Introduction: A Smarter Way to Unlock Liquidity Without Selling Your Investments

For millions of Indian investors who have steadily built mutual fund portfolios over the years, a sudden need for liquidity often triggers a difficult choice: redeem units and lose out on long-term compounding, or take on an expensive personal loan. There is, however, a third path that remains significantly underutilised — a loan against mutual funds India investors can avail from banks and NBFCs by pledging their existing holdings as collateral. This facility allows you to access funds at relatively lower interest rates while keeping your investment intact and continuing to earn returns. With India's banking system demonstrating remarkable resilience — experts have noted its robustness even amid global uncertainties such as the West Asia crisis and fluctuating forex reserves — lenders have shown increasing appetite for offering such secured credit products. This guide unpacks everything you need to know about loans against mutual funds, from how the mechanism works to the risks you must not overlook.

What Is a Loan Against Mutual Funds and How Does It Work?

A loan against mutual funds (LAMF) is a secured credit facility wherein an investor pledges their mutual fund units to a lender — typically a bank or a Non-Banking Financial Company (NBFC) — as collateral in exchange for a loan or overdraft facility. The investor does not sell or redeem the units; instead, a lien is marked on the pledged units by the Asset Management Company (AMC) in favour of the lender.

The underlying mechanics are straightforward. When you pledge your units, the AMC — regulated by the Securities and Exchange Board of India (SEBI) — restricts redemption of those specific units until the lien is released upon full repayment of the loan. The lender, in turn, disburses funds based on the current Net Asset Value (NAV) of the pledged units, subject to a prescribed Loan-to-Value (LTV) ratio.

Most lenders structure LAMF as an overdraft (OD) facility rather than a term loan. This means the borrower is given a sanctioned credit limit and pays interest only on the amount actually drawn, making it a highly cost-efficient arrangement for managing temporary cash-flow needs. Some lenders do offer it as a term loan, but the OD structure is far more common and practical.

