External Commercial Borrowings (ECB) in India Explained: A Complete Guide

For Indian companies looking beyond domestic capital markets to fund large-scale investments, external commercial borrowings India guide searches have surged as finance teams weigh international debt against increasingly competitive domestic bank credit. External commercial borrowings, or ECBs, represent one of the most significant channels through which Indian corporates, infrastructure developers, and financial intermediaries access foreign capital. Governed primarily by the Reserve Bank of India (RBI) under the Foreign Exchange Management Act (FEMA), 1999, the ECB framework has evolved considerably over the past two decades — responding to macroeconomic shifts, currency dynamics, and the strategic financing needs of a rapidly growing economy. This article offers a comprehensive overview of what ECBs are, how they work, who can access them, and when they make strategic sense for Indian borrowers.

What Are External Commercial Borrowings and Why Do Indian Companies Use Them?

External commercial borrowings are loans raised by Indian entities from foreign sources for commercial purposes. They can take the form of bank loans, buyer's credit, supplier's credit, securitised instruments such as floating rate notes and fixed rate bonds, and non-convertible or optionally convertible preference shares. In essence, any debt financing raised from outside India with a defined repayment obligation qualifies as an ECB under the RBI framework.

The motivations for Indian companies to tap ECB markets are several and interconnected:

Lower interest rates abroad: Historically, international markets — particularly USD, EUR, and JPY-denominated instruments — have offered significantly lower nominal interest rates compared to rupee-denominated domestic credit. A large infrastructure company that can borrow at SOFR (Secured Overnight Financing Rate) plus a spread may find the all-in cost considerably lower than an equivalent term loan from an Indian bank.

Longer tenors: Domestic bank credit, especially for project finance, often carries tenor constraints. ECBs, particularly those raised through bond markets, can stretch to 10, 15, or even 20 years — better aligned with the asset life of infrastructure projects.

Diversification of the liability base: Large conglomerates and public sector undertakings (PSUs) use ECBs to diversify funding sources, reducing dependence on any single domestic lender or banking system.

