Introduction: Why PMJDY Remains India's Most Transformative Banking Reform

The Pradhan Mantri Jan Dhan Yojana (PMJDY) is not merely a government scheme — it is the financial backbone that connected over 53 crore previously unbanked Indians to the formal economy. Launched on 28 August 2014 by Prime Minister Narendra Modi, PMJDY redefined what banking access means for the country's rural poor, migrant workers, women, and daily wage earners. At its core, the scheme offers zero-balance savings accounts, an overdraft facility, and a comprehensive insurance and pension ecosystem — all under one roof.

This article breaks down exactly how PMJDY works in practice: who qualifies, how to open an account, what the overdraft limit is in 2025–26, how the RuPay debit card functions, and what benefits you may be leaving on the table if you have a dormant Jan Dhan account. Whether you are a first-generation bank account holder or a financial professional advising underserved clients, this guide gives you the full picture. For a broader view of government-backed financial protection schemes, see - Link to Government Schemes for Financial Inclusion and Social Security in India 2026: Complete Guide to PMJDY, PMJJBY, PMSBY, APY, PM-SYM & NPS.

What Is Pradhan Mantri Jan Dhan Yojana (PMJDY)? Core Features Explained

PMJDY is a national financial inclusion mission administered by the Ministry of Finance and implemented through public sector banks, regional rural banks (RRBs), cooperative banks, and India Post Payments Bank. The scheme operates under a "6-pillar" framework designed to ensure universal access to banking, credit, insurance, and pension services.

Six Core Pillars of PMJDY

Universal Access to Banking Facilities: Every household in India — urban or rural — gets access to a bank branch or a Business Correspondent (BC) agent within 5 km.

Zero-Balance Basic Savings Bank Deposit (BSBD) Account: No minimum balance requirement. No penalty for zero balance.

Financial Literacy Programme: Account holders receive financial literacy materials covering savings, credit, insurance, and pension.

Credit Guarantee Fund: A ₹1,000 crore corpus to guarantee overdraft loans extended under the scheme.

Micro Insurance: Accidental and life insurance coverage via PMSBY and PMJJBY linked to the RuPay card.

Pension/Unorganised Sector: Gateway to Atal Pension Yojana (APY) and PM-SYM for retirement security.

Key Statistics as of 2025

Metric | Data (as of March 2025) |

|---|

Total PMJDY accounts | Over 53.13 crore |

Total deposits in PMJDY accounts | Over ₹2.31 lakh crore |

RuPay debit cards issued | Over 36.15 crore |

Female account holders | Approximately 55.6% of total accounts |

Rural/semi-urban accounts | Over 66% of total accounts |

These figures, sourced from the Ministry of Finance's PMJDY progress dashboard, illustrate the scheme's unmatched reach in delivering financial inclusion at scale.

Zero-Balance Account: What It Actually Means and What You Get

The most defining feature of a Jan Dhan account is that it is a Basic Savings Bank Deposit (BSBD) account — a special category introduced by the Reserve Bank of India (RBI) specifically to remove the minimum balance barrier that kept millions outside the banking system.

Features of the PMJDY Zero-Balance Account

No minimum balance: You can hold ₹0 in your account without any charges or penalties.

Interest on deposits: Interest is paid at the rate applicable to savings accounts (currently 2.70%–4% per annum, depending on the bank).

Free RuPay debit card: A RuPay Classic or RuPay Platinum card with ₹1 lakh to ₹2 lakh accidental death insurance coverage.

Free passbook facility: Physical passbook provided at no charge.

Up to 4 free withdrawals per month: At ATMs and bank branches combined, free of charge.

Direct Benefit Transfer (DBT) eligibility: All government subsidies — LPG, NREGA wages, scholarships — flow directly into the account, eliminating leakage.

Mobile banking access: Basic mobile banking via USSD (*99#) for feature phones without internet.

No chequebook by default: A chequebook can be issued if minimum conditions are satisfied and the bank's internal norms permit.

