Counter-Cyclical Capital Buffer: Understanding How RBI Safeguards India's Banking System

In the landscape of modern banking regulation, few tools are as strategically significant — yet as widely misunderstood — as the counter-cyclical capital buffer. For anyone seeking a thorough understanding of counter cyclical capital buffer Indian banks explained, this article offers a definitive guide. As India's financial system navigates a complex environment — where RBI Governor Sanjay Malhotra is keeping a watchful eye on supply shocks and inflationary pressures, credit card transactions have jumped 2.6 times in four years, and private credit is filling crucial financing gaps — the CCyB stands as a critical macro-prudential instrument designed to protect the banking sector from the very excesses that economic booms tend to create. Understanding this buffer is not merely an academic exercise; it is essential knowledge for bankers, analysts, policy watchers, and anyone who follows India's financial system closely.

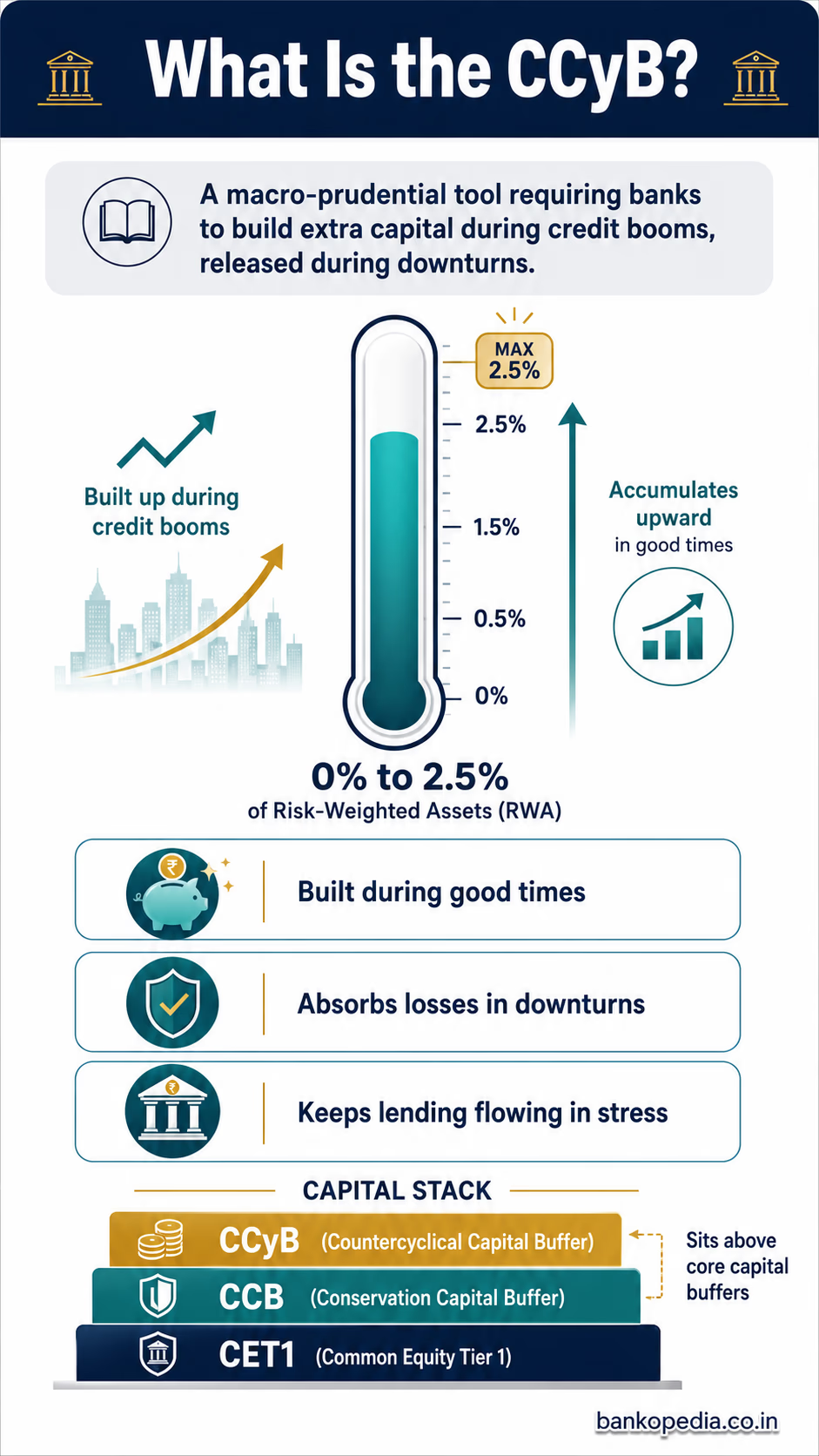

What Is the Counter-Cyclical Capital Buffer (CCyB)?

The Counter-Cyclical Capital Buffer, commonly abbreviated as CCyB, is a macro-prudential regulatory tool that requires banks to build up additional capital reserves during periods of excessive credit growth, which can then be drawn down during periods of economic stress or financial downturns. In simpler terms, it is a financial cushion that regulators compel banks to accumulate in good times, so that those institutions have the resilience to absorb losses and continue lending when the economic cycle turns adverse.

The CCyB is expressed as a percentage of a bank's total risk-weighted assets (RWA). Under the Basel III framework, it can range from 0% to 2.5% of RWA, though national regulators have the discretion to set it higher if systemic risks warrant such a measure. When activated, this buffer sits on top of other mandatory capital requirements, including the Capital Conservation Buffer (CCB) and the minimum Common Equity Tier 1 (CET1) capital requirements.

To appreciate the CCyB in its full context, it helps to understand the concept of procyclicality in banking. Banks, by their very nature, tend to lend aggressively when the economy is booming — credit is cheap, asset values are rising, and default rates are low. Conversely, when the economy contracts, banks tighten credit, raise lending standards, and reduce their balance sheets, which further deepens the downturn. This amplification effect — where banking behaviour makes booms more extreme and busts more severe — is procyclicality. The CCyB is explicitly designed to counteract this dangerous dynamic.

Key Structural Features of CCyB

