Form 26AS vs AIS: Understanding the Key Differences Every Indian Taxpayer Must Know

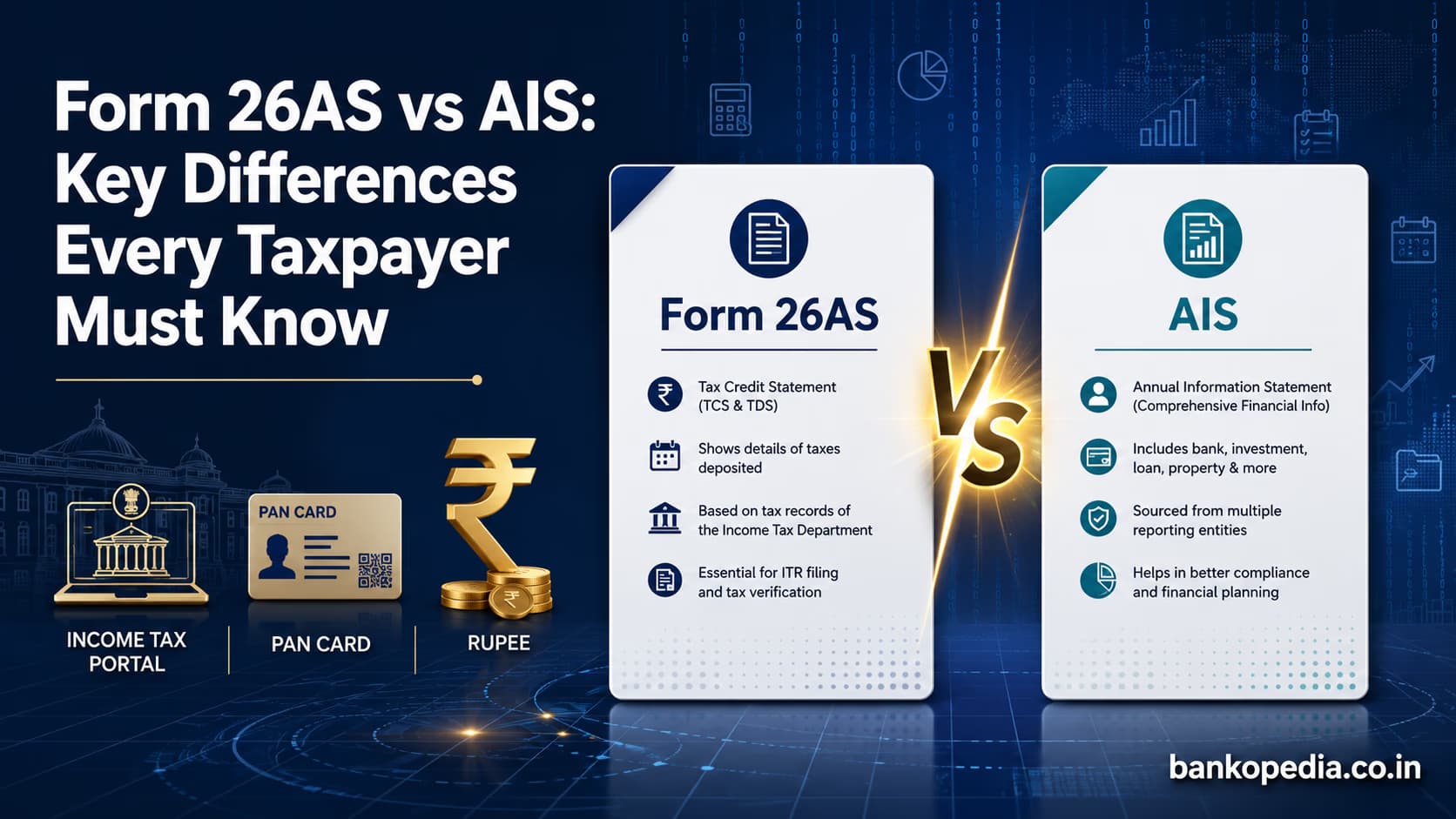

For decades, Form 26AS served as the cornerstone of tax compliance for millions of Indian taxpayers. It was the single most referenced document during the income tax return filing season — a consolidated statement that told you how much tax had been deducted at source, deposited with the government, and credited to your Permanent Account Number (PAN). But with the Income Tax Department's sweeping push toward greater transparency and data-driven compliance, the landscape has changed considerably. The Form 26AS AIS difference India taxpayers need to understand is not merely technical — it reflects a fundamental shift in how the government collects, processes, and presents financial information. The Annual Information Statement (AIS), whose portal rollout occurred on November 1, 2021, is significantly broader, deeper, and more consequential than its predecessor. Whether you are a salaried employee, a self-employed professional, a small business owner, or a high-net-worth individual, understanding this transition is now non-negotiable for clean, accurate tax compliance.

What Was Form 26AS and What Information Did It Contain?

