Atal Pension Yojana (APY): Guaranteed Pension for Unorganised Sector Workers

The Atal Pension Yojana APY scheme is one of India's most important social security initiatives, designed specifically to provide financial stability to workers in the unorganised sector after retirement. Launched in May 2015 by the Government of India and regulated by the Pension Fund Regulatory and Development Authority (PFRDA), APY guarantees a fixed monthly pension ranging from ₹1,000 to ₹5,000 — a lifeline for millions of Indians who lack formal employment benefits. This article explains everything you need to know about APY: who can join, how contributions work, what benefits are guaranteed, and how to enrol. Whether you are a daily wage worker, domestic help, street vendor, or small farmer, understanding this scheme can make the difference between a dignified retirement and financial hardship. For a broader view of government schemes protecting Indian citizens financially, see [[Link to Government Schemes for Financial Inclusion and Social Security in India 2026: Complete Guide to PMJDY, PMJJBY, PMSBY, APY, PM-SYM & NPS]].

What Is the Atal Pension Yojana APY Scheme?

APY is a defined benefit pension scheme — meaning the pension amount you receive at retirement is fixed and guaranteed, regardless of market performance. This distinguishes it from market-linked schemes like the National Pension System (NPS), where returns depend on investment performance.

The scheme is administered by PFRDA through the NPS architecture, but its benefits and contribution structure are entirely separate from NPS. Your contributions are pooled and managed by designated pension fund managers, but the Government of India guarantees the promised pension amount. If actual investment returns fall short of what is needed to deliver the guaranteed pension, the government makes up the difference.

Key Objectives of APY

Provide old-age income security to workers in the unorganised sector

Encourage voluntary savings among low-income groups

Reduce dependence on informal support systems and family during old age

Extend the reach of formal financial services to those outside the organised workforce

APY operates through a bank account — subscribers must have a savings account with any scheduled commercial bank, small finance bank, or post office savings bank. This link to the banking system also promotes financial inclusion, complementing initiatives like the Pradhan Mantri Jan Dhan Yojana (PMJDY). If you do not yet have a bank account, read our guide on [[Link to PMJDY: Zero-Balance Accounts, Overdraft Facility, and Financial Inclusion Banking]] to understand how to open one at zero cost.

Eligibility Criteria: Who Can Join APY?

APY has clear and simple eligibility requirements. Meeting all of the following conditions makes you eligible to subscribe:

Age: You must be between 18 and 40 years of age at the time of enrolment

Bank account: A savings account with a participating bank or post office is mandatory

Aadhaar and mobile number: Required for KYC verification and contribution tracking

Not an income taxpayer (for new enrolments from October 2022): From October 1, 2022, individuals who are income tax payers are not eligible to open a new APY account. However, this restriction applies only to new enrolments — subscribers who joined APY before October 1, 2022 are grandfathered in and may continue their accounts even if they subsequently become income taxpayers

EPF or other statutory social security scheme membership does not disqualify you: Any Indian citizen aged 18–40 who meets the other eligibility criteria can open an APY account regardless of their EPF or similar scheme membership. The restriction on statutory scheme membership historically applied only to eligibility for the Government Co-contribution benefit (active 2015–2020) and is no longer a bar to joining APY itself

NRI eligibility: Indian citizens who are Non-Resident Indians (NRIs) are fully eligible to open APY accounts, provided they are aged 18–40 and hold a valid Indian bank account with a participating Point of Presence (bank branch). APY eligibility is based on Indian citizenship, not residency. The only restriction applies if a subscriber subsequently gives up Indian citizenship — in that case, the account is closed and the accumulated corpus is refunded without the government co-contribution.

The minimum age of 18 ensures that even young workers entering the informal labour market can start building their retirement corpus early, which significantly reduces the monthly contribution needed.

Important Note on the Tax Payer Restriction

The October 2022 amendment specifically targets APY's intended beneficiaries — the economically weaker sections and unorganised workers. If you are a new applicant who files income tax returns, APY is not the appropriate scheme for you. Consider the National Pension System (NPS) instead, which offers market-linked returns with additional tax benefits under Section 80CCD. Importantly, if you were already an APY subscriber before October 1, 2022, you are not required to exit merely because you have since become an income taxpayer — your account continues normally and your guaranteed pension at age 60 remains intact.

Pension Amounts and Contribution Structure

The defining feature of the Atal Pension Yojana APY scheme is its guaranteed pension at age 60. Subscribers choose a pension amount at enrolment, and their monthly contributions are determined accordingly based on their age.

