Stand-Up India Scheme: Complete Guide for SC/ST & Women Entrepreneurs

Introduction: Why the Stand-Up India Scheme Matters

The Stand-Up India Scheme for SC/ST women and other underserved communities is one of India's most targeted financial inclusion initiatives. Launched on 5 April 2016 by the Government of India, the scheme mandates that every scheduled commercial bank branch facilitate at least one loan each to a Scheduled Caste (SC) or Scheduled Tribe (ST) borrower and one to a woman entrepreneur — ensuring credit reaches those historically excluded from the formal banking ecosystem.

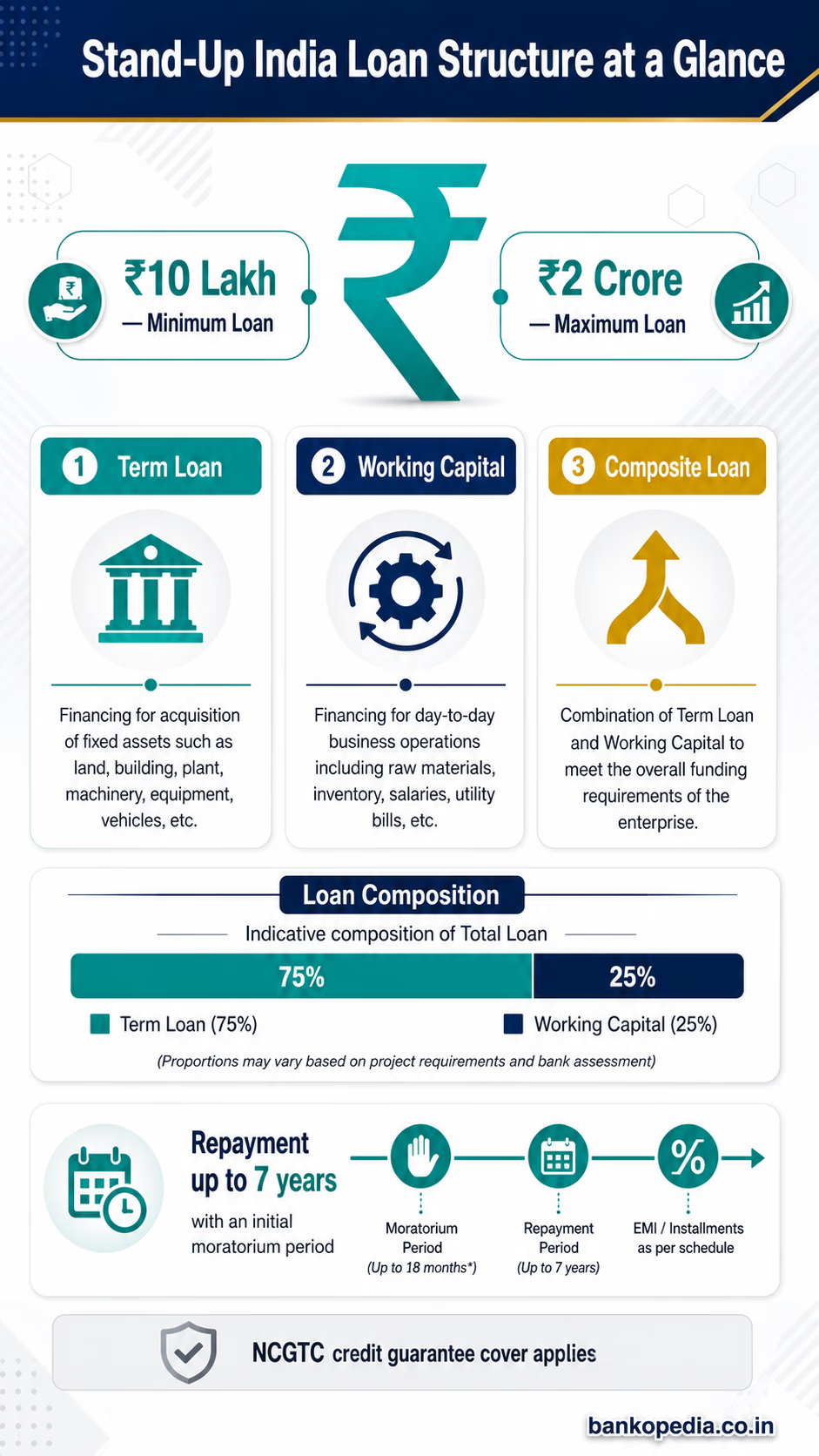

If you belong to the SC, ST, or women entrepreneur category and are looking to start or expand a greenfield enterprise in manufacturing, services, or trading, this scheme offers composite bank loans between ₹10 lakh and ₹2 crore with structured repayment terms and government-backed support infrastructure. The scheme is facilitated by SIDBI (Small Industries Development Bank of India) and monitored through the NCGTC-managed credit guarantee mechanism.