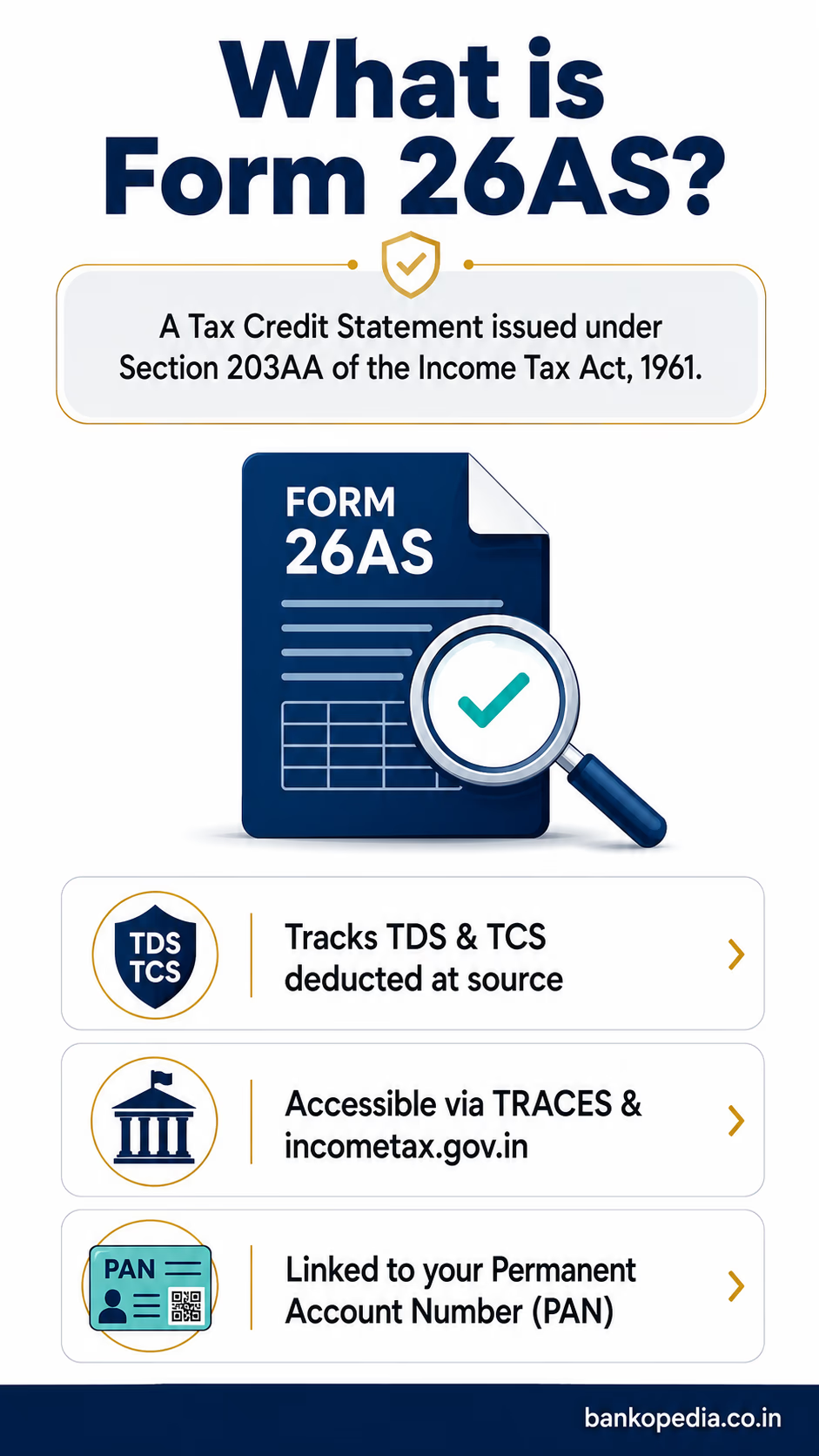

Form 26AS was essentially a tax credit statement issued by the Income Tax Department under Section 203AA of the Income Tax Act, 1961. It was accessible through the TRACES (TDS Reconciliation Analysis and Correction Enabling System) portal and, more recently, directly through the income tax e-filing portal at incometax.gov.in. For the average taxpayer, it was the go-to document to verify whether their employer, bank, or any other deductor had correctly deposited the TDS (Tax Deducted at Source) or TCS (Tax Collected at Source) amount with the government.

The information contained in Form 26AS was organised into clearly defined parts:

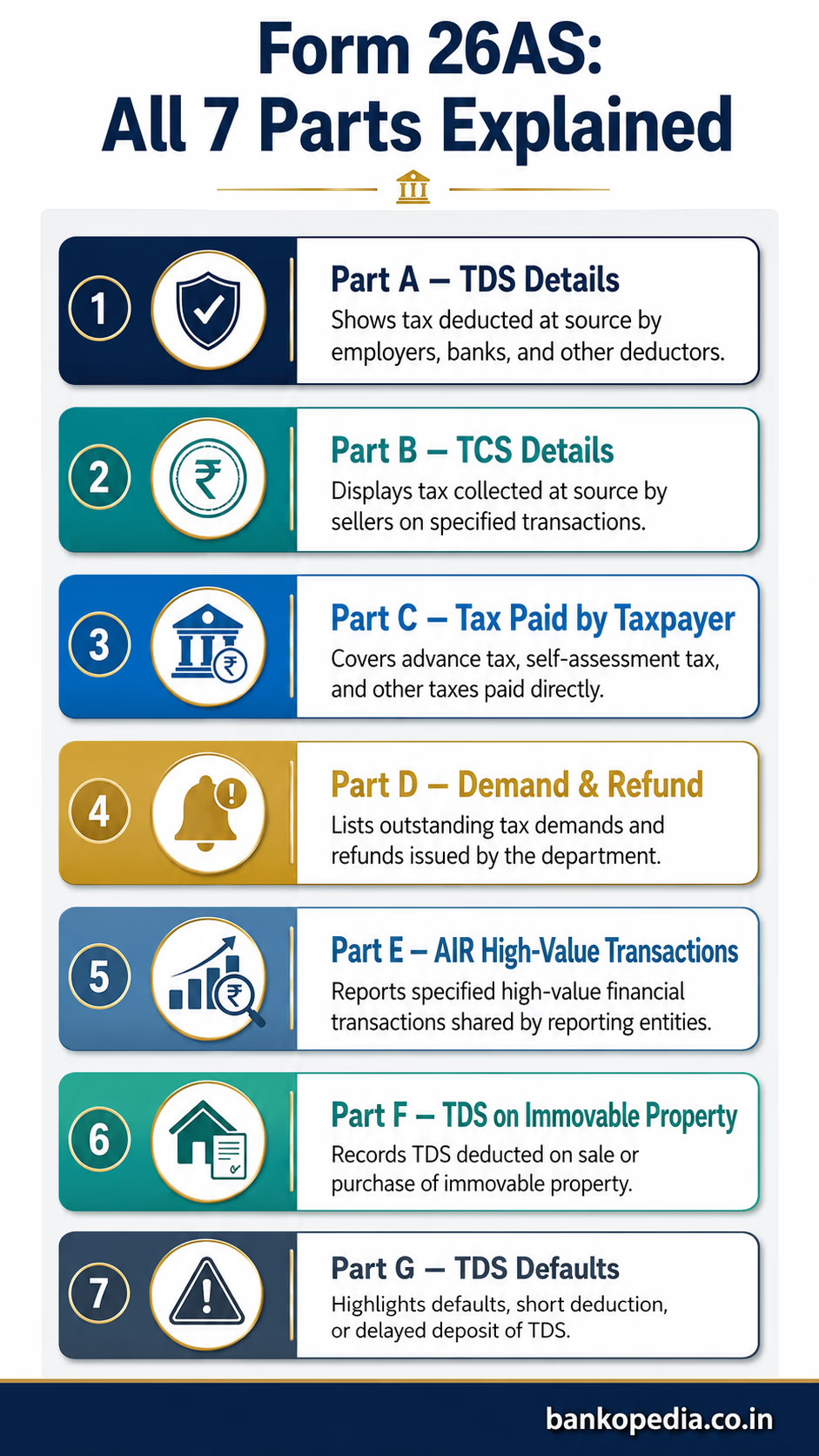

Part A – TDS Details: This section listed all TDS deductions made by employers, banks, and other entities on salary income, interest income, professional fees, rent, and other payments. It mentioned the deductor's name, TAN, the amount paid or credited, and the TDS amount deposited.

Part B – TCS Details: Tax Collected at Source by sellers of goods like motor vehicles, foreign exchange, or scrap was reflected here.

Part C – Tax Paid by Taxpayer: Self-assessment tax and advance tax payments made directly by the taxpayer were recorded in this section.

Part D – Demand and Refund Details: Any outstanding tax demand raised by the department or refunds issued to the taxpayer were captured here.

Part E – AIR (Annual Information Return) Details: High-value transactions such as large credit card payments, mutual fund investments, or property purchases were disclosed here by financial institutions and registrars under the Annual Information Return framework.

Part F – TDS on Sale of Immovable Property: Details of TDS deducted under Section 194IA for property transactions.

Part G – TDS Defaults: Defaults related to TDS processing by deductors were shown here.

Form 26AS was undeniably useful. It prevented taxpayers from missing TDS credits and helped reconcile discrepancies before filing returns. However, its scope was limited. It primarily tracked tax already deducted — it did not independently capture the full spectrum of a taxpayer's financial activity. A taxpayer could receive substantial income from dividends, sell shares, earn interest from bonds, or conduct significant real estate transactions, and much of this would go unreported in Form 26AS unless TDS had been deducted on it. This gap was exactly what the new Annual Information Statement was designed to close.