Available Pension Slabs

Monthly Pension Amount | Lump Sum Return to Nominee (on subscriber's death) | Corpus at Age 60 |

|---|

₹1,000 | ₹1.7 lakh | ₹1.7 lakh |

₹2,000 | ₹3.4 lakh | ₹3.4 lakh |

₹3,000 | ₹5.1 lakh | ₹5.1 lakh |

₹4,000 | ₹6.8 lakh | ₹6.8 lakh |

₹5,000 | ₹8.5 lakh | ₹8.5 lakh |

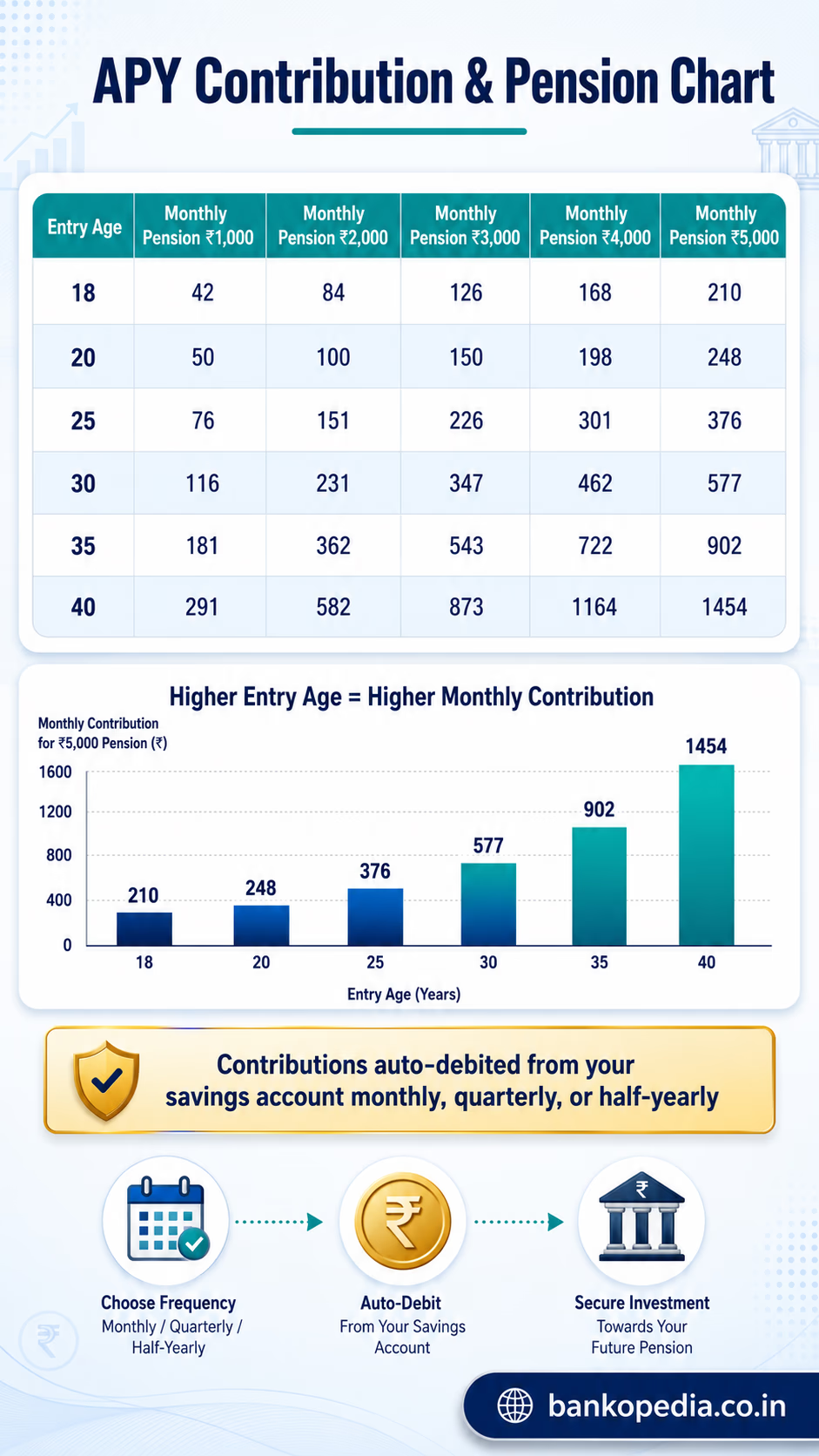

How Monthly Contributions Are Calculated

Your monthly contribution depends on two factors: the pension amount you choose and your age at enrolment. The younger you are when you join, the lower your monthly contribution, because your money has more time to grow.