This article explains who qualifies, how to apply, what pitfalls to avoid, and how the Stand-Up India Scheme compares with other government credit programs — helping you make an informed decision before approaching a bank.

What Is the Stand-Up India Scheme for SC/ST & Women Entrepreneurs?

The Stand-Up India Scheme is a central government initiative designed to promote entrepreneurship among India's most economically marginalised groups. The scheme operates through all scheduled commercial banks, including public sector banks, private sector banks, regional rural banks (RRBs), and small finance banks registered under the RBI.

Core Objectives

Facilitate bank credit between ₹10 lakh and ₹2 crore to at least one SC/ST borrower and one woman borrower per bank branch

Enable greenfield enterprise creation — meaning the applicant's first venture in the proposed business sector

Provide composite loans covering working capital and term loan components together

Create an ecosystem of handholding support through trained facilitators and SIDBI's portal

Key Implementing Agencies

SIDBI — manages the Stand-Up India portal (standupmitra.in) and provides handholding support

NCGTC (National Credit Guarantee Trustee Company) — provides credit guarantee cover under the scheme

NABARD — supports outreach in rural and semi-urban areas, especially for agriculture-allied activities

Scheduled Commercial Banks — primary disbursement channel, with branch-level targets

Important: The Stand-Up India Scheme was originally set to run until 2020 and was subsequently extended to 2025. In the 2025-26 Union Budget, the Government of India revamped and relaunched the scheme for the next five years, with the enhanced version slated to run up to 2030–31. This reflects the scheme's continued and growing relevance in India's financial inclusion agenda.

Eligibility Criteria for the Stand-Up India Scheme

Understanding eligibility is the first practical step. The scheme has clearly defined criteria — meeting all of them before applying avoids unnecessary rejections.

Who Can Apply?

Scheduled Caste (SC) entrepreneurs — must provide a valid caste certificate issued by a competent government authority

Scheduled Tribe (ST) entrepreneurs — must provide a valid tribe certificate

Women entrepreneurs — applicable regardless of caste or religion; no income ceiling applies

In the case of non-individual enterprises (partnerships, LLPs, private limited companies), at least 51% shareholding or controlling stake must be held by an SC/ST or woman applicant

Nature of the Business

Must be a greenfield project — the applicant's first enterprise in the manufacturing, services, or trading sector

The enterprise should be in manufacturing, services, or the trading sector (agriculture-allied activities are also eligible)

Existing businesses do not qualify; the scheme specifically targets new ventures

Age and Financial Requirements

Applicant must be 18 years or above

Must not be a defaulter with any bank or financial institution (clean CIBIL / credit bureau record required)

Borrower must contribute a minimum of 10% margin money (own contribution) toward the project cost

Loan Amount and Structure

Parameter | Details |

|---|

Minimum Loan | ₹10 lakh |

Maximum Loan | ₹2 crore (enhanced in 2025-26 Budget revamp) |

Loan Type | Composite (Term Loan + Working Capital) |

Repayment Period | Up to 7 years |

Moratorium Period | Up to 18 months |

Working Capital Component | Via overdraft/cash credit limit (RuPay debit card issued) |

Margin Money | Minimum 10% (can include government subsidies) |

How to Apply for the Stand-Up India Scheme: Step-by-Step Process

The application process is designed to be accessible through multiple channels. Here is how it works in practice:

Step 1: Access the Standup Mitra Portal

Visit standupmitra.in, the official portal managed by SIDBI. You can register as a borrower, access handholding support, and check your nearest bank branch's Stand-Up India loan availability — all in one place.

Step 2: Self-Assessment and Business Plan Preparation

Before approaching a bank, prepare a detailed business plan that includes:

Nature of the greenfield enterprise

Projected revenues and profitability for at least 3 years

Total project cost and break-up (land, equipment, working capital)

Means of financing (own contribution + bank loan)

If you need help with your business plan, SIDBI facilitators and District Industries Centres (DICs) offer free guidance.

Step 3: Choose Your Bank Branch

You can approach any scheduled commercial bank branch directly. Under the scheme's mandate, every branch must process and facilitate these loans. Use the portal to identify branches in your region that are actively disbursing Stand-Up India loans.

