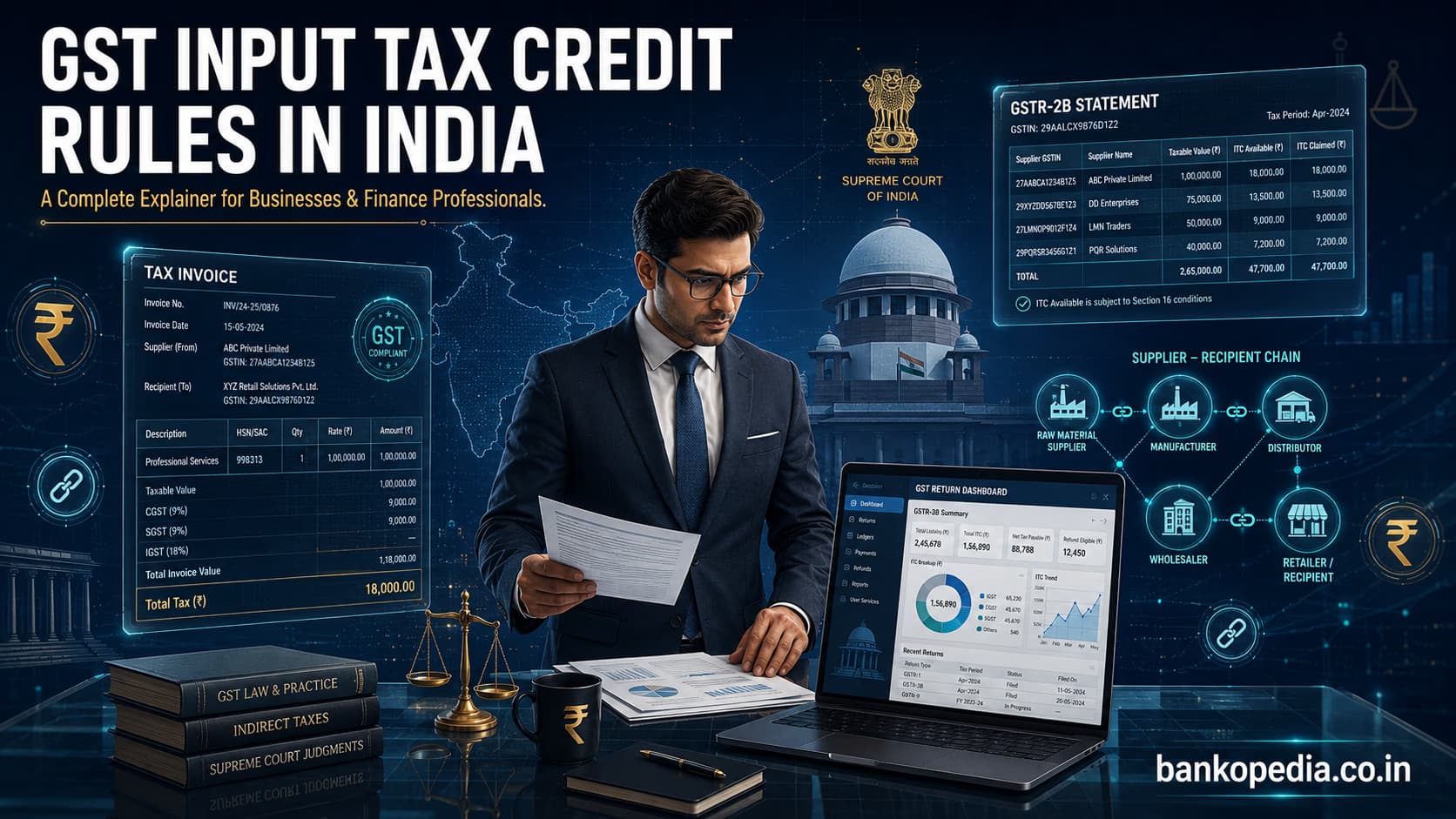

GST Input Tax Credit Rules in India: A Complete Explainer for Businesses and Finance Professionals

