Gold Monetisation Scheme India Explained: A Complete Guide for Investors and Banking Professionals

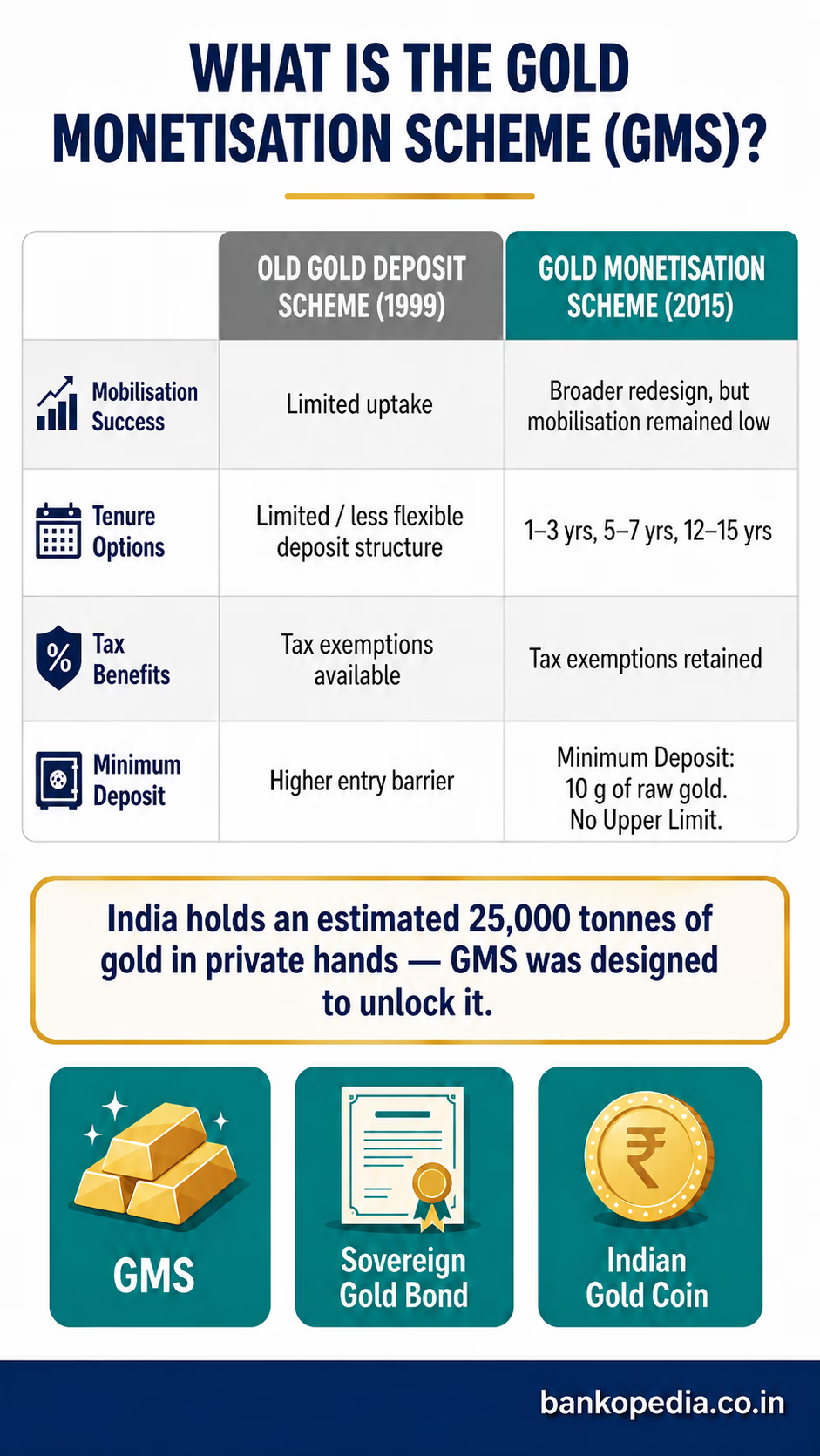

India holds an estimated 25,000 tonnes of gold in private hands — accumulated across generations in households, temples, trusts, and small businesses. This stockpile, worth several trillion rupees at current market prices, sits largely idle, generating no financial return for its owners and no productive utility for the broader economy. The Gold Monetisation Scheme India explained in this article represents one of the government's most ambitious attempts to change that equation. Launched in 2015, the Gold Monetisation Scheme (GMS) was designed to unlock this dormant wealth, channel it into the formal banking system, and reduce India's dependence on gold imports — which consistently rank among the country's largest contributors to its current account deficit. A decade on, however, the scheme has mobilised only around 39 tonnes of gold, a figure that underscores both the structural challenges of formalising household gold and the gaps in the scheme's design that still need urgent attention.

