Part 1: Understanding the Fundamentals of FCNR(B) Accounts

Before diving into the high-yield dynamics of the 2026 market, it is essential to understand the bedrock principles of the FCNR(B) scheme. Introduced by the RBI in 1993 to replace the older FCNR(A) scheme, the FCNR(B) account is a specialized term deposit designed specifically to insulate overseas Indians from exchange rate volatility.

The Core Value Proposition: Currency Protection

The defining feature of an FCNR(B) account is that it is maintained purely in foreign currency. When you remit US Dollars, British Pounds, or Euros into an FCNR(B) account, the funds are not converted into Indian Rupees (INR). Both the principal amount and the interest earned are calculated, held, and eventually repaid in that original foreign currency.

This mechanism completely eliminates currency risk for the depositor. If the Indian Rupee depreciates against the US Dollar by 15% over a five-year period, an FCNR(B) depositor remains entirely unaffected, as their maturity proceeds are guaranteed in US Dollars.

Permitted Currencies

While the exact lineup can vary slightly depending on the banking institution, the RBI permits FCNR(B) deposits to be maintained in major freely convertible global currencies. The standard suite offered by almost all major Indian commercial and small finance banks includes:

US Dollar (USD)

Pound Sterling (GBP)

Euro (EUR)

Japanese Yen (JPY)

Canadian Dollar (CAD)

Australian Dollar (AUD)

(Note: As of recent updates, some banks like ICICI have discontinued less common currencies such as the Hong Kong Dollar (HKD) for new and renewing deposits).

Eligibility: Who Can Open an FCNR(B) Account?

The eligibility criteria are strictly governed by the Foreign Exchange Management Act (FEMA), 1999, and ongoing RBI master directions. The following individuals are permitted to open and maintain FCNR(B) deposits:

Non-Resident Indians (NRIs): Indian citizens who are residing outside of India for the purposes of employment, carrying out a business or vocation, or under circumstances indicating an uncertain duration of stay abroad.

Overseas Citizens of India (OCIs) & Persons of Indian Origin (PIOs): Foreign nationals of Indian ancestry who hold a valid OCI card.

Returning NRIs (Transitional): If an NRI returns to India permanently, they can allow their existing FCNR(B) deposits to run until maturity at the contracted interest rate. Upon maturity, the funds must be converted into domestic Rupee accounts (or RFC accounts).

Joint Account Regulations: Resident Indians are not permitted to open FCNR(B) accounts as primary holders. However, an eligible NRI or OCI can open a joint FCNR(B) account with another eligible non-resident. Furthermore, an NRI can add a resident Indian close relative (such as a parent, spouse, or sibling) as a joint holder, but strictly on a "former or survivor" basis. This means the resident relative cannot operate the account or withdraw funds during the lifetime of the primary NRI account holder.

Structural Limitations

Unlike NRE accounts, which offer the liquidity of savings and current accounts alongside fixed deposits, the FCNR(B) scheme is exclusively a term deposit (fixed deposit) product. You cannot open an FCNR(B) savings account, nor can you use it for daily transactional banking or issuing checks. The standard permissible tenure for these deposits ranges from a minimum of 1 year to a maximum of 5 years.

