The Indian banking sector stands at a critical inflection point in its credit risk management journey. Expected credit loss provisioning in India's banks is transitioning from a reactive, backward-looking accounting exercise to a forward-looking, data-driven discipline that mirrors global best practices. With the Reserve Bank of India (RBI) having released its final guidelines and a phased implementation roadmap, banks across the country — from large public sector lenders to nimble private sector banks — are preparing for one of the most consequential regulatory overhauls in recent memory. A recent assessment by Fitch Ratings affirmed that Indian banks are well-placed to navigate this transition, a view that offers measured optimism even as the sector grapples with the operational and capital implications of the shift.

This article provides a comprehensive overview of the expected credit loss framework, how it differs from the existing incurred loss model, the RBI's specific roadmap for adoption, and what Indian banking professionals can expect in terms of impact on profitability, provisioning buffers, and capital adequacy.

What Is Expected Credit Loss (ECL) Provisioning?

Expected Credit Loss provisioning is a forward-looking methodology for recognising and accounting for potential credit losses on financial assets. At its core, ECL requires banks and financial institutions to estimate the losses they expect to incur on their loan portfolios — not just the losses they have already incurred or that have become objectively evident.

The ECL model was introduced internationally through IFRS 9 (International Financial Reporting Standard 9), issued by the International Accounting Standards Board (IASB) and adopted across European, Asian, and other global markets from 2018 onwards. In India, the applicable accounting standard is Ind AS 109, which is the Indian equivalent of IFRS 9 and governs financial instruments for corporates and non-banking entities. For scheduled commercial banks, the RBI's own prudential guidelines govern provisioning, which has historically been based on the older incurred loss approach.