What Is the Gold Monetisation Scheme and How Did It Start

The Gold Monetisation Scheme was formally launched by the Government of India in November 2015, replacing an older and largely unsuccessful Gold Deposit Scheme (GDS) that had been in existence since 1999. The GDS had mobilised barely 15 tonnes of gold over 16 years — a failure that made it clear a more comprehensive and accessible framework was needed.

The GMS was introduced as part of a broader package of gold-related reforms that also included the Sovereign Gold Bond (SGB) Scheme and the Indian Gold Coin programme. Together, these initiatives aimed to shift Indian households away from physical gold ownership toward financial instruments that could serve similar purposes — wealth preservation, investment, and collateral — while simultaneously mobilising gold into productive use.

The Reserve Bank of India (RBI) serves as the regulatory backbone of GMS, issuing operational guidelines and overseeing participating banks. The scheme is operationally implemented through designated banks — currently a select set of scheduled commercial banks that have been authorised by RBI to accept gold deposits, including public sector banks like State Bank of India, Bank of Baroda, and Canara Bank.

The Core Objective: Reducing the Gold Import Bill

India imports between 700 and 1,000 tonnes of gold annually, making it one of the world's largest gold importers. This has a direct and significant impact on the current account deficit and, consequently, on the value of the Indian rupee. The GMS was conceived with the idea that if even a fraction of the estimated 25,000 tonnes held in private hands could be mobilised through banks, it could reduce the need for fresh imports, decrease pressure on foreign exchange reserves, and inject liquidity into the gold supply chain — including jewellers and refineries who currently rely on import channels.

"The idle gold lying in Indian households is not just a missed financial opportunity for families — it is a macroeconomic inefficiency that GMS was designed to correct. Getting this right matters for the rupee, for the current account, and for financial inclusion."

How GMS Differs from Simply Pawning Gold

It is important to distinguish GMS from gold loans or pledging gold with non-banking financial companies (NBFCs). Under a gold loan, the depositor retains ownership but surrenders physical possession as collateral; they must repay the principal and interest to get the gold back. Under GMS, the depositor actually transfers the gold to the bank in exchange for a gold-denominated interest-bearing account. The depositor does not need to repay anything — instead, they earn interest, and at maturity, they receive either gold of equivalent weight or cash at prevailing gold prices.

How to Deposit Gold Under GMS: Eligibility and Process

Understanding the operational process is essential for any banking professional advising clients on GMS or for investors considering participation. The mechanics involve several steps and multiple stakeholders.

Who Can Deposit Gold?