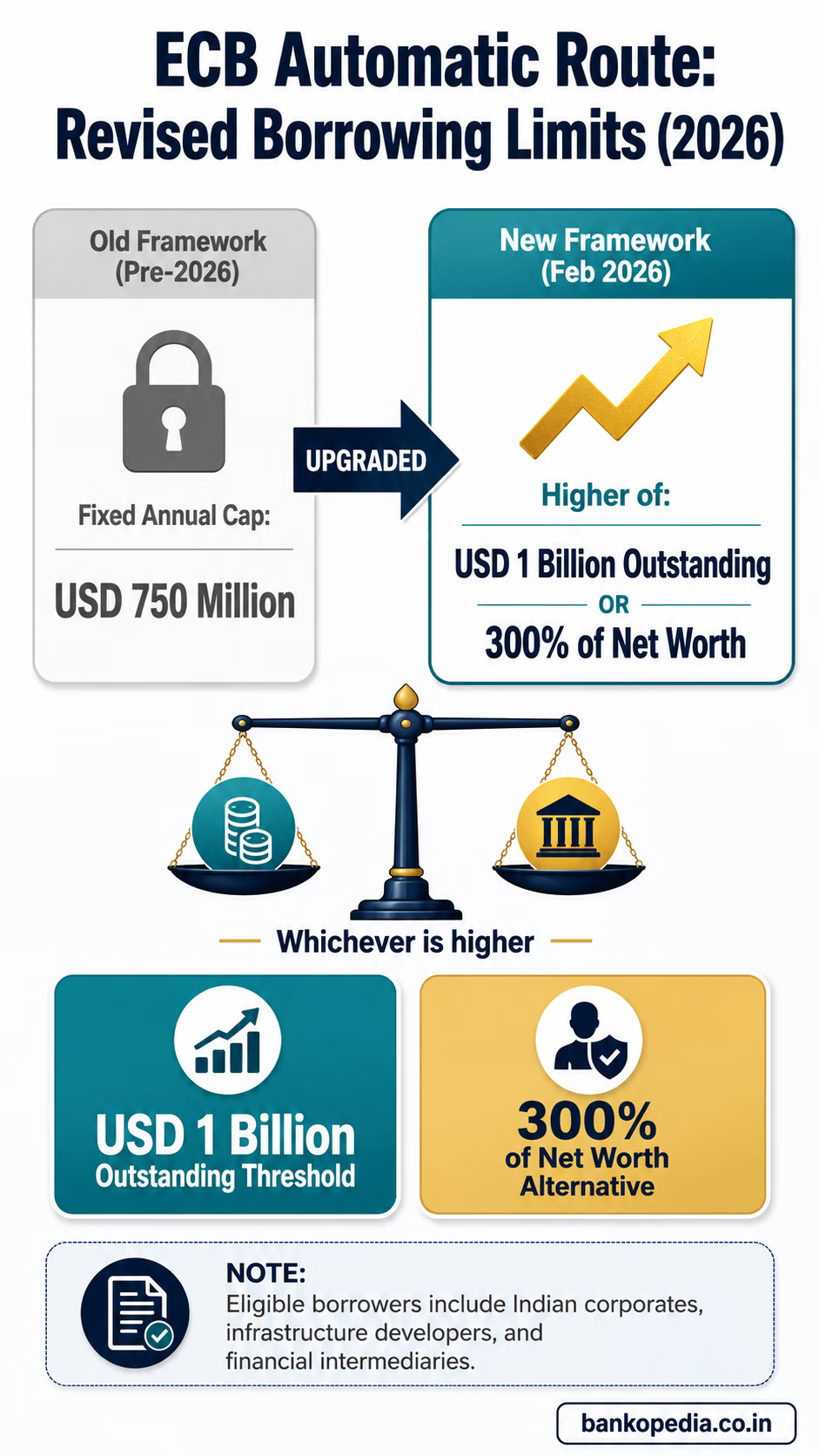

Access to larger ticket sizes: For billion-dollar projects in sectors like power, roads, ports, and telecom, domestic markets may struggle to provide the quantum of debt required at acceptable pricing. Global capital markets offer depth that Indian banks, constrained by single-party and sectoral exposure limits, cannot always match. Under the revised February 2026 framework, borrowers under the Automatic Route can raise the higher of USD 1 billion outstanding or 300% of their net worth — replacing the old fixed annual cap of USD 750 million.

Supporting foreign exchange earnings: Companies with natural currency hedges — exporters, IT services firms, shipping companies — can borrow in foreign currency without incurring significant hedging costs, since their revenue streams in the same currency offset exchange rate risk.

However, it is important to note that ECB volumes are not static. Recent data reveals that India Inc raised 33% less via ECBs in FY26 compared to the previous year, as domestic bank credit turned attractively priced following RBI's rate adjustments. This cyclical dynamic illustrates that ECBs are not universally superior — their appeal rises and falls with relative interest rate differentials, currency outlook, and domestic liquidity conditions.

"The ECB framework is not just a borrowing mechanism — it is a barometer of how Indian companies perceive the relative cost and risk of international versus domestic capital at any given point in the economic cycle."

RBI's Two Routes: Automatic Route vs Approval Route for ECBs

The RBI administers the ECB framework through two distinct channels: the Automatic Route and the Approval Route. Understanding the difference between these routes is essential for any finance professional or treasury team working on cross-border financing.

The Automatic Route

Under the Automatic Route, eligible borrowers can raise ECBs without prior RBI approval, provided they comply with the parameters laid down in the Master Direction on External Commercial Borrowings, Trade Credits, and Structured Obligations. This route is administered through Authorised Dealer (AD) Category I banks, which are responsible for ensuring compliance before remitting funds.

Key parameters under the Automatic Route include:

Minimum Average Maturity Period (MAMP): ECBs must generally have a minimum average maturity of 3 years, with some sector-specific exceptions. Following the February 2026 RBI amendments, manufacturing companies can now raise ECBs with a MAMP of 1 to 3 years subject to an outstanding cap of USD 150 million — a significant expansion from the earlier limit of USD 50 million per financial year — providing greater flexibility for working capital and capacity-building needs.

All-in Cost: Following the February 2026 RBI amendments, the previous fixed basis-point caps over the benchmark rate have been abolished. The all-in cost must now be in line with prevailing market conditions and, for related-party transactions, must adhere to the arm's length principle. This principle-based approach replaces the earlier rigid ceilings and gives lenders and borrowers significantly greater pricing flexibility.

End-use restrictions: Proceeds cannot be used for purposes specifically prohibited by the RBI (discussed in detail below).

Reporting requirements: Borrowers must submit a Loan Registration Number (LRN) application through the AD bank, and regular reporting in Form ECB 2 on actual transactions is mandatory.

The Approval Route

Certain categories of borrowers or end-uses that fall outside the Automatic Route parameters require prior approval from the RBI. Applications under this route are submitted through the AD Category I bank to the RBI's Foreign Exchange Department. The RBI considers these on a case-by-case basis, evaluating macroprudential implications, sectoral needs, and the borrower's track record.