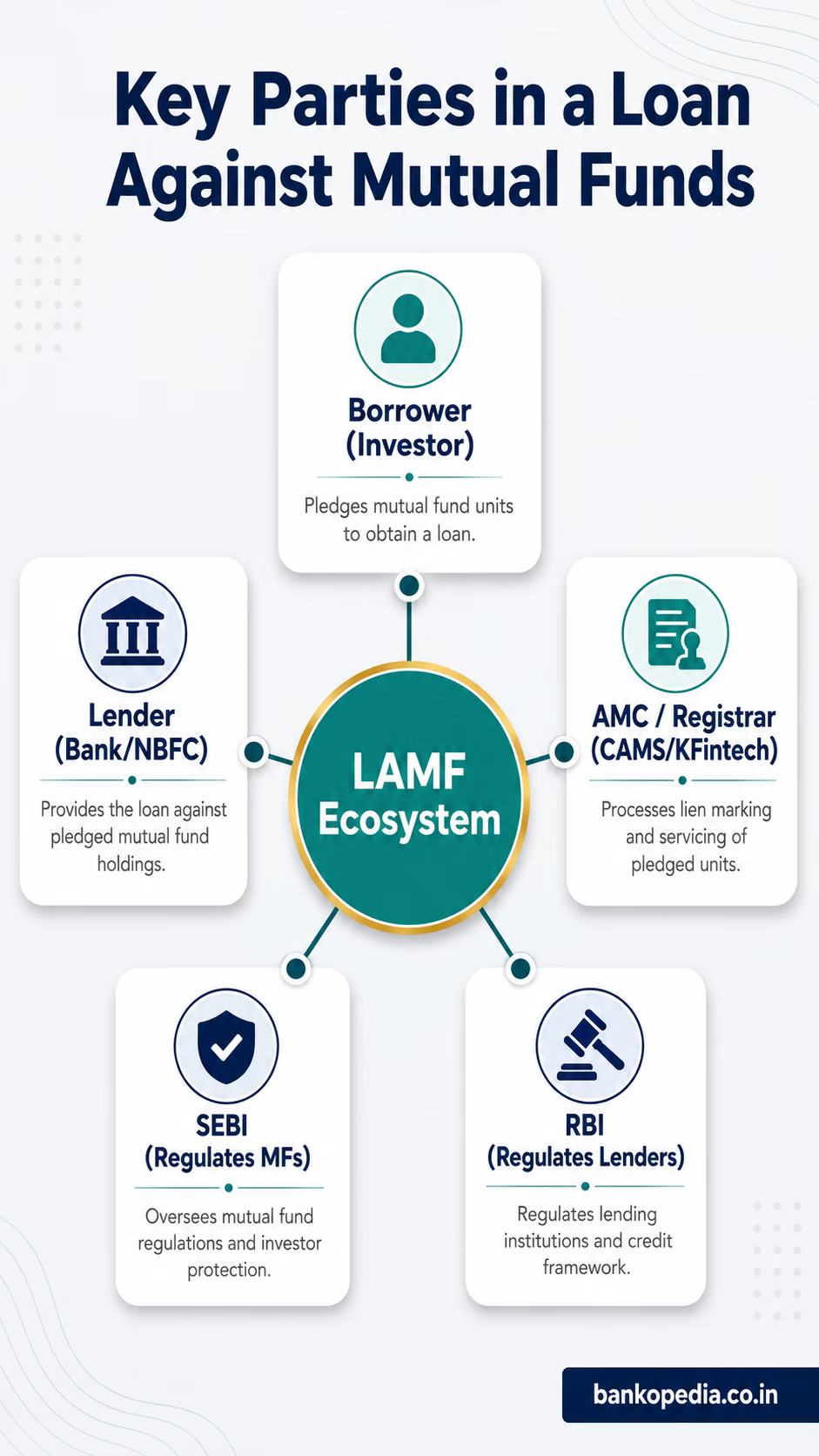

Key Parties Involved

Borrower: The mutual fund investor who pledges units

Lender: A scheduled commercial bank or registered NBFC

AMC/Registrar: The fund house or its registrar (CAMS or KFintech) that marks and releases the lien

SEBI: Regulates mutual funds and the pledge mechanism

RBI: Regulates lending institutions and prescribes guidelines on lending against securities

It is worth noting that the Reserve Bank of India (RBI) has issued specific guidelines — most notably through its Master Circular on Loans and Advances — governing how banks may lend against the security of mutual fund units, including restrictions on concentration of exposure and LTV norms. Banks must ensure compliance with these norms while structuring LAMF products.

Which Banks and NBFCs Offer Loans Against Mutual Funds in India?

The LAMF ecosystem in India has matured considerably, with both public sector banks and private lenders offering competitive products. Here is a snapshot of the major players:

Public Sector Banks

State Bank of India (SBI): Offers loans against units of mutual funds under its securities lending portfolio, typically structured as an OD facility

Bank of Baroda: Provides OD against mutual fund units with a relatively streamlined digital process

Punjab National Bank (PNB): Offers term loans and OD facilities against mutual fund holdings

Canara Bank: Has a structured product for lending against MF units, particularly for existing account holders

Private Sector Banks

HDFC Bank: One of the most widely used lenders for LAMF, with a robust digital pledge mechanism integrated with CAMS and KFintech

ICICI Bank: Offers a fully digital OD against mutual funds with fast processing

Axis Bank: Provides instant OD against MF units through its digital banking platform

Kotak Mahindra Bank: Competitive rates with a smooth lien-marking process

NBFCs and Fintech Lenders

Bajaj Finance: A prominent NBFC offering loans against mutual funds with a largely paperless process

Tata Capital: Provides LAMF with competitive interest rates

Mirae Asset Financial Services: Offers digital LAMF products linked to its AMC ecosystem

Fintech platforms such as Groww, Zerodha (through partnerships), and Orowealth: Have enabled or facilitated LAMF for retail investors through tie-ups with NBFCs

Interest rates across lenders typically range from 9% to 13% per annum for equity fund pledges and can be marginally lower for debt fund pledges, which are considered less volatile. NBFCs may charge slightly higher rates than banks, but often compensate with faster disbursements and more flexible eligibility criteria.