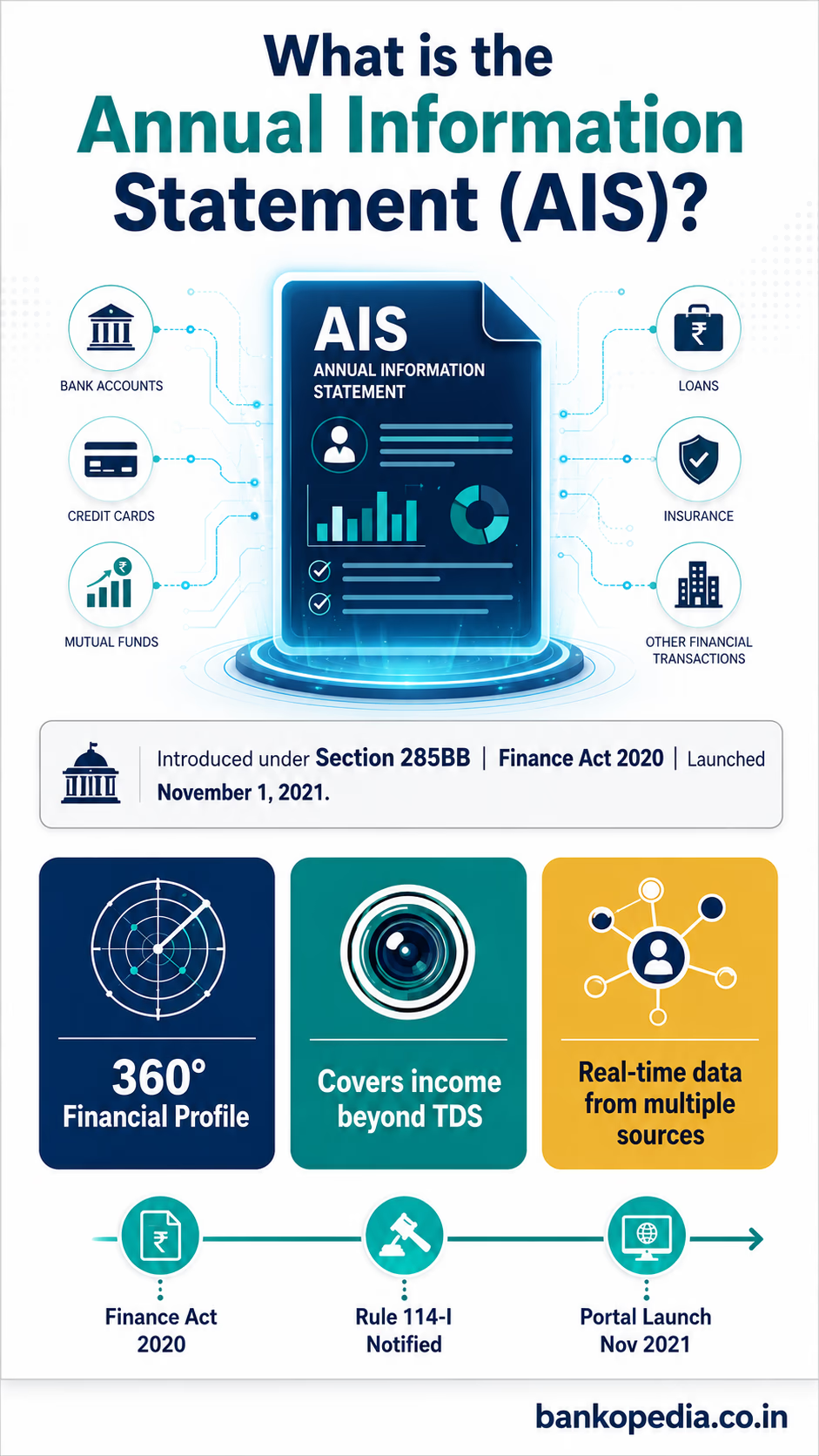

What Is the Annual Information Statement (AIS)?

The Annual Information Statement is a comprehensive financial profile of a taxpayer. Its legislative foundation was established under Section 285BB of the Income Tax Act, inserted by the Finance Act 2020. The specific rules governing AIS — Rule 114-I — were notified via Notification No. 30/2020 dated 28th May 2020. The AIS was made available to taxpayers on the income tax portal from November 1, 2021. It is accessible under the "Annual Information Statement" tab and presents information received by the Income Tax Department from a wide array of reporting entities — banks, mutual fund houses, registrars and sub-registrars, depositories, stockbrokers, and even foreign remittance processors.

The AIS is structured around two primary documents:

The AIS itself — which presents raw information reported by third parties about the taxpayer's financial transactions during the financial year.

The Taxpayer Information Summary (TIS) — which provides an aggregated, category-wise summary of the taxpayer's income and transactions, and is used by the system to pre-fill income tax returns.

The range of information captured in the AIS is substantially wider than anything Form 26AS ever attempted. The key categories of information in AIS include:

Salary income (reported by employers)

Rent received (reported by tenants deducting TDS)

Dividend income (reported by companies and mutual funds)

Interest from savings accounts, fixed deposits, recurring deposits, and bonds

Capital gains from sale of listed and unlisted securities, mutual fund units, and immovable property

Purchase and sale of immovable property

Foreign remittances received and sent (under LRS or otherwise)

Cash deposits and withdrawals above specified thresholds

Credit card spends above specified thresholds

GST turnover reported by businesses

Off-market credit transactions in demat accounts

Purchases of foreign currency

Receipts from life insurance policies

Critically, the AIS also provides a feedback mechanism. If a taxpayer believes that information reported in the AIS is incorrect, duplicated, or does not pertain to them, they can submit online feedback against each entry. The system accepts responses such as "Information is correct," "Information is not fully correct," "Information relates to other PAN/year," "Information is duplicate/included in other information," or "Information is denied." This interactive feature was absent in Form 26AS, which was a passive, read-only document.