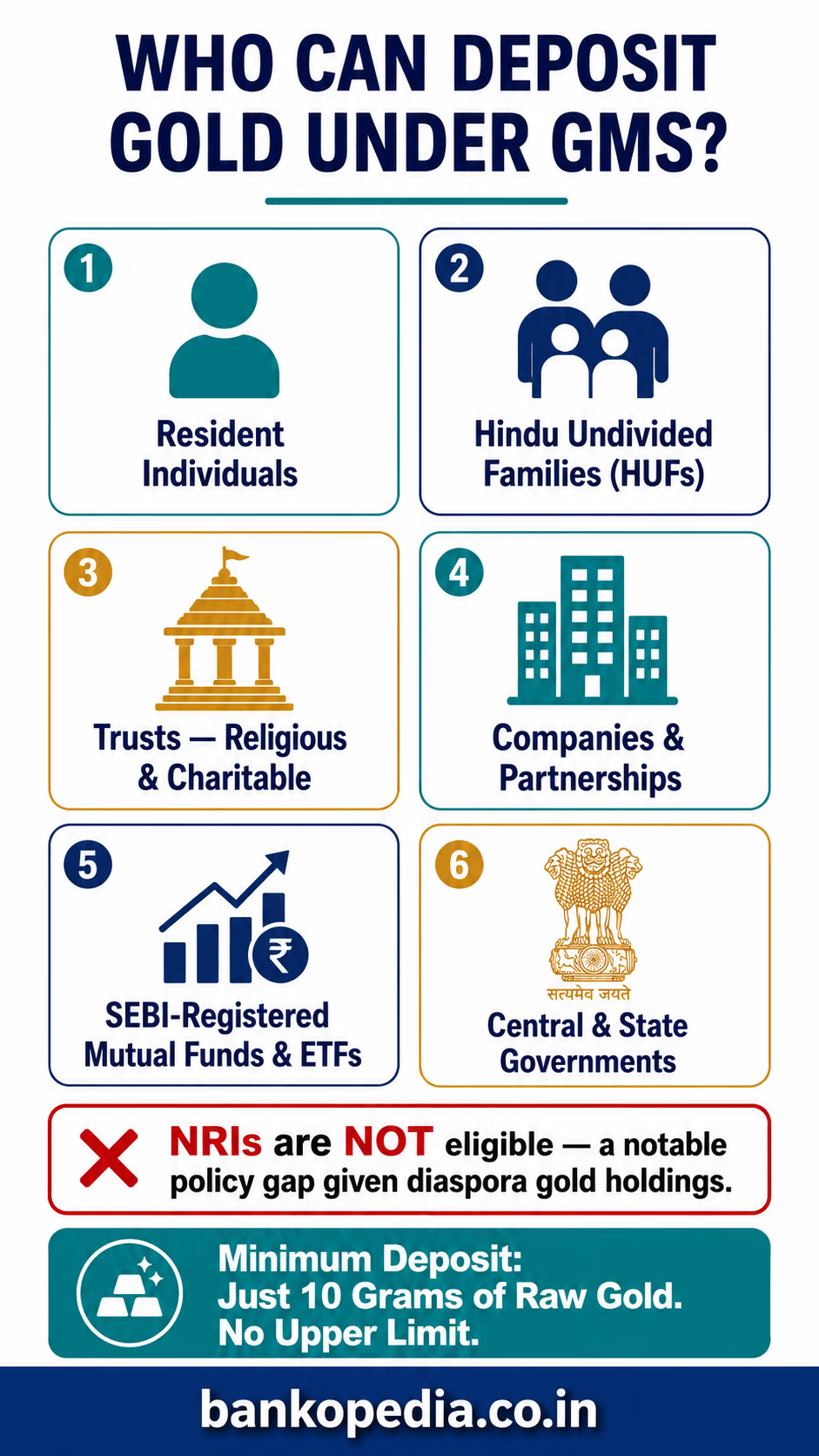

The scheme is open to a broad category of depositors, including:

Resident Indians — individuals, Hindu Undivided Families (HUFs), and proprietorship firms

Trusts, including religious and charitable trusts (this is significant, as many large temple trusts hold hundreds of kilograms of gold)

Companies and Partnerships registered in India

Mutual Funds and Exchange Traded Funds registered under SEBI

Central and State Governments and their undertakings

Non-resident Indians (NRIs) are currently not eligible to participate in GMS, which is a notable exclusion given the substantial gold holdings of the Indian diaspora.

Minimum and Maximum Deposit

The minimum quantity of gold that can be deposited is 10 grams of raw gold (bars, coins, or jewellery). There is no upper limit on the quantity that can be deposited. Gold can be in the form of jewellery, coins, or bars, including gold with embedded stones — though stones and other non-gold material will be separated and returned to the depositor at the time of deposit.

The Deposit Process: Step by Step

Approach a Collection and Purity Testing Centre (CPTC): The depositor first takes their gold to a Bureau of Indian Standards (BIS)-certified Collection and Purity Testing Centre. These centres are typically located at designated bank branches or at affiliated testing laboratories. The gold is tested for purity using fire assay or karat metres.

Receive a Purity Certificate: After testing, the depositor receives a certificate specifying the weight and purity of the gold. This forms the basis of the deposit.