Entities that typically use the Approval Route include:

Companies in sectors not otherwise covered under the Automatic Route

Borrowings for purposes not permitted under the Automatic Route but considered strategically important

Requests involving waivers of standard parameters such as MAMP

Non-profit organisations, registered trusts, and societies engaged in microfinance, under specific conditions

The Approval Route involves greater regulatory scrutiny and processing time, but it provides flexibility for borrowers with genuine needs that do not fit the standardised framework. Finance teams should build adequate lead time — typically 4 to 8 weeks — into project timelines when seeking RBI approval.

The FCY and INR Tracks

An important structural nuance within the ECB framework is the distinction between Foreign Currency ECBs (FCY ECBs) and Indian Rupee-denominated ECBs (INR ECBs), often called Masala Bonds. It is worth noting, however, that technically "Masala Bonds" specifically refer to rupee-denominated bonds issued in offshore capital markets, while INR ECBs are a broader category that also encompasses rupee-denominated bank loans raised from offshore branches of Indian banks or foreign lenders. INR ECBs shift the currency risk to the foreign lender, since repayment is in rupees, making them particularly attractive when the rupee is expected to appreciate or remain stable. However, with the rupee facing depreciation pressure — as income tax authorities have stepped up vigilance on suspicious outflows and wholesale inflation reaching a 42-month high of 8.3% in April 2026 — the appeal of INR ECBs from a foreign investor's perspective may be tempered.

Eligible Borrowers, Lenders, and End-Use Restrictions

The ECB framework carefully defines who can borrow, from whom, and for what purpose. These eligibility criteria are central to understanding the practical scope of the instrument.

Eligible Borrowers

Following the February 2026 amendments, the definition of eligible borrowers has been significantly broadened. Any non-individual resident entity incorporated or established under law is now eligible to raise ECBs. This includes, among others:

Companies registered under the Companies Act, 2013 (excluding financial intermediaries such as banks, NBFCs raising ECBs for on-lending, unless specifically permitted)

Limited Liability Partnerships (LLPs) — now explicitly permitted to raise ECBs, representing a major structural shift for cross-border debt in India

Infrastructure Finance Companies (IFCs) and Infrastructure Debt Funds (IDFs) registered with the RBI

Port Trusts, Units in Special Economic Zones (SEZs), SIDBI, and EXIM Bank

Registered entities engaged in microfinance activities

Societies, trusts, and cooperatives engaged in agriculture, agro-processing, and related activities under specific conditions

Housing Finance Companies registered with the National Housing Bank

Notably, banks are generally not permitted to raise ECBs for lending purposes, though they may access foreign currency resources through other approved mechanisms such as foreign currency borrowings for trade finance.

Eligible Lenders

The pool of recognised ECB lenders is broad but defined. It includes:

Foreign equity holders holding at least 25% of the paid-up equity of the borrowing entity

International banks and capital market players

Multilateral and regional financial institutions such as the World Bank, Asian Development Bank (ADB), and the New Development Bank (NDB)

Export credit agencies and suppliers of equipment

Foreign branches and subsidiaries of Indian banks (subject to regulatory prudential norms)

Foreign pension funds and sovereign wealth funds meeting minimum required regulatory oversight

The explicit listing of eligible lenders serves as a safeguard against round-tripping — where Indian money cycles through offshore structures and re-enters as ECB, creating artificial leverage without genuine foreign capital inflow.

End-Use Restrictions

The RBI is explicit about both permitted and prohibited end-uses. Permitted uses under the Automatic Route include:

Capital expenditure for new projects or expansion

Import of capital goods

Overseas direct investments and acquisitions (subject to other FEMA provisions)

Refinancing of existing ECBs, provided the residual maturity is not reduced

Working capital for aviation and shipping sectors

General corporate purposes (for eligible borrowers meeting specific conditions)

Prohibited end-uses are equally well-defined and include:

Real estate activities (excluding certain affordable housing and SEZ infrastructure)

Investment in capital markets or equity instruments domestically

Lending on-ward to other entities (except for eligible entities like NBFCs permitted for specific sectors)

Repayment of rupee loans to domestic banks, except in cases specifically permitted

Acquisition of land in India

These restrictions reflect the RBI's broader macroprudential objective: ECBs should channel productive foreign capital into capacity creation, not fuel speculative activity or leverage within the domestic financial system.

ECBs vs Domestic Bank Credit: Cost, Risk, and Strategic Considerations

Perhaps the most consequential decision a corporate treasurer faces is whether to access ECBs or rely on domestic bank credit. This is not a binary choice — many large companies use both in combination — but the trade-offs are significant and deserve careful analysis.

