India's Local Currency Trade Settlement: Redefining Global Commerce on India's Terms

In an era of shifting geopolitical alignments and growing calls for a multipolar financial order, the India local currency trade settlement mechanism has emerged as one of the most significant policy shifts in the country's post-independence economic history. At its core, this framework allows Indian importers and exporters to invoice, pay, and receive payments in Indian Rupees (₹) — or in a bilateral partner's local currency — rather than routing every cross-border transaction through the US Dollar. For Indian banking professionals, policy observers, and businesses engaged in international trade, understanding how this system works, which countries have signed on, and what the long-term implications are is no longer optional. It is essential knowledge for navigating an increasingly complex global financial landscape.

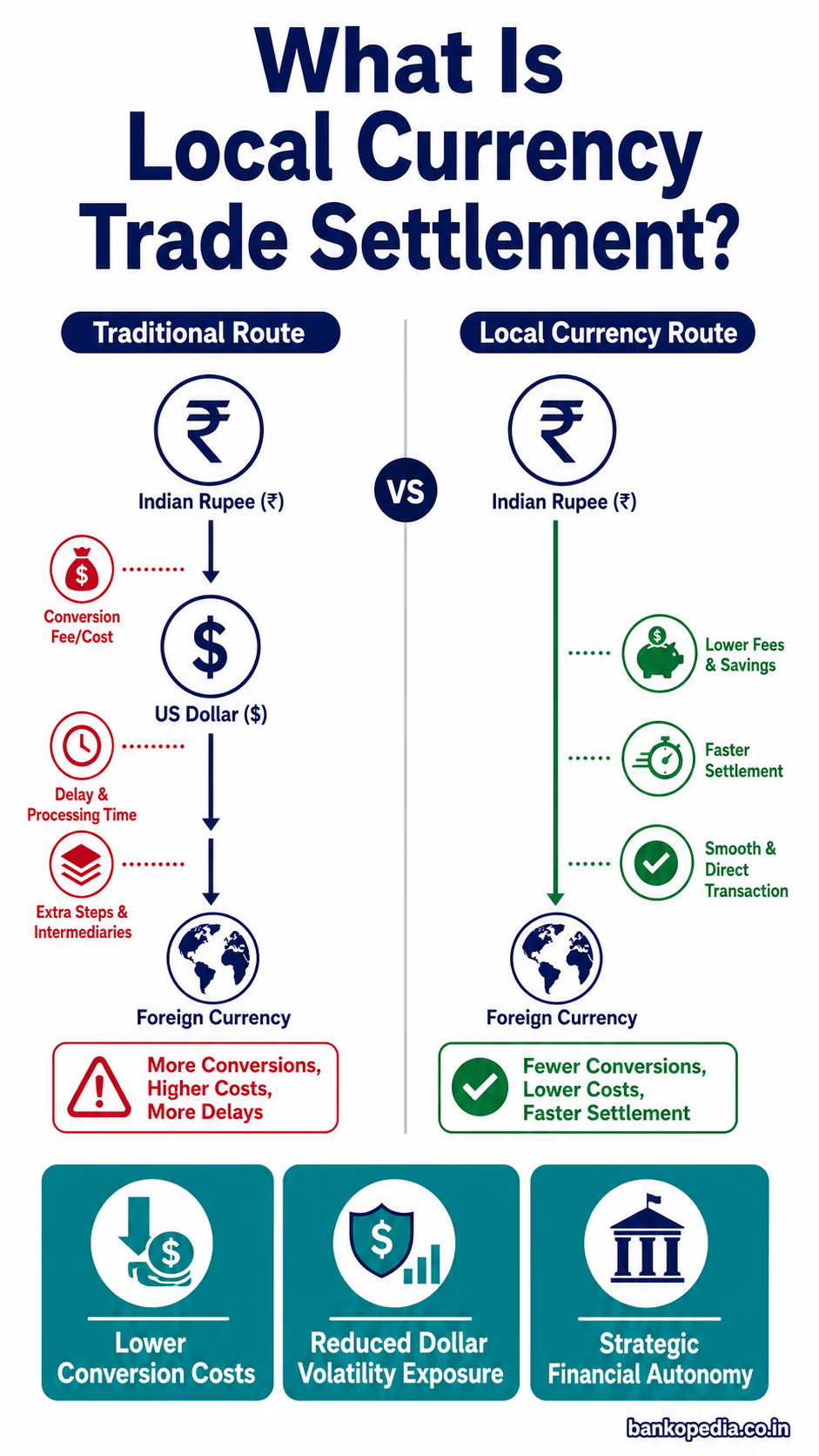

What Is Local Currency Trade Settlement and Why Does It Matter?