For any business registered under India's Goods and Services Tax regime, GST input tax credit rules in India represent one of the most consequential — and contested — areas of compliance. Input Tax Credit, or ITC, is the mechanism that prevents the cascading effect of taxes by allowing businesses to offset the GST paid on purchases against their output tax liability. In theory, it is an elegant solution to multi-stage taxation. In practice, it has generated significant litigation, regulatory scrutiny, and compliance anxiety, particularly because a recipient's right to claim ITC is directly tied to the behaviour of their supplier. As courts across India continue to shape the legal landscape — most recently, the Gujarat High Court's landmark ruling upholding the provision that links ITC eligibility for the recipient to actual tax payment by the supplier — businesses need a thorough, up-to-date understanding of the rules that govern this critical tax benefit.

What Is Input Tax Credit and Who Is Eligible Under GST in India?

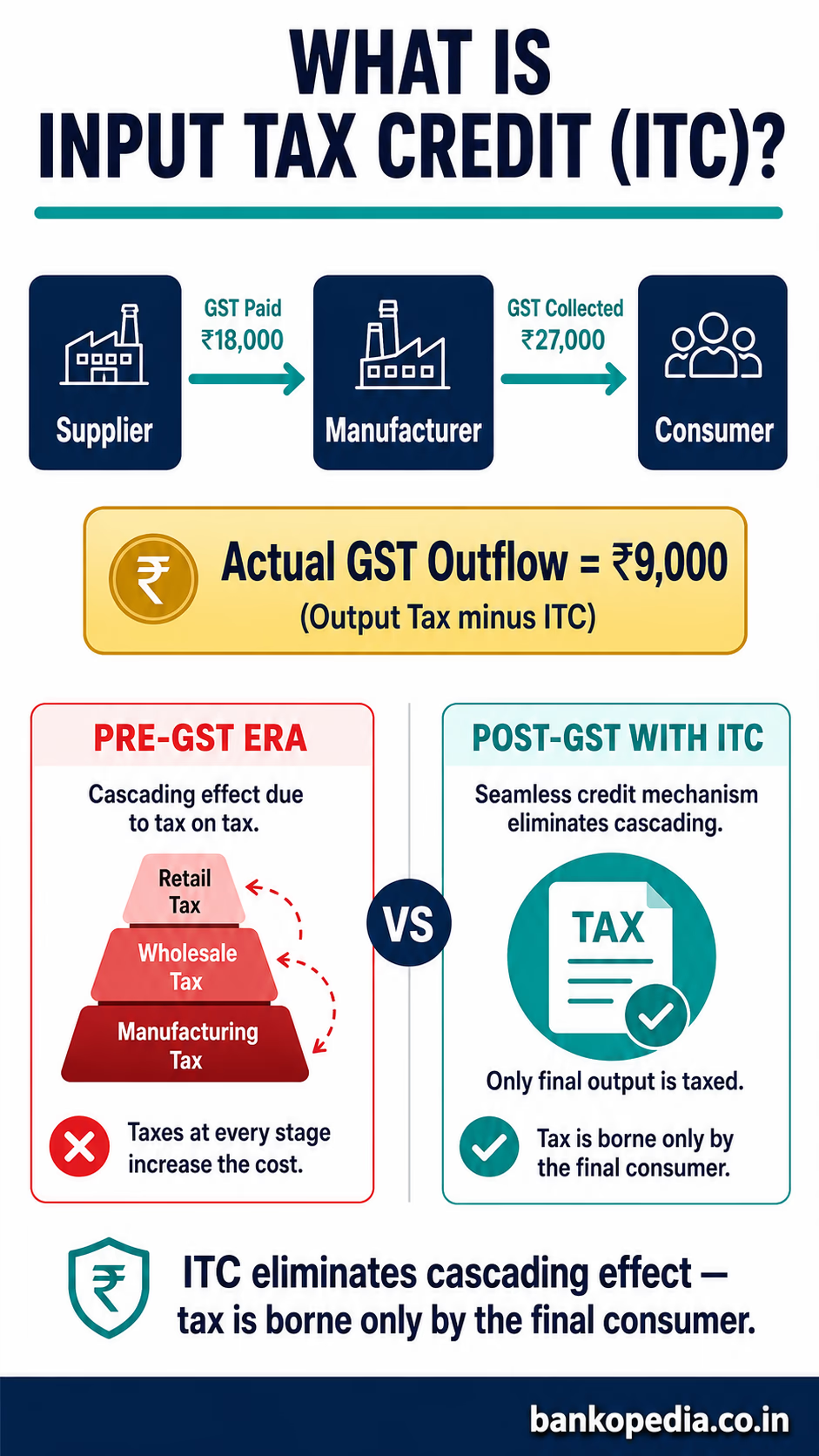

Input Tax Credit is the credit a registered taxpayer can claim for the GST paid on inputs, input services, and capital goods used in the course of their business. It is the backbone of the GST system's design, ensuring that tax is ultimately borne only by the final consumer and not accumulated at every stage of the supply chain.

The Basic Mechanics of ITC

When a manufacturer purchases raw materials worth ₹1,00,000 and pays 18% GST (₹18,000), and subsequently sells finished goods on which 18% GST amounts to ₹27,000, the manufacturer's actual GST outflow is only ₹9,000 — the difference between output tax and ITC claimed. This mechanism keeps working capital intact and prevents tax-on-tax accumulation that plagued the pre-GST era of VAT, Central Excise, and Service Tax.

Who Is Eligible to Claim ITC?