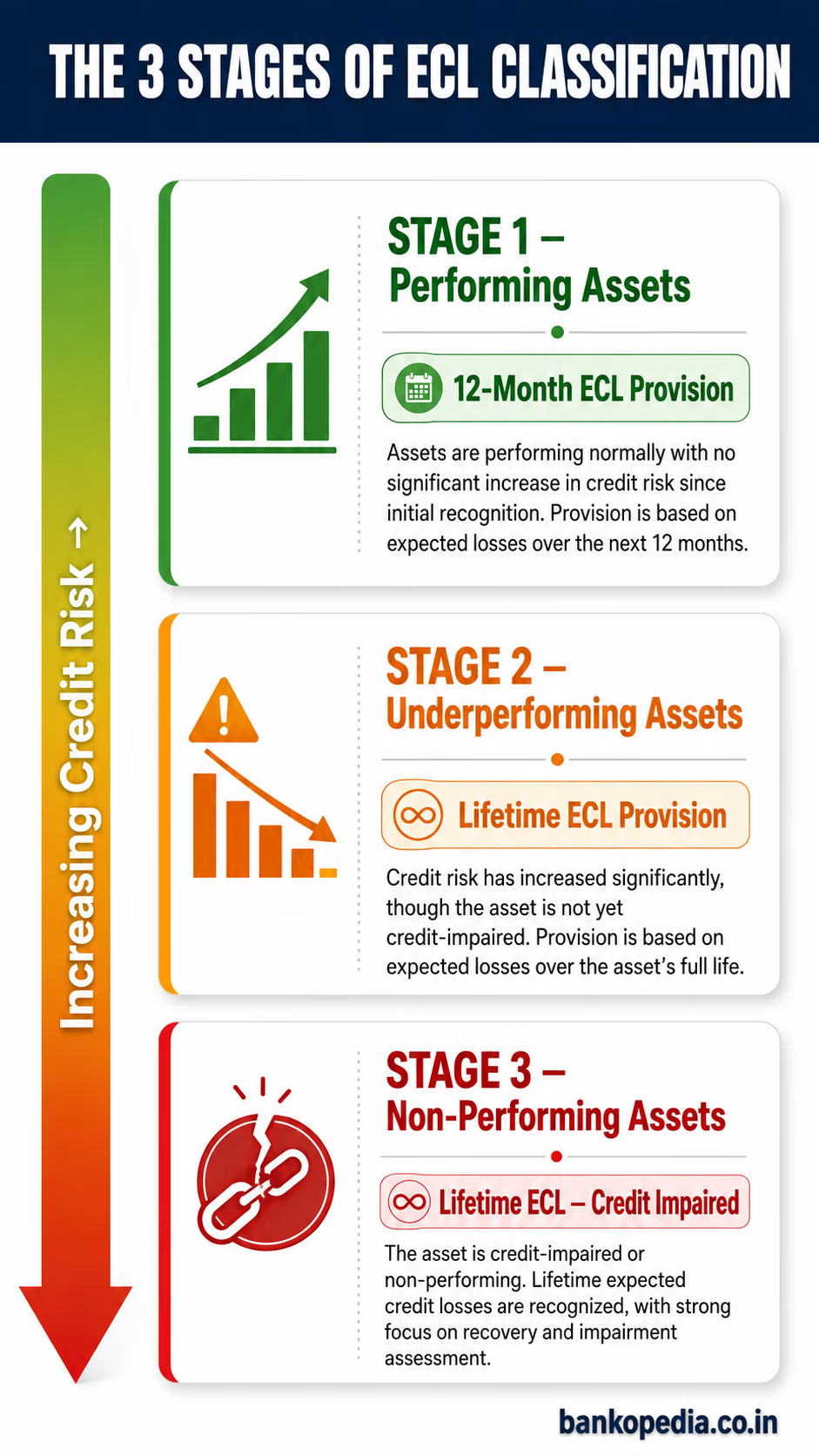

The Three Stages of ECL Classification

A defining feature of the ECL framework is its three-stage classification of financial assets, which determines the quantum of provisioning required:

Stage 1 – Performing Assets: Loans where there has been no significant increase in credit risk since origination. Banks are required to provision for 12-month ECL — the expected losses resulting from default events possible within the next 12 months.

Stage 2 – Underperforming Assets: Loans where credit risk has increased significantly since origination, but no actual default has occurred. Banks must provision for lifetime ECL — expected losses over the entire remaining life of the instrument.

Stage 3 – Non-Performing Assets: Loans in default or credit-impaired. Banks provision for lifetime ECL on a credit-impaired basis, similar in outcome to the current NPA provisioning but with richer data inputs.