Local currency trade settlement refers to the practice of conducting international trade transactions — including invoicing, payment, and final settlement — in the domestic currencies of the trading nations rather than in a globally dominant reserve currency like the US Dollar or the Euro. For most of the post-World War II era, the Dollar has served as the world's primary trade currency, a legacy cemented by the Bretton Woods Agreement of 1944. This means that even when India trades with, say, Malaysia or Russia, both sides have historically had to first convert their currencies into Dollars before transacting.

This dependence on the Dollar creates several structural vulnerabilities for emerging economies like India. Every cross-border transaction incurs currency conversion costs. Indian businesses are exposed to Dollar-Rupee exchange rate volatility that has nothing to do with the bilateral trade relationship. Furthermore, the US Federal Reserve's monetary policy decisions — interest rate hikes, quantitative tightening — have outsized ripple effects on India's foreign exchange reserves and import bills.

The importance of local currency settlement has been underscored by recent global events. The sanctions imposed on Russia following the Ukraine conflict in 2022 demonstrated how rapidly a country could be cut off from Dollar-based financial infrastructure, including the SWIFT messaging network. India, which imports significant volumes of crude oil, fertilisers, and defence equipment, could not afford to have its trade relationships held hostage to third-country geopolitical decisions. This is precisely where the local currency trade settlement mechanism offers strategic insulation.

"The internationalisation of the Rupee is not merely a financial aspiration — it is a strategic imperative for an economy of India's scale and ambition."

Beyond geopolitics, there is a compelling economic rationale. Reducing Dollar dependency lowers transaction costs for Indian businesses, deepens bilateral financial ties, and — over the long term — supports the gradual internationalisation of the Indian Rupee. For a country that is now the world's fifth-largest economy and aspires to be the third-largest by 2030, having its currency play a meaningful role in global trade is a matter of both economic logic and national prestige.

RBI's Framework for Rupee-Based Trade Invoicing

The Reserve Bank of India (RBI) has been the principal architect and regulator of India's local currency trade settlement framework. The RBI laid the formal groundwork in July 2022, when it issued a circular permitting Indian banks to open Special Rupee Vostro Accounts (SRVAs) for correspondent banks of partner countries. This single regulatory step opened the door for bilateral trade to be settled in Indian Rupees without any mandatory Dollar intermediation.

How Special Rupee Vostro Accounts Work

A Vostro account, in traditional banking parlance, is an account that a domestic bank holds on behalf of a foreign bank in the domestic currency. Under the RBI's revised framework, foreign banks — particularly those from countries that have agreed to trade with India in local currencies — can open Rupee-denominated Vostro accounts with Indian correspondent banks. The mechanics work as follows:

An Indian importer pays in Indian Rupees into the SRVA of the foreign exporter's bank.

The foreign exporter receives payment in their local currency, converted from the Rupee balance held in the SRVA.

Similarly, when an Indian exporter ships goods, the foreign importer's bank debits the SRVA and transfers the equivalent local currency to the importer.

The Rupee balances accumulated in SRVAs can also be used for investment in Indian government securities, treasury bills, and other permissible instruments — providing an additional channel for capital deployment.

This architecture is elegant in its simplicity but significant in its implications. It does not require India or its trading partner to hold large Dollar reserves for bilateral trade. The entire transaction corridor is domestic-currency denominated on both ends.

Regulatory Safeguards and RBI Oversight

The RBI has built a layered oversight structure around this framework. Indian banks seeking to open SRVAs for foreign correspondent banks must seek prior approval from the RBI. The central bank evaluates each application on the basis of the bilateral trade relationship, the regulatory standing of the foreign correspondent bank, and the macroeconomic risk profile of the partner country. This ensures that the mechanism is not misused for capital flight, money laundering, or sanctions evasion.