Below are indicative monthly contribution amounts for the ₹5,000 pension slab:

Age 18: ₹210 per month

Age 25: ₹376 per month

Age 30: ₹577 per month

Age 35: ₹902 per month

Age 40: ₹1,454 per month

For the ₹1,000 pension slab, the contributions are significantly lower — as little as ₹42 per month for an 18-year-old enrollee. Contributions are auto-debited from your linked savings account on a monthly, quarterly, or half-yearly basis.

Spousal Benefits

APY includes strong survivor protection. Upon the subscriber's death after age 60, the spouse receives the same monthly pension for the rest of their life. After both the subscriber and spouse pass away, the entire accumulated corpus is returned to the nominated beneficiary as a lump sum.

How to Enrol in APY: Step-by-Step Process

Joining the Atal Pension Yojana APY scheme is straightforward. You can enrol through your bank branch, internet banking portal, or the APY mobile application.

Offline Enrolment (Bank Branch)

Visit any branch of your savings account bank

Request the APY registration form (available at the branch or downloadable from PFRDA's website)

Fill in personal details: name, date of birth, Aadhaar number, nominee details, and preferred pension amount

Provide your savings account number and ensure sufficient balance for the first contribution

Submit the completed form with a copy of your Aadhaar card

The bank will process your enrolment and activate auto-debit within 30 days

Online Enrolment

Log in to your bank's net banking portal

Navigate to the "Government Schemes" or "Social Security Schemes" section

Select Atal Pension Yojana and complete the application form

Verify your Aadhaar-linked mobile number via OTP

Choose your pension amount and contribution frequency

Confirm auto-debit authorisation and submit

You will receive a Permanent Retirement Account Number (PRAN) upon successful enrolment. This unique number identifies your APY account and is used for all future transactions, including changing your pension amount or updating nominee details.

Changing Pension Amount After Enrolment

APY allows you to upgrade or downgrade your pension slab once per financial year. As per PFRDA guidelines updated effective July 1, 2020, this change is no longer restricted to the month of April — subscribers may make this adjustment at any time during the financial year. This flexibility lets you increase your pension goal as your income grows, or reduce contributions during financially difficult periods.

Tax Benefits and Government Co-Contribution

Tax Deduction Under Section 80CCD(1B)

APY contributions qualify for tax deduction under Section 80CCD(1B) of the Income Tax Act, providing an additional deduction of up to ₹50,000 over and above the standard ₹1.5 lakh limit under Section 80C. However, since income taxpayers became ineligible to open new APY accounts from October 2022, this benefit primarily applies to existing subscribers who were enrolled before the restriction came into effect.

Earlier Government Co-Contribution (Historical Context)

When APY was first launched in 2015–16, the Government of India co-contributed 50% of the subscriber's annual contribution or ₹1,000 per year, whichever was lower, for subscribers who joined between June 2015 and March 2016 and were not income tax payers. This co-contribution was available for five years (up to 2019–20). While this co-contribution period has ended, it significantly boosted early adoption of the scheme.