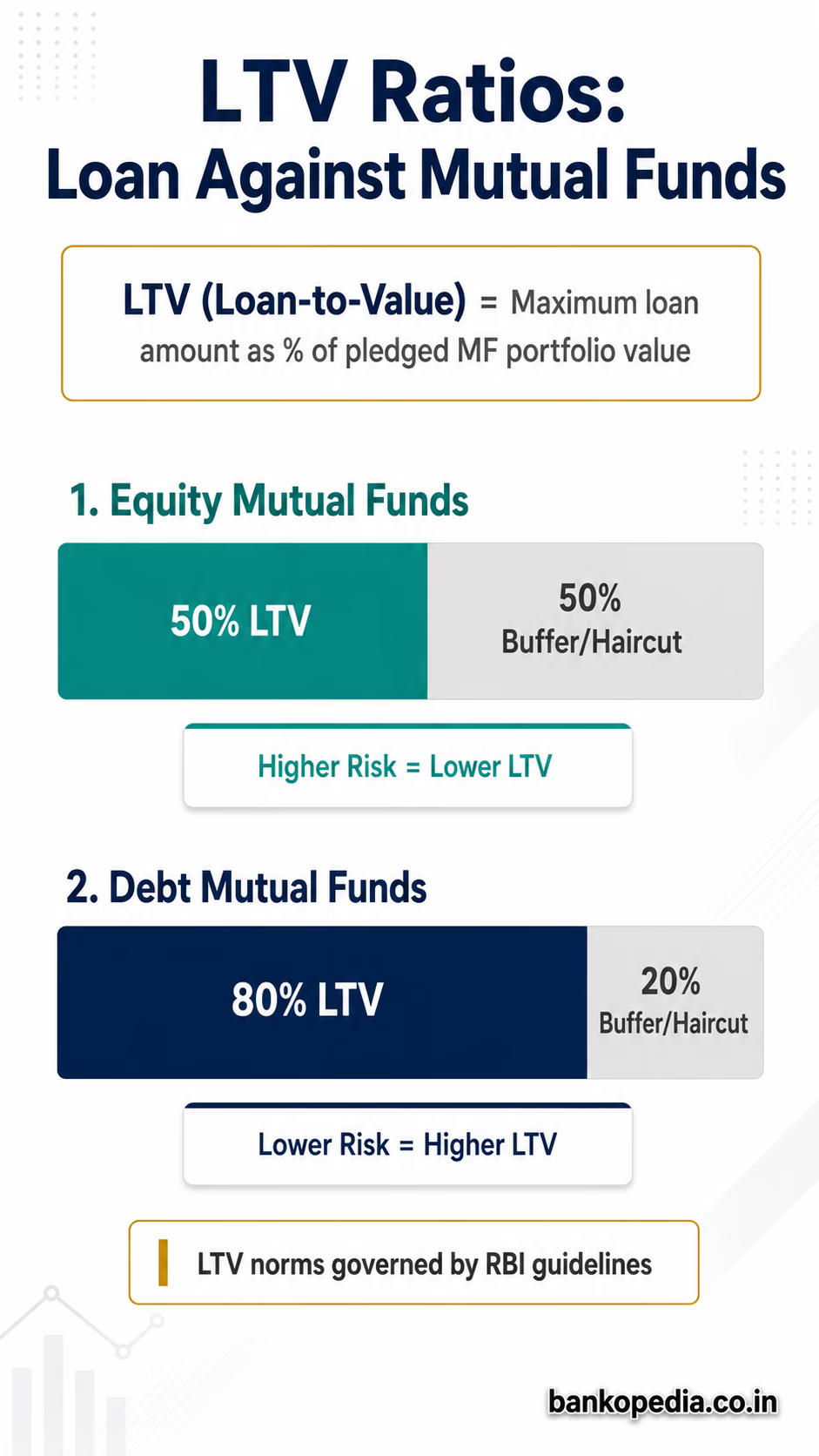

Loan-to-Value (LTV) Ratios: How Much Can You Borrow Against Your MF Units?

The LTV ratio is arguably the most critical parameter in any LAMF arrangement. It determines what percentage of your mutual fund's current market value you can borrow. The RBI and lenders themselves set LTV limits based on the nature and risk profile of the underlying fund category. Importantly, following the RBI's February 2026 revision, the regulatory caps on LTV for mutual fund loans were significantly increased, providing retail investors with greater liquidity potential against their portfolios. Individual lenders may still choose to apply more conservative internal limits within these enhanced caps.