Banks are also required to comply with existing Foreign Exchange Management Act (FEMA) guidelines, Know Your Customer (KYC) norms, and Anti-Money Laundering (AML) standards. The RBI's oversight role here is not merely administrative — it is the critical trust anchor that gives the framework credibility in the eyes of both domestic banks and foreign correspondents. This is consistent with the RBI's broader mandate of ensuring monetary and financial stability while supporting India's external sector.

In keeping with the RBI's recent emphasis on data-driven policy, the central bank has also launched key surveys targeting monetary policy inputs — gathering granular data on trade flows, currency usage patterns, and financial system stress indicators. This research infrastructure will be critical for fine-tuning the local currency settlement framework as it scales.

The Role of Indian Banks

Authorised Dealer (AD) Category-I banks in India — which includes all major public sector banks, private sector banks, and foreign banks operating in India — are the primary conduits for implementing the SRVA framework. Banks such as State Bank of India, Bank of Baroda, and Union Bank of India have been at the forefront of establishing SRVA relationships with foreign correspondent banks. The Indian Banks' Association (IBA) has also played a facilitative role in harmonising operational procedures and documentation standards across member banks.

Countries That Have Agreed to Trade in Rupees with India

Since the RBI's July 2022 circular, India has made rapid, if uneven, progress in establishing local currency trade settlement arrangements across multiple geographies. The scope and depth of these arrangements vary — some are comprehensive bilateral frameworks, others are more limited or still being operationalised.

Russia

The India-Russia local currency trade corridor has been among the most consequential and, simultaneously, most complex. Following Western sanctions on Russia, India dramatically scaled up its imports of discounted Russian crude oil. With Dollar-based payments becoming legally and logistically complicated, both countries moved aggressively toward Rupee-Rouble trade. Russian banks opened SRVAs with Indian correspondent banks, and a significant portion of oil trade began being invoiced in Rupees. However, the arrangement has faced friction: Russia has accumulated large Rupee balances that it cannot easily repatriate or deploy, given the Rupee's limited convertibility on the capital account. This imbalance — where India exports less to Russia than it imports — has created a structural surplus of Rupees in Russian hands that remains a work-in-progress to resolve.

UAE

The UAE represents perhaps the most commercially mature local currency settlement corridor for India. Bilateral trade between India and the UAE exceeds $85 billion annually, and the two countries signed a Comprehensive Economic Partnership Agreement (CEPA) in 2022. The India-UAE local currency framework allows for settlement in both Rupees and UAE Dirhams. The UAE's status as a major hub for the Indian diaspora, gold imports, and re-export trade makes this corridor particularly significant. Several Indian banks have operationalised SRVA arrangements with UAE-based correspondents, and cross-border transactions in Rupees and Dirhams are increasingly routine.

Sri Lanka and Bangladesh

India's immediate neighbours have also been early adopters of Rupee-based trade settlement, albeit for different reasons. Sri Lanka, recovering from a severe foreign exchange crisis, found Rupee-denominated trade with India a practical lifeline when its Dollar reserves were critically depleted. Bangladesh, India's largest trade partner in South Asia, has formalised arrangements for Rupee settlement for a range of goods, leveraging the significant volume of bilateral trade in textiles, agri-products, and industrial goods.

Other Partner Countries

Beyond these primary corridors, India has initiated or is in advanced discussions for local currency arrangements with a broader set of countries. These include:

Malaysia — Trade in Rupees and Malaysian Ringgit, with a particular focus on palm oil imports and pharmaceuticals exports.

Indonesia — Bilateral trade in Rupees and Indonesian Rupiah for commodities and manufactured goods.

Kenya and other African nations — Emerging frameworks being explored under India's expanding Africa engagement strategy.

Saudi Arabia and other Gulf states — Discussions ongoing, particularly relevant given India's massive hydrocarbon import dependence.

Iran — Historical precedent of Rupee-based oil trade under sanctions-related arrangements, though geopolitical sensitivities persist.

It is worth noting that the internationalisation of the Rupee is a stated goal of both the RBI and the Government of India, and the Ministry of Finance and Ministry of External Affairs work in tandem with the central bank to advance these bilateral negotiations.

Benefits, Risks, and Challenges of De-Dollarisation for India

Key Benefits

The advantages of a robust India local currency trade settlement mechanism are multiple and strategically meaningful:

Reduced currency conversion costs: By eliminating the Dollar as an intermediary, Indian importers and exporters save on bid-ask spreads and conversion fees, directly improving the competitiveness of Indian goods and services in international markets.