Capital composition: The CCyB must be met with Common Equity Tier 1 (CET1) capital, the highest quality form of bank capital consisting primarily of retained earnings and paid-up equity.

Jurisdictional reciprocity: Banks operating across borders must maintain CCyB requirements based on their credit exposures in each jurisdiction, not just their home country.

Release mechanism: Unlike other capital buffers, the CCyB can be released relatively quickly by the regulator during stress periods, signalling to banks that they are permitted to use this capital to absorb losses.

Graduated restrictions: When a bank's CCyB falls below the required level, restrictions are placed on dividend distributions, share buybacks, and discretionary bonus payments — creating strong incentives for compliance.

Why Did Basel III Introduce CCyB and How Does RBI Apply It?

The 2008 global financial crisis was, at its core, a story of excessive credit creation followed by a catastrophic collapse. Banks in the United States and Europe had extended enormous amounts of credit during the mid-2000s boom — particularly in real estate — while simultaneously lowering their capital buffers through complex securitisation and off-balance-sheet vehicles. When asset prices collapsed, the banking system had insufficient capital to absorb losses, leading to government bailouts of unprecedented scale and a global recession that affected hundreds of millions of people.

The Basel Committee on Banking Supervision (BCBS), operating under the auspices of the Bank for International Settlements (BIS), responded with the Basel III framework, published in 2010 and progressively implemented over the following decade. The CCyB was one of Basel III's most innovative contributions — a tool that gave national regulators the ability to build system-wide capital during credit booms without requiring permanent increases in capital minimums.

The RBI adopted the Basel III framework and formally introduced the CCyB through its guidelines in 2015, with full implementation phased in by March 2019. The RBI's framework for CCyB is governed by the circular "Guidelines on Counter-Cyclical Capital Buffer" which outlines the triggers, measurement methodology, and operational procedures for activating and deactivating the buffer.

How RBI Measures the Need for CCyB

The RBI uses a multi-indicator approach to assess whether systemic risks have accumulated to a level that justifies activating the CCyB. The primary quantitative indicator is the credit-to-GDP gap — the difference between the actual ratio of total private credit to GDP and its long-term trend. This metric, first proposed by the BCBS, captures the extent to which credit has grown beyond what economic fundamentals would suggest is sustainable.