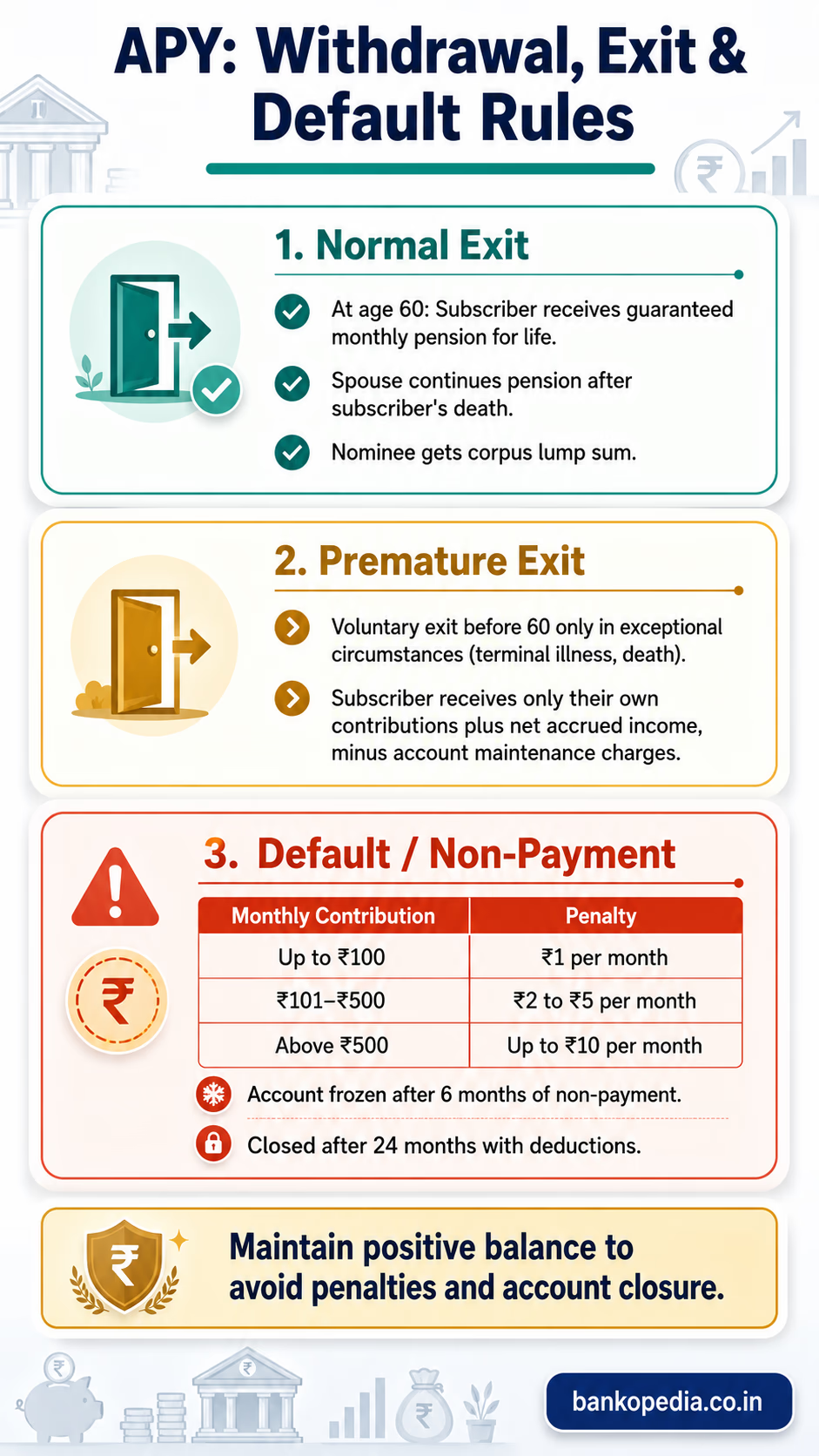

Penalties, Exits, and Account Maintenance

Penalty for Delayed Contributions

If your linked bank account does not have sufficient balance on the due date, your APY contribution will not be auto-debited. PFRDA levies overdue penalties as follows:

₹1 per month for contributions up to ₹100

₹2 per month for contributions between ₹101 and ₹500

₹5 per month for contributions between ₹501 and ₹1,000

₹10 per month for contributions above ₹1,000

Continued non-payment does not result in permanent account closure. Under updated PFRDA guidelines, an APY account is never permanently closed purely due to non-payment of contributions. Instead, the bank continues to deduct periodic account maintenance charges from the accumulated corpus. While sustained non-payment can gradually erode the corpus balance, the subscriber can regularise the account at any time before age 60 by paying the pending overdue contributions along with accrued penalty interest.

Voluntary Exit Before Age 60

PFRDA permits voluntary exit from APY at any time and for any reason before age 60. Upon voluntary exit, the subscriber receives their total contributions plus accrued net interest, minus account maintenance charges. The government's assured return above actual investment returns is not applicable for premature exits. Additionally, if the subscriber received the government's co-contribution between 2015 and 2020, that co-contribution and the interest earned on it are forfeited upon voluntary exit. There is no restriction that limits voluntary exit only to exceptional circumstances such as terminal illness — any subscriber may choose to exit voluntarily.

If you are exploring other retirement savings options and considering exiting, it is worth reading about [[Link to What Happens If You Stop NPS Contributions?]] to understand the implications of discontinuing pension contributions more broadly.

Death Before Age 60

If the subscriber dies before reaching 60, the spouse has the option to continue the APY account under their name until maturity, thereby retaining the right to the guaranteed pension. Alternatively, the spouse can choose to close the account and receive the accumulated corpus as a lump sum.