Cost Comparison

On face value, international interest rates have historically been lower than Indian domestic rates. The RBI's repo rate has typically ranged between 4% and 7% over the past decade, with corporate loan spreads adding another 150 to 400 basis points depending on credit quality. By contrast, USD-denominated borrowings (before hedging) have often been available at 5% to 7% all-in for investment-grade Indian issuers in recent years.

However, the true cost comparison must account for currency hedging. When a company borrows in USD and earns in rupees, it must either accept foreign exchange risk or purchase a hedge (cross-currency swap or forward cover). The cost of hedging approximately equals the interest rate differential between India and the US — a reflection of the interest rate parity principle. After full hedging, the cost of an ECB often converges with domestic bank credit.

This is precisely why FY26 saw a 33% drop in ECB issuances: as Indian bank credit became more competitively priced following monetary easing, and as the rupee came under depreciation pressure (amplifying hedging costs), the arbitrage that had previously made ECBs attractive narrowed materially.

Risk Dimensions

ECBs carry risks that domestic borrowings do not:

Currency risk: Unhedged or partially hedged ECBs expose borrowers to rupee depreciation. A company that borrows USD 100 million when the exchange rate is ₹82/USD faces a significantly higher repayment burden if the rupee falls to ₹90/USD — an increase of nearly ₹800 million in principal alone.

Refinancing risk: International capital markets can seize up during global risk-off episodes (as seen during the 2008 financial crisis or the 2020 COVID shock), making refinancing expensive or impossible at short notice.

Covenant complexity: Cross-border loan agreements typically carry more complex financial covenants, cross-default clauses, and governing law provisions (often English or New York law) compared to domestic facilities, requiring sophisticated legal and treasury capabilities.

Regulatory compliance burden: Ongoing RBI reporting obligations, LRN management, and compliance with FEMA provisions add an administrative layer that domestic borrowings do not entail.

Strategic Scenarios Where ECBs Make Sense

Despite these complexities, ECBs remain strategically compelling in several scenarios:

Natural currency hedges: IT exporters, pharmaceutical companies, and engineering exporters with large foreign currency receivables can borrow in the same currency as their revenues, eliminating hedging costs entirely.

Very long tenor requirements: For 15-20 year infrastructure projects, ECBs via project bonds or multilateral lending can provide tenors unavailable in the domestic market.

Large quantum financing: When the deal size exceeds ₹5,000 crore, domestic banks may struggle with concentration limits; international syndicated loans or bond markets offer the scale required.

Periods of domestic monetary tightening: When the RBI is in a rate-hiking cycle and domestic credit is expensive, well-hedged ECBs can offer genuine cost savings.

ESG and sustainability-linked financing: Green bonds and sustainability-linked loans from international ESG-focused investors are growing channels for Indian companies with strong environmental credentials, often at preferential pricing.

The Domestic Credit Landscape Today

The current environment presents a nuanced picture. With wholesale inflation hitting a 42-month high of 8.3% in April 2026 and the RBI carefully managing liquidity, domestic bank credit has been both competitively priced and readily available for creditworthy borrowers. The income tax department's heightened scrutiny on outflows — prompted partly by rupee weakness — adds a layer of sensitivity around cross-border financial transactions. For mid-sized companies without sophisticated treasury operations or natural currency hedges, this environment tilts the equation firmly toward domestic credit.

Conclusion: Navigating ECBs With Eyes Open

External commercial borrowings remain a vital pillar of India's corporate financing architecture, particularly for large-scale infrastructure, export-oriented industries, and companies requiring long-tenor or high-value debt. The RBI's framework — with its two-route structure, clearly defined eligibility criteria, principle-based cost requirements, and end-use restrictions — strikes a deliberate balance between enabling productive foreign capital inflows and safeguarding macrofinancial stability.

For finance professionals and treasury teams, the decision to pursue an ECB must go beyond comparing nominal interest rates. It demands a holistic assessment of hedging costs, currency outlook, regulatory compliance capacity, refinancing risk, and the strategic tenor of the borrowing need. In a year when domestic bank credit has asserted its competitiveness and the rupee faces headwinds, the case for ECBs is more selective — but no less relevant for the right borrower with the right profile.

The February 2026 RBI amendments have brought meaningful structural changes: the shift to a principle-based all-in cost standard, expanded borrowing limits tied to net worth, enhanced MAMP flexibility for manufacturers, and the inclusion of LLPs as eligible borrowers. As the RBI continues to refine its framework — responding to evolving global capital market conditions, domestic monetary dynamics, and India's growing integration into international financial systems — staying current with Master Direction updates and RBI circular amendments is non-negotiable for any practitioner in this space. Bankopedia will continue to track these developments and provide timely, authoritative analysis for India's banking and finance community.