Under Section 16 of the Central Goods and Services Tax (CGST) Act, 2017, a registered person is eligible to claim ITC subject to the following fundamental conditions:

Possession of a valid tax invoice or debit note issued by a registered supplier

Receipt of goods or services — the taxpayer must have actually received the supply

Tax has been paid to the government by the supplier, either in cash or through ITC

Filing of GST returns — the recipient must have filed their own returns under Section 39

Payment to the supplier within 180 days of the invoice date; failure to do so results in reversal of ITC claimed

Certain categories of taxpayers and supplies are excluded from ITC benefits. Composition scheme dealers under Section 10 of the CGST Act cannot claim ITC. Similarly, ITC is blocked under Section 17(5) on specific inward supplies including motor vehicles used for personal purposes, food and beverages, outdoor catering, club memberships, and construction of immovable property (except plant and machinery). It is worth noting the ongoing evolution in this space: the Insurance Regulatory and Development Authority of India (IRDAI) has been pushing for greater clarity on ITC eligibility for insurance companies on third-party motor premiums, an area of growing commercial significance given the surge in third-party motor cover as a driver of non-life insurance premium growth.

The Role of GSTR-2B in Establishing Eligibility

Since the introduction of GSTR-2B — an auto-populated, static ITC statement — the government has provided recipients with a structured view of ITC available based on their suppliers' filed returns. GSTR-2B pulls data from suppliers' GSTR-1 filings and import data, giving recipients a monthly snapshot of claimable credit. However, the availability of ITC in GSTR-2B is a necessary but not sufficient condition; it does not guarantee the credit is legally secure if the underlying supplier has not actually remitted the tax.