Open a Gold Savings Account: Based on the purity certificate, the depositor opens a Gold Savings Account with a designated bank. The account is denominated in grams of gold, not in rupees.

Gold is Melted and Sent to Refineries: The deposited gold is melted, refined, and either held by the bank or supplied to jewellers, the RBI's gold reserves, or used in other approved ways. The depositor's original physical gold is not returned in its original form — this is a critical point that many households find psychologically difficult to accept.

Interest Credited: Interest begins accruing on the account, either in gold grams or in rupee equivalent, depending on the tenure chosen and the bank's policy.

Role of BIS and Refineries

The Bureau of Indian Standards plays a crucial quality assurance role in the GMS ecosystem. Only BIS-certified CPTCs are authorised to test and certify gold purity for GMS purposes. Separately, RBI-empanelled refineries handle the melting and conversion of deposited jewellery into standard gold bars. The entire back-end logistics chain — from CPTC to refinery to bank vault — is a system that requires coordination across multiple agencies, which partly explains the scheme's operational friction.

Interest Rates, Tenure, and Tax Benefits of GMS

From a purely financial standpoint, the GMS offers a structured set of returns and significant tax advantages — though awareness of these benefits remains surprisingly low even among financially literate Indians.

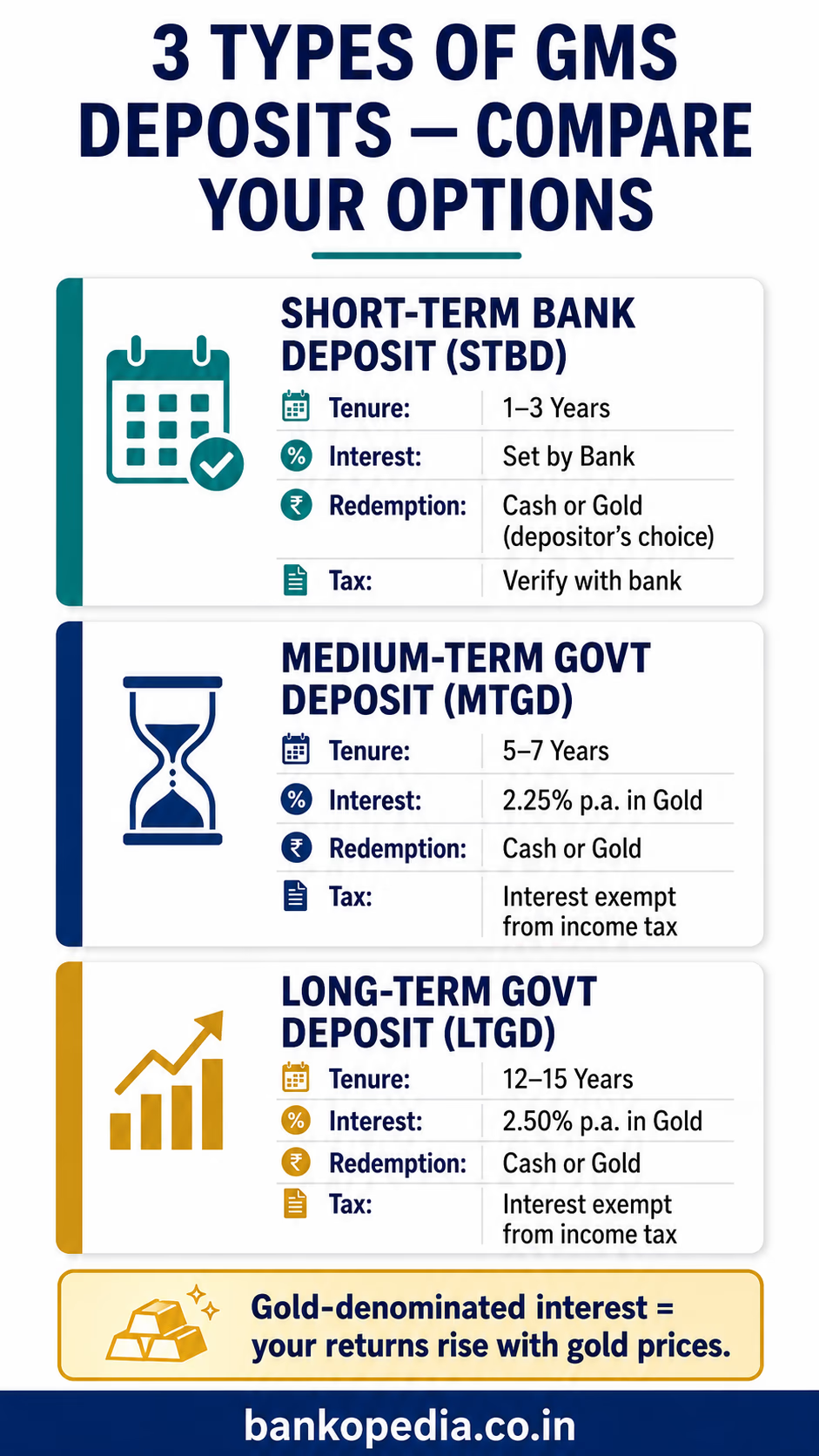

Three Types of Deposits

GMS offers three distinct deposit categories, each with its own interest rate structure and redemption terms:

Short-Term Bank Deposit (STBD): Tenure of 1 to 3 years. Interest rates are decided by individual banks (similar to how banks set fixed deposit rates). Redemption is in cash or gold at the option of the depositor.

Medium-Term Government Deposit (MTGD): Tenure of 5 to 7 years. Interest rate is fixed by the Government of India; currently set at 2.25% per annum, denominated in gold. Administered by the RBI on behalf of the government.

Long-Term Government Deposit (LTGD): Tenure of 12 to 15 years. Interest rate fixed at 2.50% per annum, denominated in gold. Also administered by the RBI.

For MTGD and LTGD, the interest earned is gold-denominated — meaning if you deposit 100 grams, you earn 2.25 or 2.50 grams annually, and this amount appreciates in value as gold prices rise. This is a compounding benefit that many depositors overlook.

Premature Withdrawal