Step 4: Submit the Application with Documents

Typical documentation requirements include:

KYC documents (Aadhaar, PAN card)

SC/ST certificate or proof of gender (for women applicants)

Proof of business address and registration (Udyam Registration Certificate recommended)

Detailed project report

Bank statements (last 6–12 months if any prior account exists)

Quotations for machinery or equipment to be procured

Photographs and declaration of greenfield status

Step 5: Credit Assessment and Sanction

The bank conducts a credit appraisal of the project. Given the scheme's mandate, banks are expected to be supportive rather than purely commercial in their assessment, but basic credit viability must still be demonstrated. After sanction, the bank issues a composite loan with a working capital component delivered via a RuPay debit card — a distinct feature of this scheme.

Step 6: Credit Guarantee Cover

All Stand-Up India loans are eligible for coverage under NCGTC's Stand-Up India Credit Guarantee Scheme, which provides collateral-free protection to lenders. This significantly improves loan approval rates for applicants who lack traditional collateral. This is conceptually similar to how the [[Link to CGTMSE Guarantee Scheme: Complete Guide for MSMEs]] works for MSMEs more broadly.

Interest Rates, Repayment, and Financial Terms

Interest Rate Structure

The scheme does not prescribe a fixed interest rate. The guidelines specify that the rate should be the lowest applicable rate for that category at the bank. Under the original scheme guidelines, this was expressed as not exceeding the base rate (MCLR) plus 3% plus tenor premium. However, applicants should note that the Reserve Bank of India (RBI) has since mandated that all new floating-rate loans to MSMEs be linked to an External Benchmark Lending Rate (EBLR) — typically the Repo Rate — rather than the internal MCLR. When approaching your bank, ask specifically about the EBLR-linked rate applicable to your Stand-Up India loan. In practice, effective rates typically range between 8% and 12% per annum depending on the bank, the prevailing Repo Rate, and the borrower's profile.

Working Capital Facility

The working capital component within the composite loan is sanctioned as a cash credit limit, and a RuPay debit card is issued to the borrower for transactional convenience. This is designed to bring SC/ST and women entrepreneurs directly into the formal digital banking ecosystem.

Repayment Flexibility

Maximum repayment period: 7 years

Moratorium: Up to 18 months from date of first disbursement

Working capital drawdowns are repayable as per overdraft/cash credit norms

Collateral Requirements

While the credit guarantee mechanism under NCGTC provides cover, banks may still ask for primary security in the form of assets created from the loan. Third-party guarantees are not mandatory, but some banks may request them depending on internal policy. Applicants should clarify this upfront.

Stand-Up India vs. Other Government Schemes: Key Differences

Many applicants confuse Stand-Up India with other MSME credit programs. Here is a structured comparison to help you choose the right scheme for your needs.

Feature | Stand-Up India | Mudra Loan (PMMY) | PMEGP |

|---|

Target Beneficiary | SC/ST & Women only | All micro entrepreneurs | Unemployed youth & artisans |

Loan Range | ₹10 lakh – ₹2 crore | Up to ₹20 lakh | Up to ₹50 lakh (mfg) / ₹20 lakh (service) |

Subsidy Available | No (margin money support only) | No | Yes (15%–35% of project cost) |

Greenfield Requirement | Yes | No | Yes |

Credit Guarantee | NCGTC (Stand-Up India) | NCGTC (CGFMU) | CGTMSE |

Disbursing Agency | Scheduled Commercial Banks | Banks, MFIs, NBFCs | Banks + KVIC/DIC/Khadi Boards |

For a deeper comparison of credit options available to small businesses, see [[Link to Mudra Loan vs Bank Loan: Which is Better for MSMEs?]] and [[Link to PMEGP – Prime Minister Employment Generation Program – Complete Revised Guidelines]].

If your enterprise will involve invoice-based cash flow management as it scales, [[Link to What is TReDS? How MSME Invoice Discounting Works]] is a useful follow-on resource.

Common Mistakes to Avoid When Applying

Despite the scheme's inclusive design, many eligible applicants face rejection or delays due to avoidable errors. Here are the most common pitfalls:

1. Applying for an Existing Business

The greenfield clause is non-negotiable. If you already operate a business — even informally — in the same sector, you will not qualify. Banks verify this through GST registration data, Udyam records, and applicant declarations.

2. Inadequate Business Plan

A vague or unrealistic project report is the single biggest reason for rejection. Your financial projections must demonstrate how the business will generate sufficient cash flow to service the loan within the moratorium and repayment window. Use SIDBI's free facilitation support at standupmitra.in before approaching the bank.

3. Poor Credit History

A default on any previous credit facility — even a small personal loan — will disqualify you. Check your CIBIL score before applying. If there is any settled or written-off account, address it proactively with the concerned lender first.