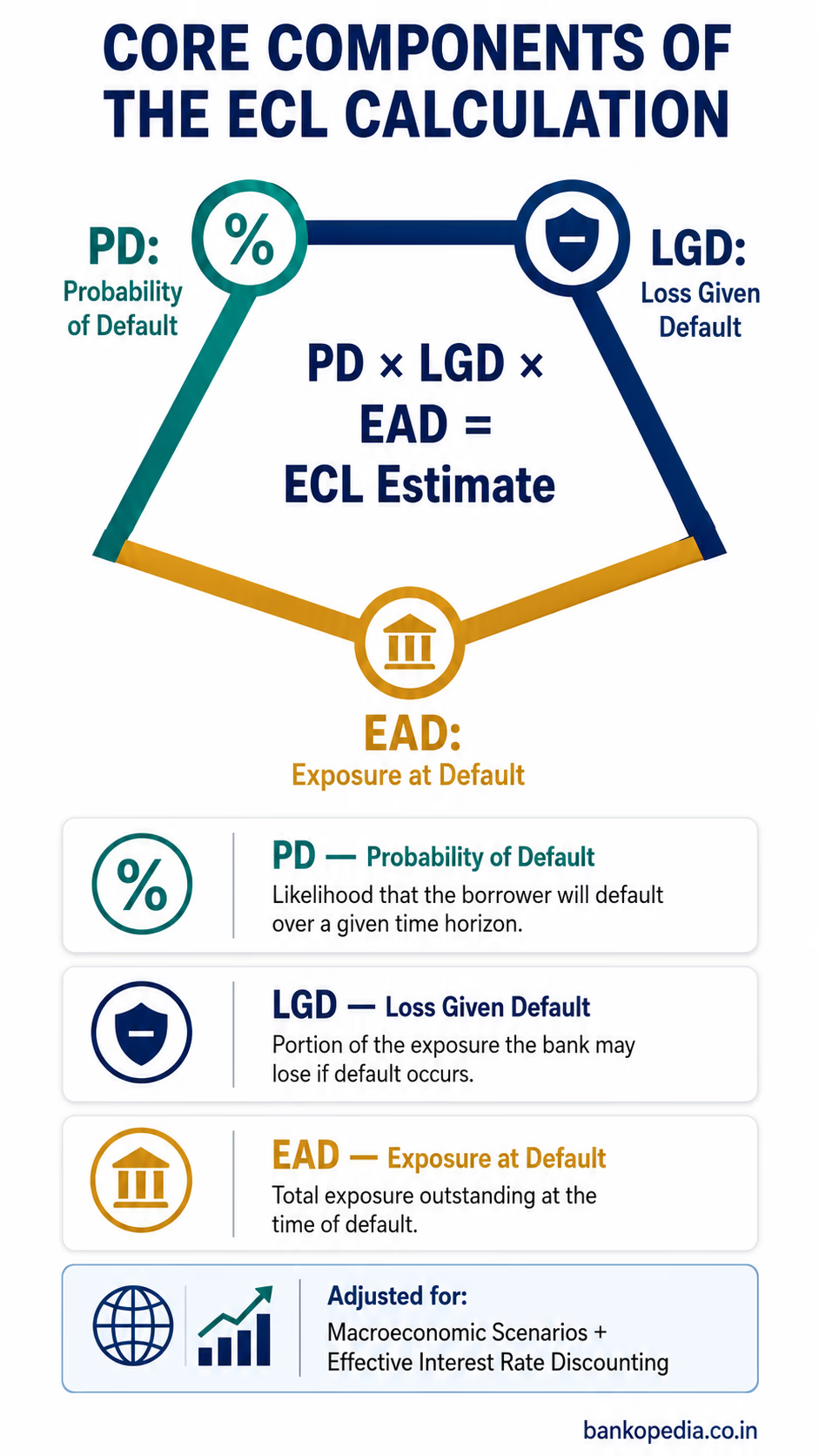

Core Components of the ECL Calculation

The ECL calculation is built on three fundamental parameters, which banks must estimate using historical data, current conditions, and forward-looking macroeconomic information:

Probability of Default (PD): The likelihood that a borrower will default over a specified time horizon.

Loss Given Default (LGD): The proportion of the exposure that the bank expects to lose if a default occurs, after accounting for recoveries and collateral.

Exposure at Default (EAD): The total value the bank is exposed to at the time of default, including drawn balances and undrawn commitments.

The interplay of these three variables, discounted at the loan's effective interest rate and adjusted for forward-looking macroeconomic scenarios, produces the ECL estimate. This is a far more granular and technically demanding exercise than the current provisioning norms, and it requires banks to invest heavily in credit data infrastructure, model development, and validation capabilities.

ECL vs Incurred Loss Model: Key Differences Explained

To appreciate why the ECL transition matters so profoundly for Indian banking, it is essential to understand the fundamental philosophical and operational differences between the existing Incurred Loss Model (ILM) and the incoming ECL framework.

The Incurred Loss Model: A Retrospective Lens

Under the incurred loss model — which has governed Indian bank provisioning through RBI's Income Recognition, Asset Classification and Provisioning (IRACP) norms — a bank recognises a credit loss only when there is objective evidence that a loss event has already occurred. In practice, this means a loan must be overdue for 90 days or more (and classified as a Non-Performing Asset) before the bank is required to make a meaningful provision against it.

The limitations of this approach became painfully apparent during the Indian banking sector's NPA crisis between 2015 and 2020, when a wave of corporate defaults — particularly in sectors like infrastructure, power, steel, and real estate — led to a sharp, sudden surge in provisioning requirements. Banks had been carrying these stressed assets on their books at full value until default crystallised, creating a cliff-edge effect that eroded capital rapidly and forced the government to recapitalise public sector banks to the tune of over ₹3.5 lakh crore over several years.

The incurred loss model created a dangerous illusion of stability. Provisions were made after the storm had already hit. The ECL model is designed to make banks provision while the clouds are still gathering."