Standard LTV Norms (Post-February 2026 RBI Revision)

Equity Mutual Funds: The RBI-prescribed maximum LTV cap is now up to 75% of the current NAV-based value. While lenders may apply internal limits below this ceiling, the revised cap reflects a greater regulatory confidence in equity fund collateral and provides investors with significantly more borrowing headroom than before.

Debt Mutual Funds: The RBI-prescribed maximum LTV cap has been raised to up to 85%, as debt funds exhibit lower NAV fluctuations and are considered relatively stable collateral. This enhancement makes debt fund pledges an even more powerful liquidity tool for investors.

Hybrid / Balanced Funds: LTV generally falls in the 60% to 70% range, reflecting their blended risk profile.

ELSS (Equity Linked Savings Schemes): Most lenders do not accept ELSS units as collateral while they are within the mandatory three-year lock-in period. After the lock-in, they are treated like regular equity funds.

Liquid Funds and Overnight Funds: These may attract LTVs of up to 80–85%, given their near-money market nature.

Illustrative Example: If you hold equity mutual fund units currently valued at ₹10,00,000 and the lender applies a 75% LTV (the revised regulatory cap), your maximum loan eligibility could be up to ₹7,50,000 — a substantial improvement over earlier caps. If NAV falls and the portfolio value drops to ₹8,00,000, your eligible limit adjusts accordingly, and if you have drawn more than the revised threshold, you face a margin call.

It is critical to note that RBI guidelines explicitly cap the total exposure of a bank to the capital market through loans against shares, debentures, bonds, and mutual fund units. Banks must monitor LTV on an ongoing basis; if the portfolio value declines below the required threshold, borrowers are expected to either repay a portion of the loan or provide additional collateral — commonly known as a margin call or top-up requirement.

Step-by-Step Process to Pledge Mutual Fund Units for a Loan

The process of availing a loan against mutual funds has become significantly more digital and borrower-friendly in recent years, largely driven by CAMS and KFintech enabling online lien-marking. Here is a step-by-step overview of how it works:

Choose Your Lender and Check Eligibility: Identify a bank or NBFC that accepts your specific mutual fund scheme as collateral. Not all AMCs are empanelled with all lenders. Confirm that the lender's platform integrates with your fund's registrar — either CAMS or KFintech.

Submit Loan Application: Apply online or at a branch. You will need to provide basic KYC documents (PAN, Aadhaar, address proof), details of your mutual fund portfolio, and bank account information for disbursement.

Portfolio Evaluation: The lender evaluates your portfolio based on eligible scheme categories and current NAV. The sanctioned OD or loan limit is calculated using the applicable LTV ratio.

Lien Marking Request: The lender submits a lien-marking request to the AMC or its registrar (CAMS/KFintech). This is increasingly done digitally. The investor typically receives an OTP-based confirmation or an email/SMS to authenticate the pledge request.

AMC Confirms Lien: Once the AMC marks the lien on the specified units, it sends a confirmation to both the lender and the borrower. At this stage, those units cannot be redeemed until the lien is released.

Loan/OD Account Activation: Upon receiving lien confirmation, the lender activates the OD facility or disburses the term loan amount to your designated bank account, often within 24–72 hours.

Utilise and Repay: In an OD structure, you draw funds as needed and repay at your convenience, paying interest only on the utilised amount. Timely repayment leads to lien release.

Lien Release on Full Repayment: Once the loan is fully repaid, the lender instructs the AMC to release the lien, and your units are restored to full tradeable status.

Several leading lenders have now made the entire journey — from application to lien marking to disbursement — a fully paperless, end-to-end digital process completable within a few hours. This is a significant improvement over the cumbersome physical pledge documentation required even a decade ago.

Risks, Hidden Charges, and When a Loan Against MF Makes Sense

While LAMF is an elegant financial tool, it is not without its risks and costs. A clear-eyed assessment is essential before pledging your hard-earned investments.

Key Risks to Understand

Market Risk and Margin Calls: The most significant risk is NAV volatility, especially for equity fund pledges. A sharp market correction — such as a sudden geopolitical shock or a broad market sell-off — can erode the collateral value and trigger a margin call. If you are unable to top up collateral or repay, the lender has the right to liquidate your pledged units.