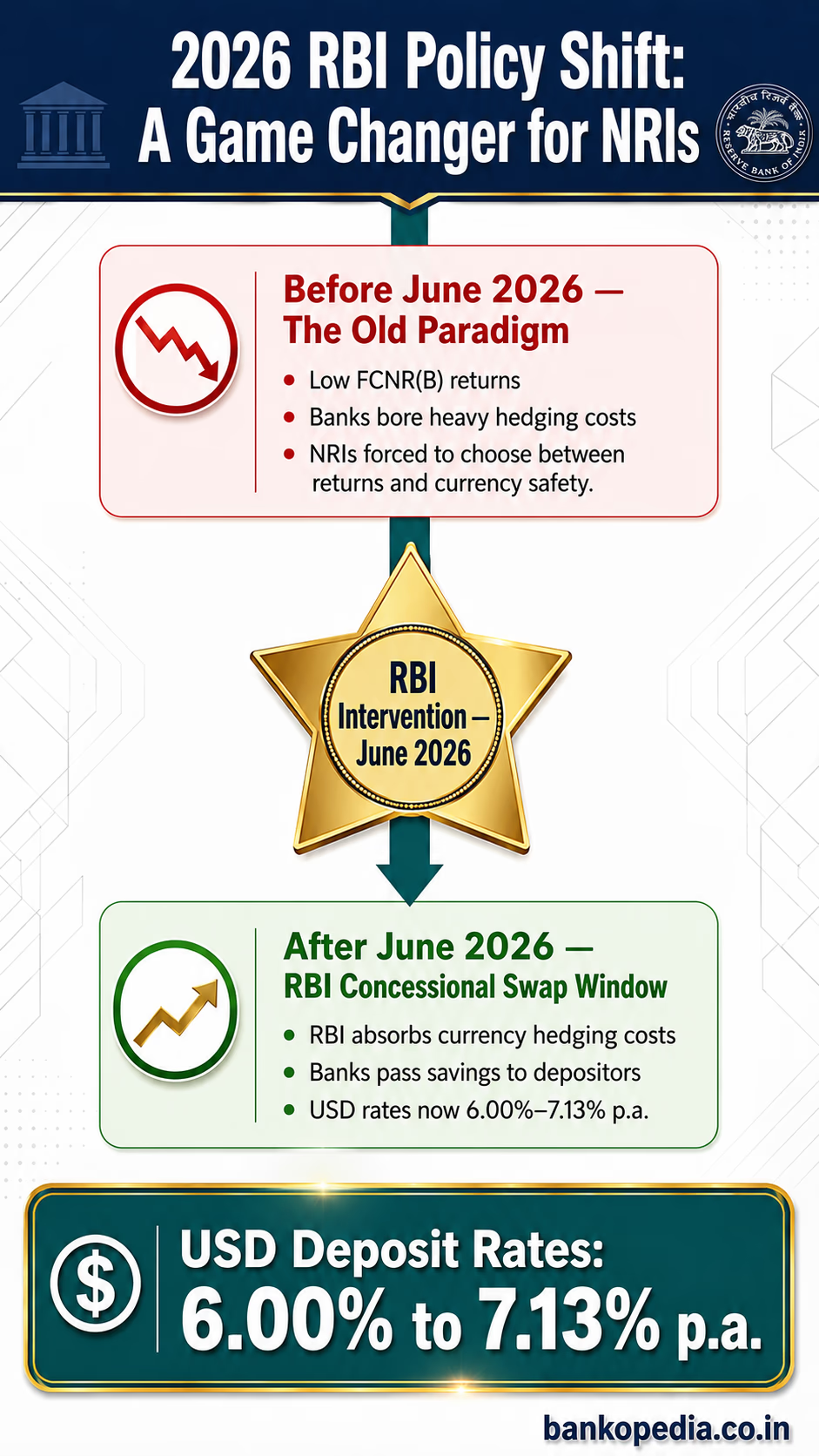

Part 2: The June 2026 RBI Masterstroke Explained

To understand why FCNR(B) rates have suddenly spiked from a modest 3.50% to over 7.00% in 2026, we must look at the mechanics of international banking and a historic intervention by the RBI.

The Historical Problem: The Cost of Hedging

Prior to June 2026, when an Indian bank accepted a 5-year USD deposit from an NRI, it faced a massive currency mismatch. The bank took in Dollars, but it operates primarily in Rupees. To utilize these funds to give out loans in India, the bank had to convert the USD into INR. However, at the end of the 5-year tenure, the bank is legally obligated to return the original amount in USD, plus interest.

If the Rupee depreciated significantly over those five years, the bank would suffer catastrophic losses when buying back Dollars to repay the NRI. To prevent this, banks were required to hedge their currency risk in the forward market. In mid-2026, the cost of hedging this USD-INR exposure in the forward market was hovering around 2.80% to 3.00% per annum (280 to 300 basis points).

Because banks had to pay this massive 3% premium just to protect themselves from currency fluctuations, they passed that cost onto the depositor by severely depressing the interest rates they offered. This is why, prior to June 2026, a standard USD FCNR(B) rate was stuck in the 3.00% to 4.00% range.

The RBI Intervention: June 8, 2026

Facing global macroeconomic uncertainty, a strong US Dollar, and a desire to significantly bolster India's foreign exchange reserves (aiming to attract an estimated $50 billion to $70 billion in inflows), the RBI launched a massive stimulus package reminiscent of its famous 2013 taper-tantrum playbook.