— A senior credit risk official at a large public sector bank

Key Differences at a Glance

Dimension | Incurred Loss Model (ILM) | Expected Credit Loss (ECL) |

|---|

Timing of loss recognition | Only after a loss event occurs | From date of origination, based on expected future events |

Scope of provisioning | Primarily NPAs | All financial assets across all three stages |

Use of forward-looking information | Largely backward-looking | Mandates macroeconomic forecasts and future conditions |

Subjectivity and modelling | Mechanical application of prescribed rates | Sophisticated internal models, judgement, and governance |

Cyclicality | Pro-cyclical — provisions surge during downturns | Counter-cyclical — provisions build gradually over time |

Regulatory alignment | RBI prudential norms (IRACP) | Ind AS 109 and global IFRS 9 standards |

The ECL model's superiority lies in its early warning character. By forcing banks to estimate and provision for potential losses on even their best-performing loans, it ensures that provisioning buffers accumulate during good times — precisely when banks have the earnings capacity to absorb them.

RBI's Roadmap for ECL Adoption in Indian Banks

The RBI's journey toward ECL adoption for commercial banks has been deliberate and carefully sequenced. The central bank released a Discussion Paper on Introduction of Expected Credit Loss Framework for Provisioning by Banks in India in January 2023, followed by a Draft Circular in October 2025 and final directions in April 2026, marking the formal beginning of the regulatory transition.

Key Provisions of the RBI's Final ECL Framework

The RBI's finalised framework for expected credit loss provisioning in Indian banks incorporates several distinctive elements tailored to India's banking ecosystem:

Applicability: The framework initially applies to all scheduled commercial banks (excluding regional rural banks, small finance banks, payments banks, and local area banks), covering public sector banks, private sector banks, and foreign banks.

Three-stage classification: Aligned with Ind AS 109 and IFRS 9, with specific RBI guidance on what constitutes a "significant increase in credit risk" in the Indian context.

Macroeconomic scenarios: Banks must incorporate at least three macroeconomic scenarios — base, optimistic, and stressed — weighted by probability, into their ECL estimates.

Regulatory floor: A prudential provisioning floor ensures that ECL-based provisions do not fall below a minimum level, preventing model-driven optimism from eroding buffers excessively.

Impact Assessment (IA) Report: Banks are required to submit a detailed impact assessment, including estimated provisioning requirements, capital impact, and model validation results, before full adoption.

Transitional arrangements: Phased transitional arrangements to spread the capital impact of higher provisioning requirements over time.

Phased Implementation Timeline

With a firm go-live date mandated for April 1, 2027, the RBI's phased approach is expected to unfold broadly as follows:

Phase | Description |

|---|

Preparatory Phase | Banks build internal ECL models, develop data infrastructure, conduct parallel runs, and submit impact assessments to the RBI. |

Pilot and Validation Phase | The RBI reviews impact assessments, provides feedback, and works with banks to refine model outputs and ensure comparability across the system. |

Transition Phase | Formal adoption with transitional capital relief, wherein additional provisioning required under ECL is phased in over a period of four years. |

Full Implementation | Complete migration to ECL-based provisioning with full regulatory oversight and supervisory review of models. |

The RBI has been in active consultation with banks, the Institute of Chartered Accountants of India (ICAI), and international bodies including the Basel Committee on Banking Supervision (BCBS) to ensure the framework is robust yet implementable.

Fitch's Assessment: A Vote of Confidence

In a recent note, Fitch Ratings observed that Indian banks are well-placed to transition to ECL provisioning, citing improved asset quality, higher existing provision coverage ratios (PCRs), and strengthened capitalisation across the system. Major banks such as State Bank of India, HDFC Bank, ICICI Bank, and Axis Bank have invested significantly in credit risk infrastructure in recent years, positioning them ahead of smaller peers in terms of ECL readiness. However, Fitch also cautioned that some mid-sized and smaller banks may face more pronounced capital headwinds during the transition.