Lower exposure to Dollar volatility: The Rupee has historically depreciated against the Dollar over time. Settling trade in local currencies reduces the hedging burden on Indian businesses, particularly SMEs and MSMEs that lack sophisticated treasury operations.

Conservation of foreign exchange reserves: India's foreign exchange reserves — which the RBI manages carefully — can be preserved if bilateral trade no longer requires Dollar outflows. This strengthens India's external sector resilience.

Strategic autonomy: Reduced Dollar dependence means India's trade relationships are less susceptible to extraterritorial application of US sanctions or financial restrictions imposed by Western governments on third countries.

Rupee internationalisation: As more countries hold and use Rupees for trade, demand for the Indian currency grows, which over time can reduce the cost of capital for Indian borrowers in international markets.

Significant Risks and Challenges

Despite these benefits, the path to de-dollarisation is neither smooth nor without risk. Indian banking professionals must be clear-eyed about the structural challenges involved:

Rupee convertibility constraints: The Indian Rupee is currently convertible on the current account but not fully on the capital account. This limits a foreign country's ability to freely deploy accumulated Rupee balances, making Rupee settlement less attractive for surplus trading partners. Until capital account convertibility is achieved — a long-discussed but unimplemented reform — the Rupee's utility as a settlement currency will remain constrained.

Trade imbalances: India runs trade deficits with many of its key partners, including China, Russia, and the Gulf states. In such scenarios, the foreign partner accumulates Rupees that they cannot easily reinvest or repatriate, creating a one-sided incentive structure that can stall the framework's momentum.

Liquidity and depth of Rupee markets: For a currency to function effectively as a trade settlement medium, it requires deep, liquid secondary markets. India's bond and money markets, while growing, are not yet at the scale of Dollar-denominated markets. The RBI's ongoing efforts to develop the government securities market — including opening it up to foreign investors through SEBI-regulated channels — are important steps in addressing this deficit.

Geopolitical risks: Some of India's local currency arrangements, particularly with Russia and Iran, carry reputational and legal risks in the context of Western sanctions regimes. Indian banks must navigate these corridors carefully to avoid secondary sanctions exposure.

Technology and infrastructure gaps: Operationalising SRVA arrangements requires banks on both sides to upgrade their core banking systems, compliance infrastructure, and correspondent banking networks. For smaller partner countries, this can be a significant implementation barrier.

The Broader De-Dollarisation Context

India's local currency push is part of a broader global trend. The BRICS grouping — of which India is a founding member — has actively discussed the creation of a common BRICS currency or enhanced local currency trade arrangements among member states. While a formal BRICS currency remains a distant and contested prospect, the directional trend is clear: emerging economies are collectively seeking to reduce systemic dependence on any single currency. India's bilateral approach — building a web of local currency arrangements rather than waiting for a multilateral solution — is pragmatic and consistent with its tradition of strategic autonomy in foreign economic policy.

Conclusion: A Framework Worth Building For the Long Term

The India local currency trade settlement mechanism is not a quick fix or a knee-jerk reaction to geopolitical tensions. It is the foundation of a longer-term structural shift in how India engages with the global economy. The RBI's regulatory architecture — centred on Special Rupee Vostro Accounts, rigorous oversight, and careful bilateral sequencing — provides a credible and scalable framework. The participation of major trading partners from the UAE to Russia to Sri Lanka demonstrates that there is genuine appetite for Rupee-denominated trade, particularly among countries that share India's concerns about Dollar dependency.

For Indian banking professionals, the practical implications are immediate: banks must invest in the systems, skills, and compliance infrastructure needed to manage multi-currency trade corridors efficiently. Corporate treasurers must rethink their hedging strategies as a larger share of trade flows shift away from Dollar denomination. Regulators at the RBI must continue the delicate balancing act of opening up the Rupee to greater international use while maintaining financial stability.

The journey toward Rupee internationalisation will be measured in decades, not months. But the direction is set, the regulatory rails have been laid, and India's economic weight gives this ambition genuine credibility. In a world where the rules of global finance are being rewritten, India has wisely chosen to be an author rather than merely a reader of those rules.