For Short-Term deposits, banks may permit premature withdrawal subject to a penalty, as they do for regular fixed deposits. For Medium and Long-Term deposits, premature withdrawal is permitted after a lock-in period (typically 3 years for MTGD and 5 years for LTGD), subject to a lower interest rate as a penalty.

Tax Benefits: A Significant Advantage

The tax treatment of GMS deposits is genuinely compelling and represents one of the scheme's strongest selling points:

No Capital Gains Tax: Any capital gain arising on redemption of gold deposited under GMS is exempt from capital gains tax, regardless of the holding period. This is a significant benefit given that gold prices have roughly doubled over the past five years.

No Wealth Tax: Gold held under GMS is exempt from wealth tax (though wealth tax has been abolished in India since 2015, this provision remains relevant for legacy understanding).

Interest Income: Interest earned on MTGD and LTGD is exempt from income tax. Interest on STBD may be taxable, depending on the bank's treatment — depositors should verify this with their bank and a tax advisor.

These exemptions make GMS substantially more tax-efficient than, say, selling jewellery (which attracts capital gains tax) or investing in physical gold ETFs (where interest income is taxable).

Why GMS Has Mobilised Only 39 Tonnes in a Decade and What Needs to Change

The headline figure — 39 tonnes mobilised over approximately ten years against an estimated private holding of 25,000 tonnes — is damning by any measure. It represents less than 0.2% of the available gold pool. Understanding why the scheme has underperformed is essential to charting a course for reform.

1. Emotional and Cultural Attachment to Physical Gold

Gold in India is not merely an asset class — it is inheritance, identity, and insurance wrapped into one. Jewellery gifted at weddings carries sentimental value that no interest rate can compensate for. The requirement that deposited jewellery be melted and refined is a deal-breaker for a large portion of potential depositors. Unlike a bank fixed deposit where the depositor always gets back their exact principal, GMS converts grandmother's necklace into anonymous gold credits — an exchange that many Indian families simply will not make.

2. Inadequate Infrastructure of CPTCs

The number of BIS-certified Collection and Purity Testing Centres remains woefully inadequate relative to India's geographic and demographic spread. In many tier-2 and tier-3 cities, and almost universally in rural India, there are no accessible CPTCs. The physical inconvenience of transporting gold to a testing centre — combined with concerns about the safety of gold in transit — deters many potential depositors.