"The AIS represents the Income Tax Department's most ambitious attempt yet at creating a unified, real-time financial mirror for every taxpayer — powered by data flows from dozens of regulated entities including banks supervised by the RBI, capital market intermediaries regulated by SEBI, and insurance companies overseen by IRDAI."

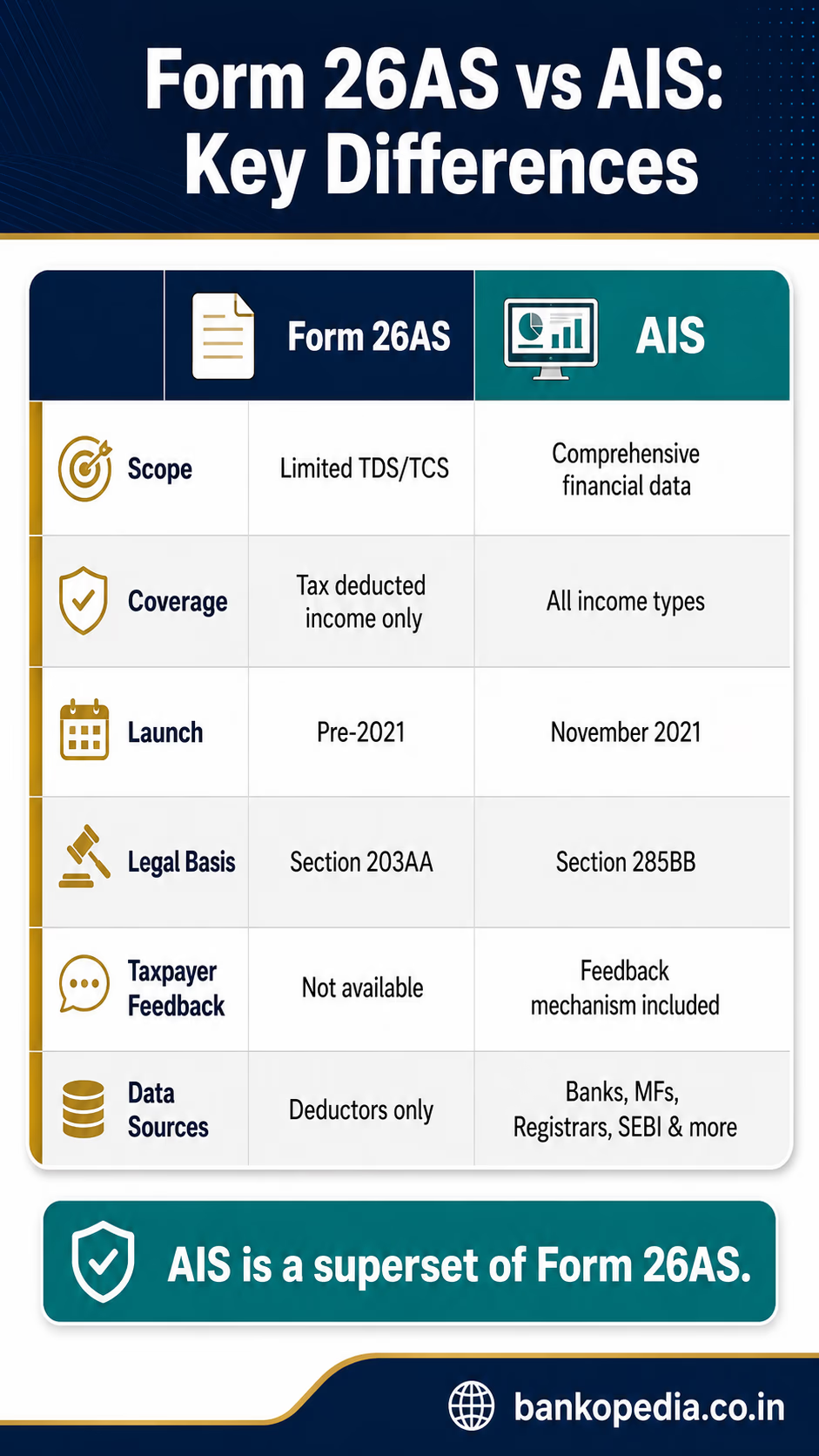

It is important to note that the government did not entirely abolish Form 26AS. Instead, it was restructured. The revised Form 26AS now functions as a trimmed document focusing on TDS/TCS credits, tax payments, demands, refunds, and pending proceedings. The detailed financial transaction data has been migrated to the AIS framework, making Form 26AS a subset, in functional terms, of the broader AIS ecosystem.

Key Differences Between Form 26AS and the New AIS

Understanding the Form 26AS AIS difference India taxpayers must navigate goes beyond a simple checklist. The two instruments differ in purpose, scope, interactivity, and their role in the compliance process.

1. Scope and Coverage

Form 26AS was narrowly focused on tax that had already been deducted or collected at source. AIS captures pre-tax and post-tax financial activity comprehensively — including transactions where no TDS was applicable. For example, interest on certain savings instruments, capital gains from equity mutual funds below the TDS threshold, or dividend income below ₹5,000 from a single company would not appear in Form 26AS but will appear in AIS because the paying entity reports it separately.

2. Data Sources

Form 26AS drew data almost exclusively from TDS/TCS returns filed by deductors. AIS aggregates data from a far larger ecosystem: Schedule AL returns, SFT (Statement of Financial Transactions) submissions by banks and financial institutions, SEBI-regulated brokers and depositories, sub-registrars for property transactions, the Directorate General of Foreign Trade, GST Network data, and information received under bilateral tax treaties. Given that RBI-regulated banks and SEBI-regulated intermediaries both feed into AIS, the coverage is extraordinarily wide.