How ECL Will Impact Bank Profitability and Capital Ratios

The financial implications of transitioning to an ECL framework are far-reaching and nuanced. For Indian banking professionals, understanding these impacts is critical for strategic planning, investor communication, and regulatory engagement.

Higher Upfront Provisioning Requirements

The most immediate effect of ECL adoption will be a day-one provisioning impact — a one-time charge to retained earnings (not through the profit and loss account) representing the difference between existing provisions and the new ECL-based requirement. Analysts estimate this impact could range from ₹30,000 crore to ₹80,000 crore across the banking system as a whole, though the range is wide given differences in portfolio composition, existing PCRs, and modelling assumptions.

Banks that have been prudent in provisioning under the existing IRACP norms — maintaining high PCRs even for standard assets — will face a smaller day-one impact. Banks with leaner provisioning practices may face a more significant hit to their Common Equity Tier 1 (CET1) capital ratios.

Ongoing Volatility in Provisioning Charges

Under ECL, provisioning charges will become more volatile on a quarter-to-quarter basis. This is because ECL estimates are sensitive to changes in macroeconomic forecasts — a deterioration in GDP growth outlook, rising unemployment, or sectoral stress can trigger a significant upward revision in ECL estimates even if no actual defaults have occurred. This is structurally different from the current environment where provisioning increases are triggered by actual NPA classification.

For investors and analysts tracking Indian banks, this means earnings will become harder to predict in the short term, even as the long-term credit quality of the system improves. Bank management will need to invest in robust investor communication frameworks to explain ECL-driven provisioning movements.

Capital Adequacy Considerations

The relationship between ECL provisioning and capital adequacy is complex. Under Basel III norms — as applied in India through RBI's capital adequacy framework — excess provisions (provisions above expected losses) can be counted as Tier 2 capital up to a limit of 1.25% of Risk Weighted Assets (RWAs). As ECL provisions increase, some portion may qualify as Tier 2 capital, partially offsetting the capital erosion effect.

However, the net effect on CET1 capital ratios is likely to be negative, at least initially. The RBI's transitional arrangements — similar to the approach adopted by the European Banking Authority (EBA) when IFRS 9 was introduced in Europe — are expected to allow banks to add back a portion of the day-one impact to CET1 capital, phased out over four years.

Long-Term Benefits: Resilience and Investor Confidence

Beyond the near-term pain, the ECL framework offers substantial long-term benefits for the Indian banking sector:

Smoother credit cycles: Counter-cyclical provisioning buffers mean banks are better capitalised going into downturns, reducing the risk of capital adequacy crises.

Improved pricing discipline: When banks accurately price credit risk from origination, they are incentivised to price loans appropriately, reducing the cross-subsidisation of high-risk lending by low-risk borrowers.

Enhanced comparability: Alignment with IFRS 9 will make Indian banks more comparable to their global peers, potentially improving their attractiveness to foreign institutional investors.

Regulatory trust: A robust ECL framework strengthens the credibility of Indian bank financial statements, which has at times been questioned due to concerns about NPA recognition practices.

Better credit culture: The requirement to model and monitor credit risk at origination and throughout the loan lifecycle is expected to elevate overall credit underwriting and portfolio management standards.

Conclusion: Preparing for a Transformed Provisioning Landscape

The shift to expected credit loss provisioning in Indian banks is not merely an accounting change — it represents a fundamental transformation in how credit risk is identified, measured, and managed across the banking system. It demands investments in data architecture, model governance, talent, and board-level risk oversight that will stretch the capabilities of many institutions, particularly smaller commercial banks.

The RBI's measured, consultation-driven approach to implementation has been reassuring, and the Fitch assessment of India's readiness provides a credible external validation of the progress made. Yet the work ahead is substantial. Banks that treat ECL as an opportunity to build genuinely superior risk management frameworks — rather than a compliance checkbox — will emerge from the transition as more resilient, more trusted, and ultimately more valuable institutions.

For banking professionals, regulators, and investors watching India's financial sector, the ECL transition is one of the most significant structural reforms underway. Understanding its mechanics, its timeline, and its implications is no longer optional — it is essential to navigating the next chapter of Indian banking.