4. Incorrect Documentation of Caste/Tribe Status

The caste/tribe certificate must be issued by the competent authority as per the state government's format. Certificates from unofficial or village-level bodies are not accepted. Women applicants must provide gender-valid KYC documents matching the entity's ownership records.

5. Confusing Composite Loan with Separate Facilities

Some applicants approach banks for only a term loan or only a working capital limit. The Stand-Up India product is a composite facility — both components must be applied for together, as a single loan account.

6. Not Registering on the Standup Mitra Portal

Registration on the portal connects you with handholding agencies, tracks your application status, and flags your requirement to nearby bank branches. Skipping this step reduces visibility and support access.

Practical Tips to Maximise Your Chances of Approval

Register your enterprise under Udyam before applying — this adds legitimacy and is increasingly required by banks

Open a current or savings account with the bank you intend to borrow from — prior banking relationship improves trust

Combine with state government subsidies — many state governments offer additional margin money support for SC/ST and women entrepreneurs which can reduce your own contribution below 10%

Seek handholding — SIDBI-empanelled facilitators can help with project reports, documentation, and bank liaison at no cost

Ask about interest subvention — some banks offer additional rate concessions for women borrowers under their own schemes; always negotiate

Keep your enterprise account active and compliant — post-disbursement, maintain GST filings and submit utilisation certificates as required to avoid account reclassification

Conclusion: Actionable Takeaways for Aspiring Entrepreneurs

The Stand-Up India Scheme for SC/ST women and other eligible entrepreneurs fills a genuine gap in India's MSME credit landscape — providing substantial, composite financing of up to ₹2 crore (as enhanced under the 2025-26 Budget revamp) with a supportive credit guarantee framework and structured repayment terms. Unlike smaller micro-loan schemes, this is serious growth capital designed to fund meaningful greenfield businesses, and the scheme is now extended to run through 2030–31.

Here is what you should do next:

Confirm your eligibility: SC/ST certificate or women-owned majority stake, greenfield business, clean credit record

Register on standupmitra.in and connect with a SIDBI facilitator

Prepare a robust project report with realistic financials

Approach your preferred scheduled commercial bank branch with complete documentation

Ensure the loan is structured as a composite facility with both term loan and working capital components

The scheme is not a subsidy — it is a loan that must be repaid. Treat it as institutional capital for a viable business, plan carefully, and it can be a transformative financial resource for first-generation entrepreneurs from SC, ST, and women categories across India.

Frequently Asked Questions (FAQs)

Q1. Can a woman entrepreneur from the general category apply for the Stand-Up India Scheme?

Yes. The scheme has two distinct targets per bank branch — one loan to an SC or ST borrower, and one loan to a woman borrower. A woman from the general or OBC category qualifies under the woman entrepreneur category without any caste restriction.

Q2. What does "greenfield" mean in the context of the Stand-Up India Scheme?

Greenfield means the applicant's first enterprise in the proposed sector. If you run a tailoring shop and want a loan to start a food processing unit, the food processing unit qualifies as a greenfield project. However, expanding the existing tailoring business would not qualify.

Q3. Is collateral mandatory for a Stand-Up India loan?

Not strictly. The loan is covered under NCGTC's credit guarantee mechanism, which provides collateral-free protection. However, the primary assets created from the loan proceeds (machinery, equipment) typically serve as primary security. Individual banks may have internal policies requiring additional collateral — clarify this before applying.

Q4. Can a private limited company apply for the Stand-Up India Scheme?

Yes. Non-individual entities including partnerships, LLPs, and private limited companies are eligible, provided that at least 51% of the shareholding and controlling stake is held by an SC/ST individual or a woman. The controlling nature of the stake — not merely nominal shareholding — is verified by banks.

Q5. How is the Stand-Up India Scheme different from a Mudra loan?

Mudra loans (under PMMY) are available to all micro entrepreneurs up to ₹20 lakh, with no restriction on existing businesses. The Stand-Up India Scheme is exclusively for SC/ST and women entrepreneurs, covers loans up to ₹2 crore, and mandates a greenfield project. Mudra also channels funds through NBFCs and MFIs, while Stand-Up India is limited to scheduled commercial banks. See [[Link to Mudra Loan vs Bank Loan: Which is Better for MSMEs?]] for a detailed comparison.

Q6. What happens if my application is rejected by the bank?

If a branch rejects your application without adequate reason, you can escalate through the Standup Mitra portal, which connects you with senior banking officials and SIDBI facilitators. You can also approach another bank branch, as the scheme's mandate applies across all scheduled commercial bank branches. Persistent unexplained rejection can be flagged to the RBI's banking ombudsman under fair lending practice norms.