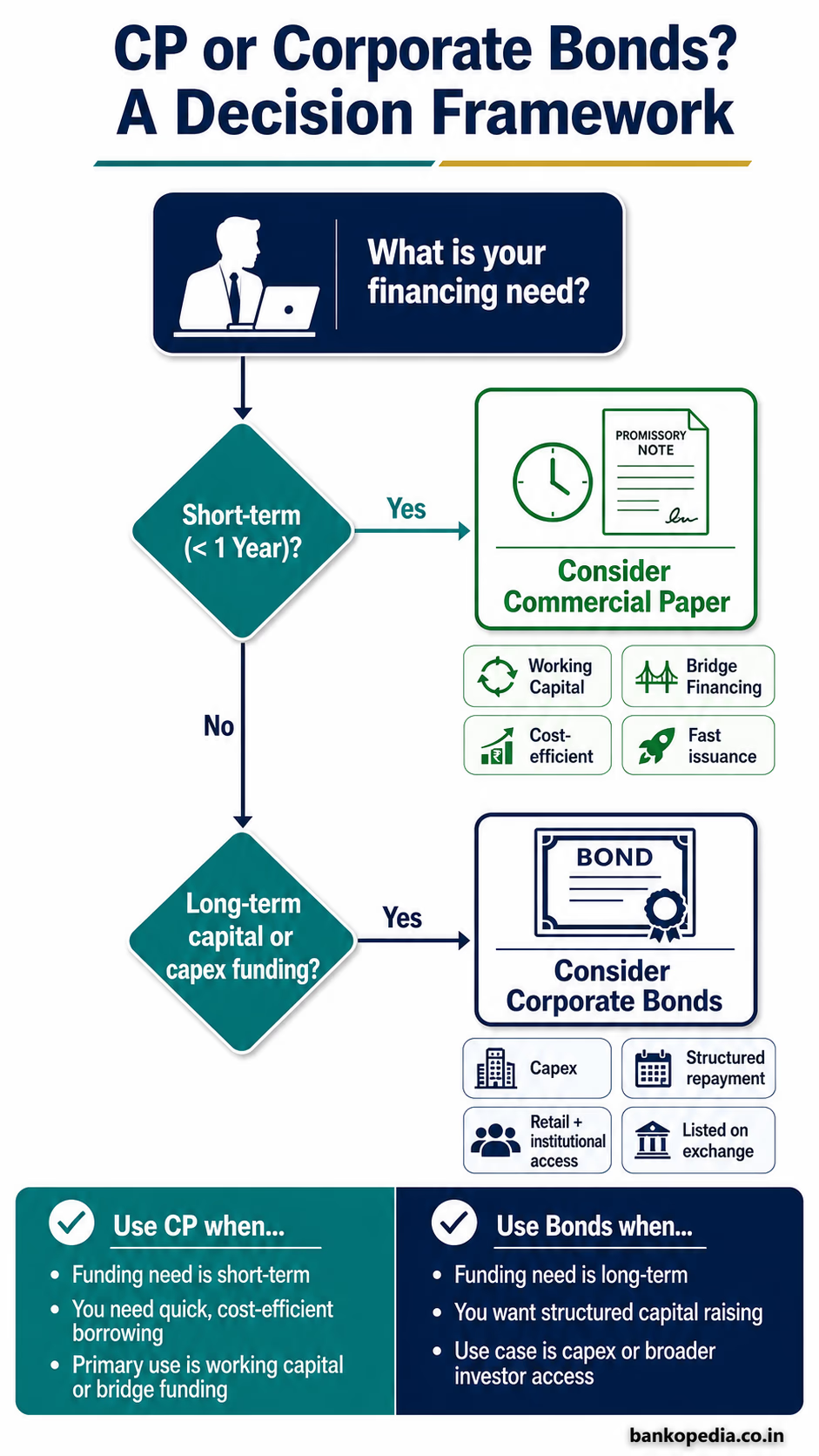

This is the most fundamental distinction. CPs are strictly short-term instruments — 7 days to 1 year — designed for working capital and transient liquidity needs. Corporate bonds, by contrast, are medium-to-long-term instruments with maturities typically ranging from 2 to 30 years, making them suitable for funding capital projects, infrastructure development, or long-term refinancing strategies. A company cannot use a CP to fund a 10-year infrastructure project; similarly, it would be inefficient to issue a 10-year bond merely to fund a seasonal working capital requirement.

Cost of Issuance

CPs are generally cheaper to issue in absolute terms. The issuance process is streamlined, documentation requirements are lighter compared to a public bond issue, and the tenor alignment with short-term money market conditions often enables lower effective borrowing costs — especially when the yield curve is steep or when banking system liquidity is flush. Corporate bonds, particularly public issues, entail higher transaction costs: underwriting fees, debenture trustee fees, listing fees, credit rating costs (ongoing), and compliance-related expenditures add to the total cost.

However, it is important to note that CP costs are variable and market-sensitive. During periods of tight liquidity, credit stress, or monetary policy tightening, CP yields can spike sharply — as was witnessed during episodes like the IL&FS crisis of 2018 and the NBFC liquidity squeeze that followed. A corporate bond, once issued at a fixed coupon, locks in the borrowing cost for its entire tenor, providing interest rate certainty that CPs cannot offer.

Eligibility and Access

Corporate bonds are accessible to a wider universe of issuers — any company incorporated under the Companies Act can potentially issue bonds, subject to SEBI regulations and market appetite. CP eligibility, while broadened under the RBI's 2024 Master Directions, still requires issuers to meet specific conditions: companies must have their borrowal accounts classified as Standard Assets, while other body corporates, co-operative societies, and LLPs must meet a ₹100 crore net worth threshold. The mandatory minimum credit rating of A3 continues to limit CP market access to only well-established, creditworthy entities. Smaller or mid-rated companies that might be able to issue long-tenor secured bonds at moderate yields may find the CP market entirely inaccessible.