However, RBI's framework wisely recognises that a single indicator can be misleading, particularly in a large, structurally evolving economy like India's. Therefore, the RBI also monitors a set of supplementary indicators, including:

Growth in credit to the private non-financial sector

Industry-level credit concentration and sectoral stress signals

Asset quality indicators, including gross and net NPA ratios

Housing price indices and real estate credit trends

Equity market valuations and financial conditions indices

Current account deficit and capital flow volatility

The RBI's Financial Stability Report (FSR), published biannually, is the key document where much of this systemic risk assessment is made public. Banking professionals and analysts should treat the FSR as essential reading for tracking where the CCyB dial is likely to move.

"The countercyclical capital buffer aims to ensure that the banking sector in aggregate has the capital available to maintain the flow of credit in the economy without its solvency being threatened." — Basel Committee on Banking Supervision

RBI's Current CCyB Status

It is important to note that as of the most recent RBI guidance available, the CCyB rate for India has been maintained at 0%. The RBI periodically reviews this position and has the authority to activate it when systemic risks are deemed sufficient. The fact that it remains at zero does not indicate complacency; rather, it reflects the RBI's assessment that credit growth, while robust in certain segments, has not yet crossed the threshold that would warrant an activation. Given that credit card transactions have grown 2.6 times in four years according to a recent RBI report — a sign of rising retail credit intensity — this is a space that deserves ongoing monitoring.

When Does RBI Activate or Deactivate the CCyB?

The decision to activate or deactivate the CCyB is one of the most consequential macro-prudential judgements a regulator makes. Get it wrong on the way up, and you fail to build the capital buffer when it is most affordable. Get it wrong on the way down, and you may signal distress prematurely or fail to release capital when banks need it most to keep credit flowing.

Conditions for Activation

RBI activates the CCyB when it determines that systemic risk from excessive credit growth has reached a level where a buffer build-up is justified. The key conditions typically involve:

A significantly positive credit-to-GDP gap: When actual credit-to-GDP substantially exceeds its historical trend, it signals that credit is outpacing economic activity — a classic precursor to financial instability.

Broad-based credit acceleration: When credit growth is not limited to one sector but is expanding rapidly across corporate, retail, and MSME segments simultaneously.

Deteriorating lending standards: Signs that banks are easing collateral requirements, extending longer tenors, or increasing exposure to lower-rated borrowers at scale.

Asset price inflation: Particularly in real estate and equity markets, where credit is fuelling price appreciation that is disconnected from intrinsic value.

When activated, banks are typically given a lead time of up to 12 months to build up the required CCyB. This phased approach prevents a sudden tightening of bank balance sheets that could itself trigger a credit crunch.

Conditions for Deactivation or Release

The CCyB can be released — either partially or fully — when the financial cycle turns. The conditions for release include:

A sharp contraction in credit growth or evidence that the credit-to-GDP gap is closing rapidly

A material deterioration in asset quality across the banking system, signalling that the stress phase has arrived

Heightened systemic risk from external shocks — such as a global financial crisis, a pandemic, or severe geopolitical disruption — that threatens the domestic credit supply

Crucially, the release of the CCyB is designed to be immediate and decisive. Unlike the activation phase, which involves a build-up period, the release can happen with immediate effect. This speed is intentional: during a crisis, the signal that banks are free to use their accumulated capital buffers can restore market confidence and prevent a damaging credit freeze. The COVID-19 pandemic illustrated this globally, as many central banks and regulators released CCyBs to provide banks with maximum flexibility to support borrowers through the shock.

Impact of CCyB on Bank Lending, Credit Growth, and Stability in India

The CCyB has multi-dimensional implications for how Indian banks lend, how credit cycles evolve, and how resilient the financial system becomes over time. These impacts operate through several interconnected channels.

Effect on Bank Lending Behaviour

When the CCyB is activated, banks face a higher capital requirement, which increases the cost of extending new credit. This is not punitive by design — it is corrective. Higher capital costs make banks more selective about the loans they originate, encouraging them to price risk more accurately and avoid the kind of aggressive, margin-compressing lending that characterises the peak of a credit cycle.