3. Pre-filling of Returns

While Form 26AS was used informally to cross-check figures before filing, AIS data flows directly into the pre-filled ITR forms via the Taxpayer Information Summary (TIS). The system automatically populates fields for salary, interest, dividends, capital gains, and other income categories. This means errors in AIS — if not corrected through the feedback mechanism — can propagate directly into your pre-filled return.

4. Feedback and Correction Mechanism

Form 26AS offered no recourse if data was wrong. The only remedy was to contact the deductor and ask them to revise their TDS return. AIS, by contrast, has a built-in online feedback module. A taxpayer can flag incorrect entries directly, and the system stores both the original reported value and the taxpayer's response. This does not automatically correct the AIS but informs the Income Tax Department about disputed entries.

5. Capital Gains Reporting

This is arguably the most significant practical difference for investors. AIS reports sale and purchase values of listed securities, mutual fund units, and unlisted shares as reported by depositories like NSDL and CDSL and by registrar and transfer agents. Form 26AS had no comparable functionality. Taxpayers who trade actively in equities or mutual funds now have a ready reference in AIS to cross-verify their capital gains computations.

6. Cash Transaction Monitoring

Banks are required to report cash deposits of ₹10 lakh or more in savings accounts and ₹50 lakh or more in current accounts in a financial year under the SFT framework. This data, which feeds into AIS, helps the department flag disproportionate cash activity. Form 26AS captured a narrower version of this under Part E, but AIS brings in a more granular and real-time view.

7. Foreign Remittances

AIS now captures outward remittances under the Liberalised Remittance Scheme (LRS), which allows Indian residents to remit up to USD 2,50,000 per financial year for permitted purposes. Authorised dealer banks report these transactions to the department. This is a new addition that has no equivalent in Form 26AS.