Investor Base

CPs primarily attract institutional money market investors — mutual funds (especially liquid and money market funds), insurance companies, corporate treasuries, and banks. Corporate bonds attract a broader investor base including insurance companies (regulated by IRDAI with prescribed investment norms), provident funds, pension funds (regulated by PFRDA), mutual funds, foreign portfolio investors (FPIs), and increasingly retail investors through platforms enabled by SEBI's regulatory push.

Risk and Return Profile Comparison

From a risk perspective, both instruments carry credit risk (the risk of issuer default), but their risk profiles differ materially in terms of duration, liquidity, and structural protections.

Duration and Interest Rate Risk

CPs, by virtue of their short tenor, carry minimal interest rate risk (duration risk). An investor holding a 90-day CP is exposed to market interest rate movements for only 90 days. Corporate bonds, particularly those with 10- or 15-year maturities, carry significant duration risk — their market value is sensitive to changes in benchmark interest rates, and mark-to-market losses can be substantial during rate-rising cycles.

Credit and Refinancing Risk

Paradoxically, CPs may carry higher refinancing risk for issuers. Since CPs mature within a year, the issuer must continuously roll them over. If market conditions deteriorate — due to a credit event, sectoral stress, or systemic liquidity tightening — the issuer may be unable to roll over maturing CPs, potentially triggering a liquidity crisis. This "rollover cliff" is a well-documented vulnerability, particularly for NBFCs and housing finance companies that historically relied heavily on short-term CP funding for long-term mortgage assets, creating dangerous asset-liability mismatches.

Corporate bonds, with their longer maturities, reduce this refinancing frequency risk. An issuer who successfully places a 7-year bond does not need to return to the market for that tranche for seven years.

Collateral and Recovery

CPs are unsecured instruments — in the event of issuer default, CP holders rank as unsecured creditors with limited recourse. Secured corporate bonds, by contrast, offer bondholders a claim on specific charged assets, theoretically improving recovery rates in insolvency proceedings under the Insolvency and Bankruptcy Code (IBC), 2016.

Returns

In a normal yield curve environment, corporate bonds offer higher absolute yields than CPs of the same issuer, compensating investors for taking on longer duration and liquidity risk. However, on a risk-adjusted, short-term basis, CP yields can be competitive — and for liquid fund investors, the tax efficiency and mark-to-market treatment under mutual fund structures make CPs an attractive portfolio component.

When Should Companies Issue CPs vs. Bonds?

The choice between commercial paper and corporate bonds is ultimately a strategic treasury decision, influenced by the purpose of the borrowing, prevailing market conditions, the issuer's credit profile, and the desired liability structure.

Situations Favouring Commercial Paper

Short-term working capital needs: Seasonal inventory build-up, debtor financing, or bridge requirements ahead of a long-term fundraise

Exploiting favourable short-term rates: When the money market is flush with liquidity and short-term rates are significantly below long-term bond yields, CPs offer meaningful cost arbitrage

Flexibility requirements: CPs allow issuers to borrow for very specific periods (as short as 7 days) without committing to long-term debt structures

Strong credit rating and brand: For AAA/AA-rated issuers, the CP market offers near-instantaneous access to large volumes at competitive rates with minimal friction

Situations Favouring Corporate Bonds

Capital expenditure and project financing: Long-gestation infrastructure projects, plant expansions, or asset-heavy businesses require tenure-matched financing that only bonds can provide

Asset-liability management discipline: Financial intermediaries (NBFCs, HFCs) must match funding tenors to asset maturities — over-reliance on CPs for long-term loan books is a recipe for systemic stress

Locking in rates ahead of expected rate hikes: When interest rates are expected to rise, locking in long-term borrowing at current coupon rates is strategically prudent

Diversifying investor base: Bond issuances — especially listed public issues — broaden the investor base beyond money market mutual funds and reduce concentration risk

Building a credit curve: Regular bond issuances across maturities help issuers establish a visible credit curve, enhancing market reputation and future borrowing capacity

India Inc's recent preference for CPs over corporate bonds in FY27 reflects a deliberate tactical choice — corporates are betting on near-term rate cuts and preferring the flexibility of short-term instruments over committing to long-term coupon rates amid evolving monetary policy signals from the RBI Monetary Policy Committee.

Conclusion: Two Instruments, One Strategic Framework

Commercial paper and corporate bonds are not competing instruments — they are complementary tools in a well-structured corporate financing strategy. The ideal debt capital structure leverages CPs for short-term liquidity management while relying on bonds for stable, tenure-matched long-term funding. Mature treasury functions in large Indian conglomerates routinely operate both CP programmes and bond shelf registrations simultaneously, calibrating the mix based on prevailing rates, maturities due, and strategic capital needs.

For investors, understanding the commercial paper vs corporate bonds India difference is equally critical. The two instruments serve distinct portfolio roles — CPs belong to the liquidity management and short-duration bucket, while corporate bonds serve as core fixed-income allocations in medium-to-long-term portfolios. Regulatory frameworks from the RBI (for CPs, updated via the 2024 Master Directions) and SEBI (for bonds) ensure a structured, rating-driven ecosystem, but investors must remain vigilant about credit quality, rollover risks, and liquidity conditions — lessons that India's debt markets have had to learn the hard way through high-profile credit events.

As India's bond market continues to mature — driven by SEBI's market development initiatives, RBI's liquidity management frameworks, and the broader push to deepen domestic capital markets — the relative importance of both CPs and corporate bonds will only grow. For banking and finance professionals, mastering the nuances of both is not optional; it is foundational.