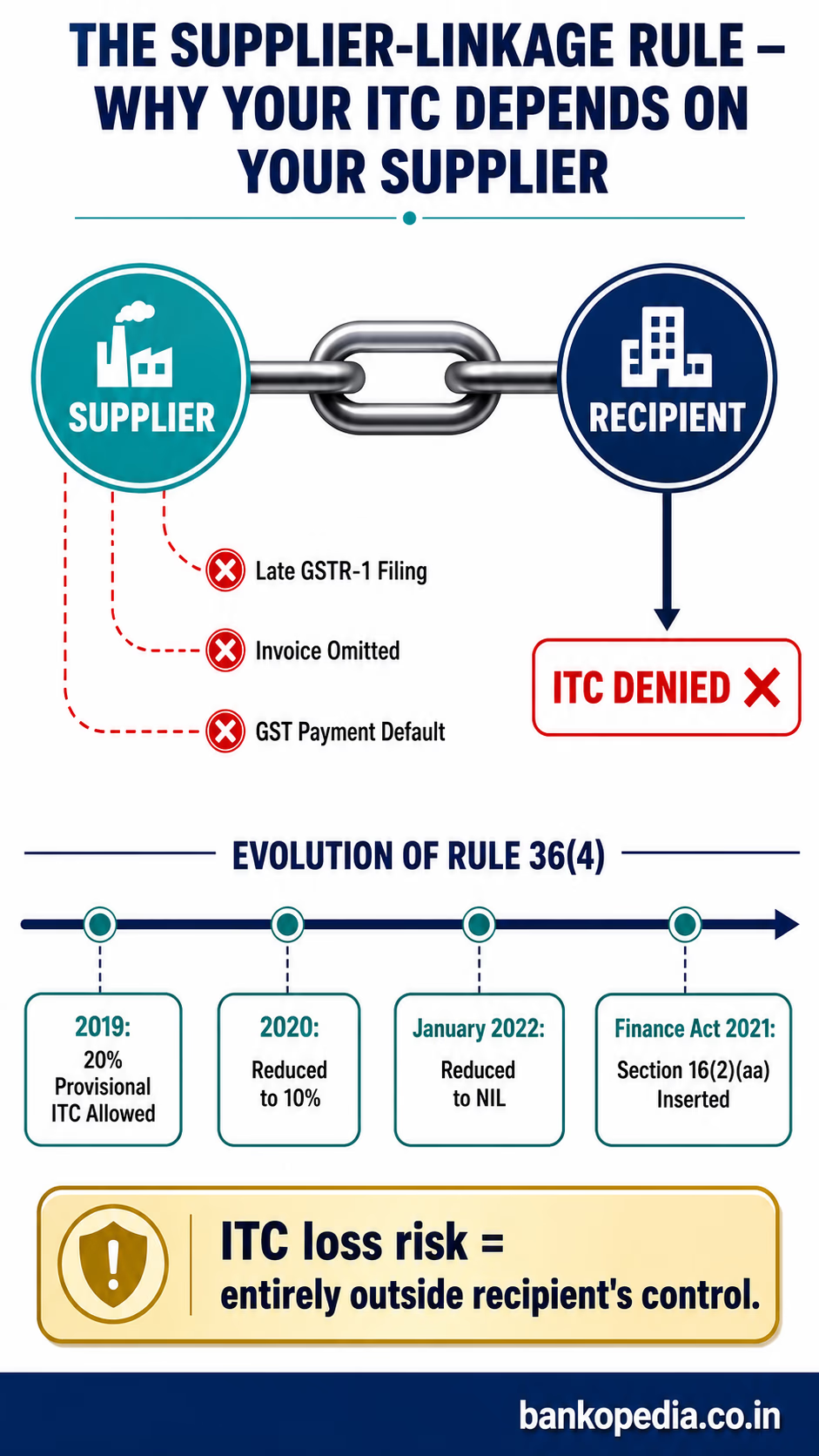

The Supplier-Recipient Linkage Rule: Why Your ITC Depends on Supplier Compliance

Perhaps no aspect of GST input tax credit rules in India has generated more controversy than the conditional linking of a recipient's ITC claim to the supplier's tax compliance. This is not merely a procedural technicality — it is a structural feature of the law that places recipients in a position of vulnerability they cannot fully control.

Understanding Rule 36(4) and Section 16(2)(aa)

The GST Council and the government progressively tightened the ITC matching framework. Rule 36(4), introduced in 2019 and subsequently amended, originally allowed provisional ITC for invoices not reflected in GSTR-2A up to a certain percentage limit (starting at 20%, later reduced to 10%, and eventually to nil in January 2022). The insertion of Section 16(2)(aa) via the Finance Act, 2021 formalised the requirement: ITC is available to a recipient only in respect of invoices and debit notes that have been furnished by the supplier in their GSTR-1 or via the Invoice Furnishing Facility (IFF), and are reflected in the recipient's GSTR-2B.