On June 8, 2026, the RBI issued a series of circulars introducing a concessional USD-INR forex swap facility for banks.

How the Swap Facility Works: Under this special window, when a bank mobilizes a fresh FCNR(B) deposit in USD for a tenure of 3 to 5 years, the bank no longer has to buy an expensive hedge in the open market. Instead, the RBI itself acts as the counterparty. The bank sells the USD to the RBI at the spot rate and enters into a swap agreement to buy the USD back at maturity at par (or at a highly subsidized forward rate).

In simple terms, the RBI has decided to absorb the entire 2.80% to 3.00% annual hedging cost.

The Ripple Effects: Rate Caps Removed and CRR/SLR Exemptions

The RBI did not stop at absorbing the hedging costs. To ensure banks aggressively wooed NRI depositors, the central bank implemented two more massive regulatory waivers:

Removal of Interest Rate Ceilings: Previously, the RBI strictly capped how much interest banks could offer on FCNR(B) deposits (usually tied to an Overnight Alternative Reference Rate plus a spread). Until September 30, 2026, the RBI has completely temporarily removed this interest rate ceiling for eligible 3-to-5-year deposits. Banks are now free to price these deposits as aggressively as they want.

CRR and SLR Exemptions: Normally, banks must keep a certain percentage of all deposits parked with the RBI as Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR), meaning they cannot lend out 100% of the money they raise. The RBI announced that any fresh FCNR(B) deposits mobilized between June 8 and September 30, 2026, are entirely exempt from CRR and SLR requirements. Banks can now deploy 100% of these funds into profitable lending avenues.

Freed from hedging costs, unconstrained by rate ceilings, and exempt from reserve requirements, Indian banks instantly passed these immense savings onto NRI depositors, resulting in the historic rate hike we see today.

Part 3: Exploring the FCNR(B) Rate Landscape (July 2026)

The banking sector’s response to the RBI’s June 8 announcement was instantaneous. Within days, banks across the spectrum—from mammoth public sector entities to agile small finance banks—revised their rate cards.

It is crucial to note that these hyper-elevated rates apply exclusively to deposits with tenures of 3 to 5 years mobilized before the RBI swap window closes on September 30, 2026. Deposits of 1 to 2 years do not qualify for the RBI swap and continue to offer lower, standard market rates (typically around 3.85% to 4.50%).

Here is a comprehensive breakdown of the current rate landscape for 3-to-5-year USD FCNR(B) deposits as of July 2026:

1. Small Finance Banks (SFBs): The Yield Maximizers

Small Finance Banks have been the most aggressive players in the market, utilizing the RBI window to attract high-net-worth NRIs and build a stable base of foreign currency liabilities.

AU Small Finance Bank: Leading the charge, AU SFB is offering an astonishing 7.10% per annum for 3-year USD deposits, and 7.00% for 4-to-5-year tenures.

Other SFBs: Banks like Equitas, Ujjivan, and ESAF are similarly positioned in the 6.75% to 7.15% bracket.

The Trade-off: While SFBs offer the absolute highest yields, they inherently carry a slightly higher risk profile than systemically important legacy banks. However, because FCNR(B) deposits are fundamentally backed by the strength of the bank's balance sheet (and technically insured up to ₹5 Lakhs by DICGC, though currency conversion applies during liquidation), many NRIs find the premium yield well worth the moderate counterparty risk.

2. Large Private Sector Banks: The Sweet Spot

For the vast majority of NRIs, large private sector banks represent the optimal balance between aggressive yields, institutional safety, and seamless digital banking infrastructure.