For large public sector banks, which dominate India's banking landscape with over 60% of total assets, the CCyB has particular relevance. These institutions, often operating under dual pressures of government ownership and market competition, have historically been susceptible to cycles of excessive lending followed by sharp increases in non-performing assets (NPAs). A well-calibrated CCyB provides an institutional safeguard against this pattern.

Impact on Credit Growth and the Real Economy

Critics of the CCyB sometimes argue that it constrains credit availability at precisely the moment when businesses and households need it most — during a boom, when investment is high and borrowing demand is strong. This concern, while understandable, misunderstands the buffer's purpose. The CCyB does not seek to stop credit growth; it seeks to ensure that credit growth is sustainable and that the banking system retains the capacity to fund that growth through complete economic cycles.

Consider the current Indian context: the Centre is accelerating capital expenditure, with states receiving 50-year interest-free loans under the "Special Assistance to States for Capital Investment" scheme — an outlay of ₹1.3 lakh crore in FY24, subsequently scaled up to ₹1.5 lakh crore for FY25 and FY26 — to boost infrastructure investment. Private credit is stepping in to fill financing gaps in real estate. These are positive developments — but they also represent a significant expansion of credit across multiple sectors simultaneously. If this credit expansion is well-capitalised at the bank level, it supports durable growth. If it is not, it plants the seeds of the next NPA crisis.

The Stability Dividend

Perhaps the most important impact of the CCyB is the stability dividend it generates for the broader financial system. When banks hold higher capital buffers, they are better positioned to absorb losses without requiring government recapitalisation — a recurring feature of India's banking history that has cost taxpayers enormous sums. The recapitalisation of public sector banks following the post-2015 NPA recognition exercise, for instance, required injections running into the hundreds of thousands of crores of rupees.

A robust CCyB regime, consistently applied across the credit cycle, has the potential to significantly reduce the frequency and severity of such episodes. It also strengthens market confidence: when investors and depositors know that India's banks are adequately capitalised on a through-the-cycle basis, the cost of funding for those banks falls and systemic risk premiums decline.

Interaction with Other Macro-Prudential Tools

The CCyB does not operate in isolation. It interacts with a suite of other macro-prudential instruments that the RBI deploys, including sector-specific risk weights, Loan-to-Value (LTV) ratios for home loans, and the Incremental Credit-to-Deposit (ICD) ratio. For example, the RBI has previously increased risk weights on consumer credit and credit card lending — a targeted tool that operates at the sectoral level, complementing the system-wide CCyB. Together, these instruments give the RBI a nuanced toolkit for managing financial stability without resorting to blunt instruments like blanket credit controls.

Conclusion: CCyB as a Pillar of India's Financial Resilience

The counter-cyclical capital buffer represents a sophisticated and essential element of modern bank regulation. For Indian banking professionals, understanding the CCyB — its design logic, its activation triggers, and its real-world impacts — is no longer optional. It is fundamental to interpreting RBI policy signals, assessing bank balance sheet strength, and understanding the macro-prudential architecture that governs India's ₹200-plus lakh crore banking system.

As India's economy continues to grow, as retail credit deepens, as infrastructure financing expands, and as private credit markets evolve, the conditions that might eventually warrant a CCyB activation will periodically come into view. RBI Governor Sanjay Malhotra's emphasis on monitoring supply shocks and inflation reflects the broader vigilance that characterises thoughtful central banking — and the CCyB is a key instrument in that vigilance toolkit.

For banks, the practical implication is clear: capital planning must incorporate CCyB scenarios. Boards and risk committees should model what a 0.5%, 1%, or 2.5% CCyB activation would mean for their capital adequacy ratios, lending capacity, and dividend policies. For analysts and investors, tracking the RBI's CCyB signals — through the Financial Stability Report, the Monetary Policy Committee statements, and prudential circulars — provides valuable intelligence about the regulator's view of systemic risk. And for the broader public, understanding the CCyB is part of understanding why India's banking system, despite its periodic challenges, remains structurally more resilient today than it was two decades ago.

The CCyB is not a constraint on India's growth ambitions. It is the foundation that makes those ambitions sustainable.