This means if a supplier files their GSTR-1 late, omits an invoice, or defaults on GST payment entirely, the recipient loses ITC — even if they have a genuine invoice, have received the goods or services, and have made full payment including GST to the supplier. The tax liability simply does not disappear; it shifts to the recipient.

The Implications for Business Operations

This supplier-recipient linkage creates a peculiar compliance burden. A large manufacturer sourcing from hundreds of vendors, or a bank outsourcing multiple services to various agencies, must now effectively monitor the GST filing behaviour of each supplier. For banking institutions — which deal with a vast ecosystem of IT vendors, facility management providers, and professional service firms — this translates into a significant operational risk. Indeed, as public sector banks scale up IT spending in response to evolving cyber threats, ensuring that every technology vendor maintains impeccable GST compliance becomes as much a procurement concern as it is a financial one.

The linkage also creates asymmetric risk: the recipient has paid the tax amount to the supplier (embedded in the invoice price) but cannot recover it through ITC if the supplier vanishes or defaults. In economic terms, it is the recipient who bears the cost of the supplier's non-compliance.

Circular No. 183/15/2022-GST and Departmental Clarifications

The CBIC has issued multiple circulars attempting to clarify the process for matching, reversals, and re-availment of ITC. The framework envisions that if a supplier subsequently files their return and pays the tax, the recipient can re-avail the reversed ITC. However, the time constraints, interest implications, and audit exposure in the interim period make this cold comfort for most businesses.

Key High Court and Supreme Court Rulings Shaping ITC Eligibility

The judiciary has been actively called upon to interpret and, in some cases, temper the rigours of the ITC matching framework. The resulting case law forms an essential reference for tax practitioners and finance professionals.

Gujarat High Court Upholds Supplier-Linkage Provision

In one of the most closely watched recent developments, the Gujarat High Court has upheld the constitutional validity of the provision linking ITC for the recipient to actual tax payment by the supplier. The court found that this condition does not violate fundamental rights and is a reasonable restriction in the context of preventing revenue leakage and tax fraud. This ruling effectively closes one avenue of challenge that many taxpayers had hoped would succeed — the argument that penalising an innocent recipient for a supplier's default is arbitrary and unconstitutional.

The judgment has significant practical implications. It signals that businesses cannot rely on constitutional challenge as a safety net and must instead invest in robust supplier compliance monitoring as a core business function.

Writ Petitions and the "No Fault of Recipient" Argument

Several High Courts, including Delhi and Madras, have grappled with petitions from recipients who argue they should not be denied ITC for circumstances entirely beyond their control. In a number of cases, courts have directed tax authorities to not mechanically deny ITC where the recipient has demonstrated genuine transactions, maintained proper documentation, and made payments through banking channels — the last being particularly important because it establishes a verifiable audit trail.

The Madras High Court, in particular, has on occasion directed the government to re-examine ITC denial orders where recipients produced evidence of bank transfers, lorry receipts, e-way bills, and other corroborating documentation. However, these remain discretionary and fact-specific reliefs rather than settled law protecting all bonafide recipients.

The Apex Court's Position on Transitional Credits

The Supreme Court, in the Filco Trade Centre Pvt. Ltd. case (2022), ruled in favour of taxpayers' rights to claim transitional credits (TRAN-1 and TRAN-2) from the pre-GST era, directing the GSTN to open the portal for filing or revision. This ruling underscored the court's sensitivity to genuine hardship caused by technical and procedural barriers to credit availment. However, the court has also, in broader terms, affirmed that the GST regime's anti-evasion provisions — including conditions on ITC — are within the legislature's competence.

Emerging Jurisprudence on Fake Invoicing

The GST authorities have been particularly aggressive in pursuing ITC claims linked to fake invoicing networks — entities that issue invoices without actual supply, enabling fraudulent ITC claims. Courts have generally supported the department in denying ITC in such cases and have held that the burden of proving the genuineness of supply rests on the claimant. This has created a difficult situation for recipients who may have unknowingly transacted with fraudulent suppliers, reinforcing the importance of due diligence at the onboarding stage.