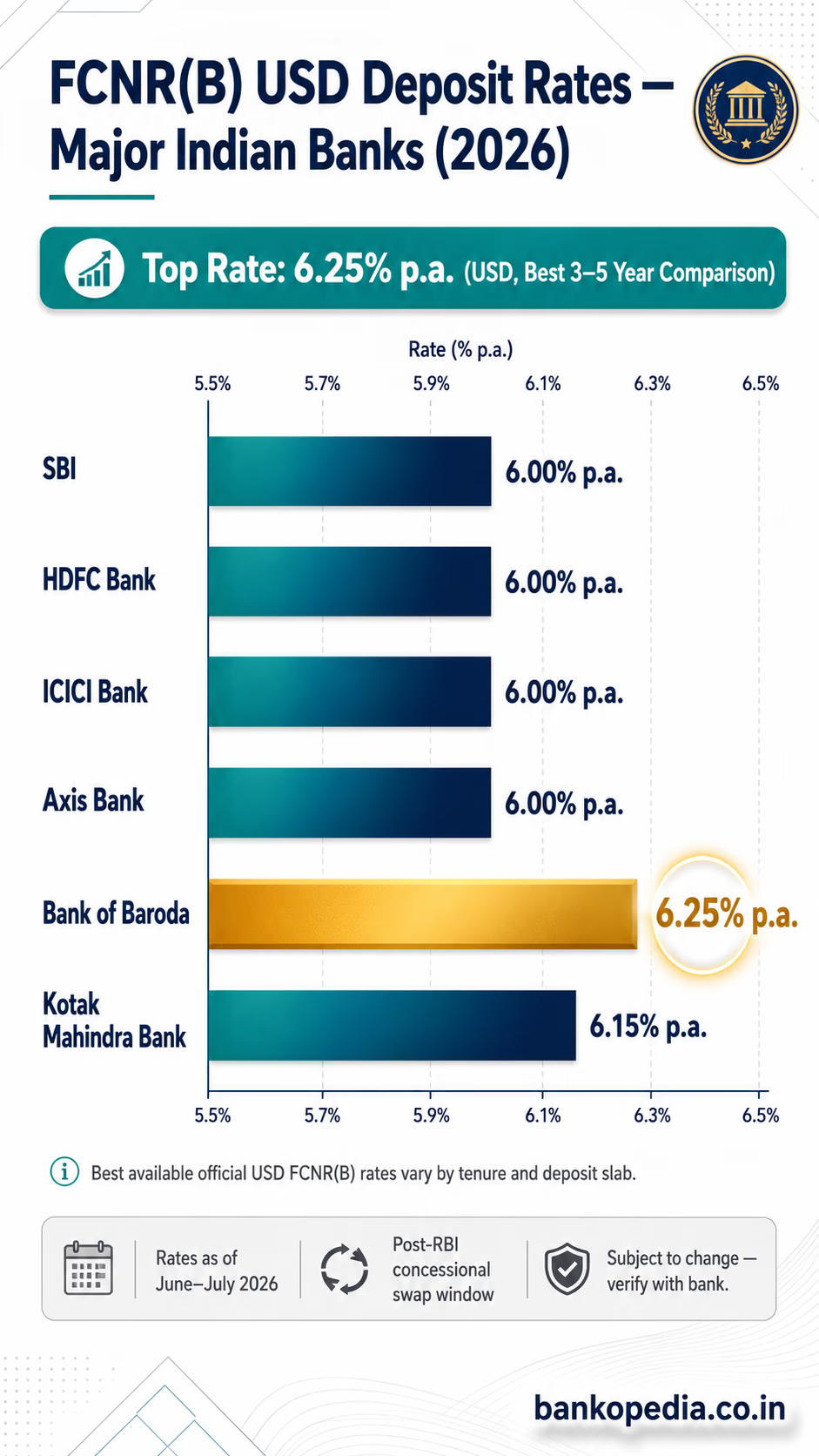

HDFC Bank, ICICI Bank, and Axis Bank: The private sector titans have unified their offerings, currently providing a flat 6.00% per annum across the 3, 4, and 5-year USD deposit buckets.

Kotak Mahindra Bank: Similarly offering highly competitive rates in the ~6.00% range for the 3-to-5-year window.

The Trade-off: While 100 basis points lower than the top-tier SFBs, a guaranteed 6.00% tax-free USD return from a Domestic Systemically Important Bank (D-SIB) like HDFC or ICICI is a historically rare opportunity that minimizes anxiety regarding the safety of principal.

3. Public Sector Banks (PSBs): Sovereign Safety

Public sector banks rely on their massive global footprint, sheer scale, and implicit sovereign backing to attract deposits, meaning they do not need to price as aggressively as private players.

Punjab National Bank (PNB): Offering a surprisingly competitive 6.10% per annum for 3-to-5-year tenures.

State Bank of India (SBI): The nation's largest lender is offering 5.25% for 3-to-4-year tenures and 6.00% for 5-year tenures (for deposits up to $1 million). Rates via SBI's GIFT City branch can sometimes offer slight variations.