How to Use AIS Correctly While Filing Your Income Tax Return

Filing an accurate income tax return in the post-AIS era requires a more active approach than simply downloading Form 26AS and reconciling TDS credits. Here is a structured methodology for using AIS effectively:

Step 1: Access and Download AIS Well Before the Filing Deadline

Log in to incometax.gov.in, navigate to "Annual Information Statement" under the Services menu, and download both the AIS (in PDF or JSON format) and the Taxpayer Information Summary. Do this at least four to six weeks before the return filing deadline to give yourself time to resolve discrepancies.

Step 2: Cross-Verify Each Category Against Your Own Records

Go through every income category systematically. Match salary figures against your Form 16. Reconcile interest income against bank passbooks and FD certificates. Check dividend income against your broker statements and company dividend advices. For capital gains, reconcile the buy and sell values reported in AIS against your own transaction records from your broker's contract notes.

Step 3: Submit Feedback for Incorrect or Duplicate Entries

If you find errors — for instance, a transaction that does not belong to your PAN, or a figure that is duplicated across two entries — use the feedback option in AIS. Select the most appropriate response category. Keep a record of the feedback you submit, as this creates an audit trail demonstrating your due diligence to the department.

Step 4: Do Not Wait for AIS Corrections Before Filing

A common misconception is that taxpayers must wait for AIS to be corrected before they can file their return. This is incorrect and potentially dangerous from a compliance standpoint. You should file your return based on the correct figures as per your own books and records, and note in your return (or in your records) any discrepancies flagged via feedback. The Income Tax Department has clarified that filing based on correct information is the taxpayer's responsibility even if AIS shows different figures.

Step 5: Use TIS for Cross-Checking Pre-filled Return Data

The Taxpayer Information Summary aggregates and deduplicates the raw AIS data. Before accepting the pre-filled return, verify that TIS values match your own computed income. Discrepancies between TIS and your records should be investigated — they may indicate either an error in third-party reporting or an income item you have inadvertently missed.

Step 6: Retain Documentation

Given the expanded reporting infrastructure, the likelihood of the Income Tax Department issuing compliance notices for apparent discrepancies between AIS data and filed returns has increased. Maintain proper documentation — bank statements, broker contract notes, mutual fund account statements, property sale deeds, and insurance surrender documents. Because AIS inherently tracks high-value transactions, a tiered retention strategy is advisable. Under Rule 6F, the standard statutory minimum is six years from the end of the relevant assessment year. However, following amendments to Section 149 of the Income Tax Act, the department can reopen assessments up to 10 years from the end of the relevant assessment year where income escaping assessment amounts to ₹50 lakh or more. Cases involving foreign assets attract an even longer window. The recommended retention periods are as follows:

Situation | Safe Retention Period (from end of Assessment Year) |

|---|

Standard tax filings | 6 Years |

High-value transactions (≥ ₹50 lakh) | 10 Years |

Cases involving foreign assets | 16 Years |

Conclusion: A More Transparent, More Demanding Compliance Environment

The transition from Form 26AS to the Annual Information Statement is not merely an administrative upgrade — it signals a decisive step toward a fully data-integrated tax ecosystem in India. Powered by information flows from RBI-regulated banks, SEBI-regulated capital market intermediaries, IRDAI-regulated insurance companies, and a host of other reporting entities, AIS gives the Income Tax Department an unprecedented composite view of every taxpayer's financial life.

For Indian banking professionals, financial advisors, and compliance officers, understanding the Form 26AS AIS difference India presents is now a core professional competency. Clients — whether retail investors, HNIs, or corporate treasurers — will increasingly look to their financial institutions and advisors to help them navigate AIS discrepancies, understand what is being reported, and ensure that their tax filings are consistent with the data the department already holds.

As India's digital financial infrastructure matures — and as the government continues to invest in real-time data linkages between the tax system, the banking system, and capital markets — the era of passive compliance is firmly behind us. The AIS is not just a document to download before July 31; it is a living record of your financial year that demands active engagement, timely review, and careful reconciliation. Taxpayers and professionals who treat it as such will find the filing process cleaner, faster, and far less likely to attract unwanted scrutiny.