Best Practices for Businesses to Protect and Reconcile ITC Claims

Given the legal and regulatory environment, businesses — from large corporates and NBFCs to smaller enterprises — must treat ITC management as a continuous, structured compliance function rather than a periodic accounting exercise.

1. Implement a Vendor Compliance Monitoring System

The most effective preventive measure is real-time monitoring of key suppliers' GST filing behaviour. Businesses should:

Use the GSTN's taxpayer search facility to verify GST registration status of all vendors before onboarding

Incorporate GST compliance clauses into vendor contracts, including indemnification provisions for ITC loss caused by supplier default

Automate monthly checks against GSTR-2B to identify mismatches early — ideally within the same return period

Prioritise follow-up with high-value suppliers where ITC exposure is material

2. Conduct Monthly GSTR-2B Reconciliation Without Fail

Reconciling purchase registers with GSTR-2B every month is no longer optional — it is a legal and commercial necessity. Finance teams should map:

Invoices present in the purchase register but absent from GSTR-2B (requiring supplier follow-up)

Invoices in GSTR-2B not yet recorded in accounts (potential duplicate or timing differences)

Discrepancies in invoice values or GSTIN details that could trigger notices

Modern ERP systems and GST-specific reconciliation tools can automate much of this, reducing manual error and ensuring that the 180-day payment rule is also tracked systemically.

3. Maintain Comprehensive Documentation for Every Claim

In the event of a departmental audit or notice, the strength of an ITC claim rests heavily on documentation. Businesses should maintain, for every significant inward supply:

Original tax invoice and, where applicable, e-way bill

Proof of receipt: goods receipt notes, delivery challans, or service completion certificates

Payment proof: bank transfer records linking payment to the specific invoice

Supplier's GSTIN verification screenshot at the time of transaction

This documentation package not only strengthens the defence in proceedings but also aligns with judicial guidance from multiple High Courts that have protected bonafide recipients who could demonstrate genuine transactions through banking and logistics evidence.

4. Understand and Apply Blocked Credits Rules Carefully

The Section 17(5) blocked credits list requires careful application, particularly for financial institutions and service firms. Banks and NBFCs, for instance, must carefully distinguish between ITC available on inputs used for taxable services versus exempt services (such as interest income), applying the common credit apportionment formula under Rule 42 and Rule 43 of the CGST Rules. Errors here are a frequent trigger for show-cause notices and demand proceedings.

5. Engage Tax Counsel for Systemic Risk Assessment

Given the evolving jurisprudence — particularly in light of the Gujarat High Court's recent ruling and ongoing writ petitions in various High Courts — businesses with significant ITC exposure should periodically engage qualified GST counsel to assess:

Litigation risk associated with pending ITC claims in disputed periods

The adequacy of contractual protections with major vendors

Opportunities to seek advance rulings from the Authority for Advance Rulings (AAR) for novel or uncertain transactions

Conclusion: ITC Compliance Is a Strategic, Not Just Operational, Priority

The architecture of GST input tax credit rules in India reflects a deliberate policy choice: making ITC a conditional, earned benefit rather than an automatic right. This design serves the important goal of curbing revenue leakage and invoice fraud in a country where the informal economy and compliance gaps remain significant challenges. However, it imposes real costs on honest businesses caught in the compliance failures of their supply chains.

The Gujarat High Court's endorsement of the supplier-linkage condition, combined with the CBIC's continued enforcement focus on ITC mismatch, means the pressure on businesses to manage their ITC ecosystem proactively will only intensify. For Indian banking institutions, financial services firms, and large corporates managing complex vendor networks, ITC is no longer merely a tax line item — it is a risk exposure that demands boardroom-level attention, investment in compliance technology, and ongoing legal monitoring.

The businesses that thrive in this environment will be those that treat supplier compliance as an extension of their own compliance obligations, build documentation cultures that can withstand departmental scrutiny, and stay abreast of the judicial developments that continue to refine the boundaries of this critical tax benefit.

This article is intended for informational purposes only and does not constitute legal or tax advice. Businesses should consult qualified GST practitioners for guidance specific to their circumstances.