Common Mistakes to Avoid When Using APY

Many subscribers fail to maximise the benefits of the Atal Pension Yojana APY scheme due to avoidable errors. Here are the most frequent mistakes and how to prevent them:

Insufficient bank balance on auto-debit date: Always maintain at least 2–3 months' worth of contributions in your linked account as a buffer. Set a reminder or maintain a separate savings sub-account for APY

Not updating nominee details: Life circumstances change. Update your nominee details after marriage, the birth of a child, or the death of a nominee to ensure the lump sum reaches the right person

Choosing too low a pension slab to minimise contributions: ₹1,000 per month in retirement will not be sufficient even at current prices, let alone 20–30 years from now. Choose the highest slab you can afford, especially if you are enrolling young

Delaying enrolment: Every year you wait significantly increases your required monthly contribution. A 25-year-old pays ₹376/month for ₹5,000 pension; a 35-year-old pays ₹902/month for the same

Not keeping PRAN details safe: Your PRAN is essential for managing your APY account. Store it securely and register your mobile number for SMS alerts

Assuming APY replaces all retirement needs: APY provides a base income of up to ₹5,000/month. Supplement it with other savings instruments if possible

Conclusion: Is APY the Right Scheme for You?

The Atal Pension Yojana APY scheme fills a critical gap in India's social security framework. For the hundreds of millions of workers in agriculture, construction, domestic work, retail, and other informal sectors — people with no employer-provided pension or provident fund — APY offers the closest thing to a guaranteed retirement income available in India today.

The scheme's strengths are clear: government-backed guarantee, low and flexible contributions, spousal pension protection, and simple enrolment. Its limitations are equally clear: the maximum pension of ₹5,000/month may not be sufficient as a standalone retirement income, and new enrolments are now restricted to non-taxpayers.

Actionable takeaways:

If you are between 18 and 40, work in the unorganised sector, and are not an income taxpayer, enrol in APY immediately — the cost of waiting is measurable in higher future contributions

Choose the highest pension slab (₹5,000/month) if you can afford it — this provides both the maximum income and the maximum corpus for your nominee

Link APY to a Jan Dhan account if you have one, and ensure regular balance maintenance to avoid penalties

Treat APY as your retirement foundation and build additional savings on top of it

For a comprehensive understanding of how APY fits within India's broader financial inclusion and social security ecosystem — including PMJDY, PMJJBY, PMSBY, and PM-SYM — refer to our detailed guide: [[Link to Government Schemes for Financial Inclusion and Social Security in India 2026: Complete Guide to PMJDY, PMJJBY, PMSBY, APY, PM-SYM & NPS]].

Frequently Asked Questions (FAQs)

Can a husband and wife both have separate APY accounts?

Yes. APY allows only one account per individual, but a husband and wife can each hold their own separate APY account. This means a couple can collectively receive up to ₹10,000 per month in guaranteed pension if both opt for the ₹5,000 slab.

What happens to my APY account if I become a salaried employee and start paying income tax?

It depends on when you enrolled. If you joined APY before October 1, 2022, you are grandfathered in — you are not required to exit and your account continues normally. You will receive your guaranteed pension at age 60 even if your income has since increased and you now pay income tax. If you enrolled on or after October 1, 2022, the income taxpayer restriction applies to new enrolments, and you would not have been eligible to join at that point. Existing pre-October 2022 subscribers who become taxpayers should consider complementing their APY with NPS for additional retirement savings, but they do not need to close their APY account.

Can I change my pension amount after enrolling in APY?

Yes. You can upgrade or downgrade your chosen pension slab once per financial year. As per updated PFRDA guidelines effective July 1, 2020, this change is no longer restricted to the month of April and can be made at any point during the financial year. Your contribution amount will be revised accordingly based on your current age at the time of the change.

Is the ₹5,000 monthly pension from APY adjusted for inflation over the years?

No. The pension amount under APY is fixed and not inflation-indexed. The ₹5,000/month you receive at 60 will be the same nominal amount throughout your retirement, regardless of rising prices. This is an important limitation to account for when planning your overall retirement strategy.

What if I miss several months of APY contributions?

Missing contributions attracts monthly penalties (₹1 to ₹10 per month depending on contribution size). However, under updated PFRDA guidelines, an APY account is never permanently closed solely due to non-payment. The account remains active, and the bank deducts periodic account maintenance charges from the accumulated corpus. You can regularise your account at any time before age 60 by paying the overdue contributions and accrued penalty interest. Prolonged non-payment can erode your corpus through maintenance charges, so it is advisable to regularise arrears as soon as possible.

Can NRI (Non-Resident Indian) workers join APY?

Yes. APY is available to all Indian citizens aged 18–40 years, including Non-Resident Indians (NRIs). The scheme is based on citizenship, not residency. As long as an NRI holds Indian citizenship, is within the eligible age bracket, and maintains a valid Indian bank account with a Point of Presence (participating bank branch), they can enrol in APY. The only geographic restriction arises if a subscriber subsequently gives up their Indian citizenship — in that case, the APY account is closed and the accumulated corpus is refunded, without the government co-contribution.