(Disclaimer: Interest rates are dynamic and subject to change based on bank policies and asset-liability management requirements. Always verify the exact rate on the bank's official NRI portal immediately prior to booking.)

Part 4: The New Catch – Lock-Ins and Premature Withdrawals

The RBI’s generosity in absorbing hedging costs comes with strict stipulations designed to ensure the stability of this foreign capital. The central bank wants long-term, sticky money, not speculative hot money. Therefore, the special 2026 framework has introduced a rigorous lock-in period.

The Mandatory 1-Year Lock-In

Any FCNR(B) deposit booked under the special RBI swap window (3 to 5 years) carries a mandatory, non-negotiable 1-year lock-in period.

If a depositor attempts to withdraw the funds before the completion of 12 months, no interest will be paid whatsoever, and the bank may even levy a premature withdrawal penalty on the principal, depending on internal policies.

The RBI swap contract that the bank enters into is non-cancellable. Because the bank cannot unwind its position with the RBI, it absolutely will not allow early exits without severe punitive measures to cover its resulting mismatch.

Withdrawals After the First Year

Once the mandatory 1-year lock-in is completed, banks are permitted to allow premature withdrawals, but strict penal clauses apply. For example, under ICICI Bank’s published 2026 guidelines for deposits with original tenors of 36 to 60 months: If the deposit is prematurely withdrawn after the 1-year lock-in, the interest will be paid at the rate that was applicable on the date of booking for the period the deposit actually remained with the bank, minus a 1% penalty.

Strategic Advice: Do not park emergency funds or liquidity you might need within the next 3 to 5 years into these special FCNR(B) buckets. Only allocate capital that you are absolutely certain can remain untouched for the full duration of the tenure.

Part 5: Tax Efficiency and TDS – A Major Advantage

The headline interest rates of 6.00% to 7.10% are highly attractive on their own, but their true value is unlocked when viewed through the lens of taxation. FCNR(B) deposits are arguably the most tax-efficient instruments in the Indian banking system.

Absolute Exemption in India

Under Section 10(15)(iv)(fa) of the Income Tax Act, 1961, the interest income earned on FCNR(B) deposits is fully exempt from Indian income tax in the hands of a non-resident or an individual holding Resident but Not Ordinarily Resident (RNOR) status.

No TDS: Banks will not deduct any Tax Deducted at Source (TDS) on the interest accrued or paid out.

No ITR Requirement: If an NRI has no other taxable income in India, the interest earned on an FCNR(B) deposit alone does not trigger a requirement to file an Income Tax Return (ITR) in India.

Repatriability: Both the principal and the accumulated tax-free interest are fully and freely repatriable to your country of residence without requiring any special permissions from the RBI or a Chartered Accountant's certificate (15CA/15CB).

The Global Taxation Reality (US, UK, Canada, etc.)

While India gives you a free pass, your home country likely will not. The tax-free status in India does not magically erase your tax liabilities in the country where you are a tax resident.

United States: US tax residents (including Green Card holders and citizens) are taxed on their global income. The interest earned on an FCNR(B) deposit is fully taxable at standard federal and state income tax rates. Furthermore, FCNR(B) accounts must be reported to the IRS via the FBAR (FinCEN Form 114) if your aggregate foreign account balances exceed $10,000, and potentially via FATCA (Form 8938) depending on asset thresholds.

United Kingdom & Canada: Similar global taxation rules apply. You must declare this interest income on your local tax returns.

The Silver Lining: Because no tax is withheld in India, you do not have to navigate complex Foreign Tax Credit (FTC) claims to avoid double taxation. You simply pay your local taxes on the gross interest amount. Even after paying US or UK taxes, a 6.00% to 7.10% gross yield on a USD deposit massively outperforms standard savings rates in those domestic markets (which are actively falling as western central banks cut rates).

Part 6: FCNR(B) vs. NRE Accounts – The 2026 Mathematical Paradigm

The most common dilemma for an NRI is choosing between an NRE Fixed Deposit (denominated in INR) and an FCNR(B) deposit. Prior to June 2026, NRE deposits offered 7.00% to 7.50% while FCNR(B) offered ~4.00%. The wide 3.50% gap made NRE accounts tempting despite the currency risk.

However, with the RBI swap window pushing FCNR(B) rates to 6.00%–7.10%, the mathematical advantage has decidedly flipped in favor of the FCNR(B) account. Let us analyze why, using the concept of real currency-adjusted returns.