Forced Redemption Risk: In a worst-case scenario, if the borrower defaults and the lender liquidates the units at a depressed NAV, the investor not only loses the investment but may also have residual debt if the proceeds do not cover the outstanding loan.

Over-Leveraging Risk: The ease of accessing funds against mutual funds — further amplified by the higher LTV caps introduced in February 2026 — can tempt investors to over-leverage, effectively using long-term savings to fund short-term consumption or speculative activity. The enhanced borrowing headroom makes financial discipline even more important.

Opportunity Cost During Lien Period: Pledged units cannot be switched to other schemes, redeemed, or used for STP/SWP until the lien is released, potentially causing you to miss rebalancing opportunities.

Interest Rate Risk: Many LAMF products come with floating interest rates linked to the lender's benchmark. A rising rate environment can push up borrowing costs.

Hidden and Associated Charges

Processing Fee: Typically 0.25% to 1% of the loan amount, sometimes subject to a minimum flat fee. Notably, many new-age fintechs and digital banking platforms now offer LAMF with flat-fee processing (e.g., ₹499 to ₹999) or occasionally waive it entirely during promotional periods to attract retail investors.

Lien Marking and Release Charges: Some lenders charge a nominal fee for the lien-marking and release process

Non-Utilisation Charges: In OD facilities, certain lenders charge a fee on the unutilised portion of the sanctioned limit

Penal Interest: Late repayment or breach of LTV covenants can attract penal interest, often 1–2% above the contracted rate

Renewal Fees: OD facilities are typically renewed annually and may carry a renewal charge

When Does a Loan Against Mutual Funds Make Sense?

Despite these risks, LAMF is genuinely advantageous in several scenarios:

Short-term liquidity crunch: Medical emergencies, bridge funding for a property purchase, or a temporary business cash-flow gap where you expect repayment capacity within weeks or a few months

Avoiding premature redemption penalties or exit loads: Many equity funds levy exit loads for redemptions within one year. Pledging instead of redeeming saves this cost

Tax efficiency: Following the July 2024 Union Budget, redemption of equity mutual funds held for over one year now attracts Long-Term Capital Gains (LTCG) tax at 12.5% (above the revised exemption threshold of ₹1.25 lakh). A loan does not trigger any tax event, making it significantly more efficient when your portfolio is sitting on large gains — and with the higher LTCG rate, the tax-saving advantage of pledging over redeeming is now even more compelling than before.

Preserving the compounding effect: For investors in the wealth accumulation phase, retaining investment in a rising market while borrowing at 10–11% can be mathematically superior to exiting a fund delivering 14–16% CAGR

Cost advantage over personal loans: Personal loans in India currently carry interest rates of 12–24% per annum. LAMF at 9–12% offers a meaningful cost benefit for creditworthy borrowers

Maximising the revised LTV benefit: With the RBI's February 2026 hike in LTV caps — up to 75% for equity funds and 85% for debt funds — LAMF is now an even more powerful liquidity tool, enabling investors to unlock a larger proportion of their portfolio value without triggering a redemption or tax event.

Conclusion: A Powerful Tool, Best Used with Discipline

A loan against mutual funds represents one of the most sophisticated and cost-effective secured credit options available to Indian investors today. It bridges the gap between long-term wealth creation and short-term liquidity needs without dismantling your investment portfolio. The growing digital infrastructure — anchored by CAMS, KFintech, and an increasingly tech-forward banking sector — has made LAMF more accessible than ever before. The RBI's February 2026 upward revision of LTV caps to 75% for equity funds and 85% for debt funds further strengthens the case for LAMF as a mainstream liquidity tool, allowing investors to borrow more meaningfully against their portfolios than was previously permissible.

However, this facility demands financial discipline and a clear repayment plan. The same market forces that make mutual funds a wealth-building vehicle can turn pledged units into a liability trap in the absence of prudent risk management. Borrowers should rigorously assess their repayment capacity, avoid over-leveraging, and treat LAMF as a bridge — not a crutch.

As India's credit culture matures and more investors build sizable MF portfolios, the loan against mutual funds India landscape is poised to grow substantially. For the informed investor who uses it judiciously, it remains one of the smartest ways to access liquidity without sacrificing the future.

Always read the fine print of your lender's LAMF product document and consult a registered financial advisor before pledging your mutual fund units as collateral.