3. Low Awareness and Poor Last-Mile Banking Outreach

Despite a decade of existence, GMS remains poorly understood even among educated urban investors. A scheme that requires depositors to navigate CPTCs, fire assay tests, Gold Savings Accounts, and differentiated tenure structures is inherently complex. Banks have not invested heavily in training branch staff to explain and promote GMS, and marketing efforts have been minimal compared to campaigns for insurance products or mutual funds — where distribution incentives are considerably higher.

4. Trust Deficit and Grievance Redressal

Several depositors have reported challenges related to purity disputes — situations where the gold tested at a CPTC was graded lower than expected, resulting in a smaller deposit than anticipated. Without a robust, accessible grievance redressal mechanism, such experiences spread through word of mouth and discourage potential depositors. The RBI has issued guidelines on depositor protection, but implementation at the ground level remains inconsistent.

5. Competition from More Accessible Alternatives

The Sovereign Gold Bond Scheme, also launched in 2015, has arguably cannibalised some of GMS's potential depositor base. SGBs offer gold-linked returns, capital gains exemption on maturity, and 2.5% annual interest — all without requiring the depositor to surrender physical gold. For someone looking to invest in gold financially, SGBs are simply more convenient. GMS, by contrast, requires the depositor to already own physical gold and be willing to surrender its physical form — a much higher behavioural barrier.

What Needs to Change: A Reform Agenda

For GMS to fulfil its potential, a multi-pronged reform agenda is necessary:

Expand CPTC Infrastructure: The government should fast-track BIS certification of more testing centres, including mobile CPTC units that can visit clusters of potential depositors, particularly temple trusts and rural households.

Allow Jewellery to be Returned in Original Form for STBD: For short-term deposits, allowing depositors to get back their original jewellery (rather than refined gold) would remove the single biggest psychological barrier — though this would require significant changes to the scheme's architecture.

Introduce Distributor Incentives: Banks and financial intermediaries need a compelling reason to promote GMS. A structured commission or incentive framework, similar to what exists for mutual fund distribution, could dramatically improve last-mile outreach.

Digital Onboarding and Doorstep Gold Collection: Integrating GMS with the India Stack — Aadhaar-based KYC, UPI-linked Gold Savings Accounts — and enabling doorstep collection services through bank correspondents or fintech partners could dramatically lower the friction of participation.

Bring Temple Trusts on Board: Religious and charitable trusts are estimated to hold thousands of tonnes of gold. A targeted outreach programme, perhaps led by NABARD in partnership with state governments, could mobilise significant quantities from institutionalised holders who face fewer emotional barriers to melting jewellery.

Mandatory Reporting and Transparency: Publishing quarterly data on GMS deposits, CPTC performance, and bank-wise mobilisation figures would create healthy competition among banks and allow policymakers to identify bottlenecks more quickly.

Conclusion: GMS Remains a Work in Progress — But Its Logic Is Sound

The Gold Monetisation Scheme India remains one of the more intellectually sound financial policy innovations of the past decade. Its underlying logic — that mobilising idle gold reduces import dependence, strengthens the rupee, and creates productive value from dormant wealth — is unimpeachable. The tax exemptions, gold-denominated interest, and flexible tenure options make it genuinely attractive on paper.

Yet 39 tonnes in ten years is a result that demands humility and honest reckoning. The scheme's underperformance is not primarily a failure of financial design — it is a failure of implementation infrastructure, last-mile delivery, and cultural sensitivity. Any meaningful reform of GMS must begin with the recognition that Indian gold is not simply a commodity to be monetised; it is a store of memory, trust, and security that policy must engage with respect rather than impatience.

For banking professionals, GMS represents both a client advisory opportunity and an institutional challenge. Explaining its mechanics clearly, identifying clients with idle gold holdings — particularly HUFs, trusts, and senior clients with inherited jewellery — and guiding them through the deposit process can generate goodwill and deepen banking relationships, even if the direct revenue from GMS itself is modest. As India works toward its Viksit Bharat ambitions for 2047, unlocking the productive potential of its household gold will be an essential, if difficult, part of the journey.