Understanding the Rupee Depreciation Factor

When you invest in an NRE deposit, you remit foreign currency, which is converted to INR. At maturity, if you wish to repatriate the funds, the INR is converted back to your foreign currency. Over the last two decades, the Indian Rupee has historically depreciated against the US Dollar at an annualized rate of roughly 2.50% to 3.50%.

A Real-World Calculation

Let us assume an NRI has $100,000 to invest for a 5-year tenure and has two options at a large private bank:

Assume the spot exchange rate today is 1 USD = ₹83.00.

Scenario A: The NRE Deposit

Remit $100,000. It converts to ₹8,300,000.

Invested at 7.25% p.a. (compounded quarterly) for 5 years.

Maturity Value in INR = Approximately ₹11,889,000.

Now, assume the INR depreciates by a conservative 3% per year against the USD. In 5 years, the exchange rate might be roughly 1 USD = ₹96.22.

Repatriation Value: ₹11,889,000 / 96.22 = $123,560. Effective Annualized USD Return: ~4.32%

Scenario B: The FCNR(B) Deposit

Remit $100,000 directly into the USD FCNR(B) account.

Invested at 6.00% p.a. (compounded half-yearly) for 5 years.

Maturity Value in USD = $134,391. Effective Annualized USD Return: 6.00% (Guaranteed)

The Verdict: Because the yield gap between NRE and FCNR(B) has shrunk to less than 1.50%, the NRE rate is no longer high enough to compensate for historical Rupee depreciation. If your ultimate goal is to retain your wealth in US Dollars, Pounds, or Euros, the FCNR(B) deposit is mathematically far superior in the current 2026 rate environment.

NRE deposits should now only be used for funds you explicitly plan to spend inside India (e.g., buying local real estate, supporting family, or funding retirement in India) where currency repatriation risk is not a factor.

Part 7: Practical Guide for NRIs – How to Maximize This Opportunity

If you have idle foreign currency sitting in low-yield savings accounts abroad, the current FCNR(B) landscape represents a generational opportunity to lock in high, risk-free yields. However, execution requires careful planning. Here is your actionable checklist:

Beat the September 30, 2026 Deadline: The RBI’s concessional swap facility is a temporary window. It explicitly closes for deposit mobilization on September 30, 2026. If you wait until October, banks will once again have to bear the 3% hedging costs, and FCNR(B) rates will plummet back down to the 3.50% - 4.50% range. Do not procrastinate.

Ensure Tenure Compliance: To qualify for these hyper-elevated rates (6.00%+), you must select a tenure between exactly 36 months (3 years) and 60 months (5 years). Selecting a 2-year and 364-day deposit will drop you into the standard, much lower rate bracket.

Optimize for Compounding: FCNR(B) interest is compounded half-yearly (every 180 days). When comparing rates across banks, look at the annualized yield, not just the nominal rate.

Evaluate Digital Account Opening: Most major Indian banks (HDFC, ICICI, Kotak, Axis) now offer fully digital, video-KYC-enabled account opening processes for NRIs. You do not need to physically visit an Indian branch or wait weeks for couriered documents to clear. Leverage these portals to secure rates quickly before the deadline.

Consult a Cross-Border Financial Advisor: While FCNR(B) interest is tax-free in India, the reporting requirements in your home country (especially the US) can be complex. A misstep in FBAR or FATCA reporting can lead to severe penalties that wipe out your interest gains. Always consult an advisor who understands the tax codes of both jurisdictions.

Conclusion

The Reserve Bank of India’s June 2026 intervention has drastically rewritten the rules of NRI banking. By eliminating hedging costs and suspending regulatory caps, the RBI has transformed the FCNR(B) deposit from a defensive, low-yield instrument into a powerhouse fixed-income asset.

Offering absolute protection against Rupee depreciation, total tax exemption in India, seamless repatriability, and yields that crush domestic western banking rates, the 3-to-5-year FCNR(B) deposit is currently the undisputed king of the NRI portfolio. With the window slamming shut on September 30, 2026, the time for NRIs to evaluate their liquidity and lock in these historic rates is right now.

(Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial, investment, or tax advice. Interest rates, RBI guidelines, and tax laws are subject to change. Readers should verify current rates directly with their respective banks and consult certified professionals before making any financial decisions.)