Difference Between BSBD Account and Regular Savings Account

A BSBD account under PMJDY cannot be held simultaneously with a regular savings account at the same bank. If a regular account already exists, it must be converted or closed when opening a BSBD account. RBI guidelines explicitly prohibit holding both account types with the same institution.

This distinction matters for urban workers who may already have salary accounts. They should verify their existing account type before applying under PMJDY to remain compliant with RBI norms.

Overdraft Facility Under PMJDY: Eligibility, Limits, and How to Access It

One of the most underutilised benefits of PMJDY is the overdraft (OD) facility — a small, collateral-free credit line that functions as an emergency credit buffer for account holders with no credit history.

Current Overdraft Limits (Revised in August 2018)

Category | Overdraft Limit |

|---|

Basic overdraft (after 6 months of satisfactory account operation) | Up to ₹10,000 |

Without conditions (automatic for first 6 months) | Up to ₹2,000 (seed overdraft) |

Age eligibility range | 18 to 65 years |

Who Is Eligible for the PMJDY Overdraft Facility?

The account must have been active for at least 6 months with regular transactions (deposits and withdrawals).

Only one adult per household — preferably the woman of the household — is eligible for the OD facility.

The account holder must be between 18 and 65 years of age.

A satisfactory credit track record with no defaults on any prior loans is required.

The account should have no history of overdraft misuse or unauthorised negative balance.

How to Apply for the Overdraft Facility

Visit the home branch where the Jan Dhan account is held.

Submit a written request or fill the bank's OD application form.

Provide proof of identity, address, and account activity statement (passbook).

The bank's Business Correspondent (BC) can also facilitate this process in rural areas.

Approval is at the bank's discretion based on account activity and RBI/government guidelines.

Important Points About the Overdraft

The OD is a revolving credit facility, not a term loan. You draw, repay, and redraw as needed.

Interest is charged only on the amount utilised, not the full ₹10,000 sanctioned limit.

Non-repayment affects your credit history with Credit Information Bureau India Limited (CIBIL), as banks increasingly report PMJDY OD defaults to credit bureaus.

The Credit Guarantee Fund (₹1,000 crore corpus) backs defaults, reducing the bank's risk — but this does not absolve the borrower of repayment obligations.

RuPay Debit Card and Insurance Benefits Bundled with PMJDY

Every PMJDY account holder receives a RuPay debit card — a domestically developed card network managed by the National Payments Corporation of India (NPCI). This card is not merely a payment tool; it is the access key to two major insurance covers.

Insurance Benefits via RuPay Card

Insurance Type | Coverage | Condition |

|---|

Accidental Death & Disability (AD&D) Insurance | ₹1 lakh (Classic) / ₹2 lakh (Platinum) | Card must have been used at least once in 45 days prior to the accident |

Life Insurance Cover (for new accounts opened between 15 Aug 2014 and 26 Jan 2015) | ₹30,000 | Only for those who were unbanked at the time of account opening |

The ₹2 lakh accidental coverage under the RuPay Platinum card is particularly significant — it is available at zero annual premium to the account holder. The premium is settled between NPCI and the insurer (currently under IRDAI-regulated general insurance companies).

Linking PMJDY to PMJJBY and PMSBY

PMJDY accounts serve as the premium deduction platform for the government's micro-insurance schemes:

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY): ₹2 lakh life insurance cover at just ₹436/year (FY 2024–25 premium), auto-debited from the Jan Dhan account.

Pradhan Mantri Suraksha Bima Yojana (PMSBY): ₹2 lakh accidental death cover at ₹20/year, also auto-debited.

For detailed coverage of these linked schemes and how they work together as a social security ecosystem, refer to [[Link to Government Schemes for Financial Inclusion and Social Security in India 2026: Complete Guide to PMJDY, PMJJBY, PMSBY, APY, PM-SYM & NPS]].

How to Open a PMJDY Account: Step-by-Step Eligibility and Process

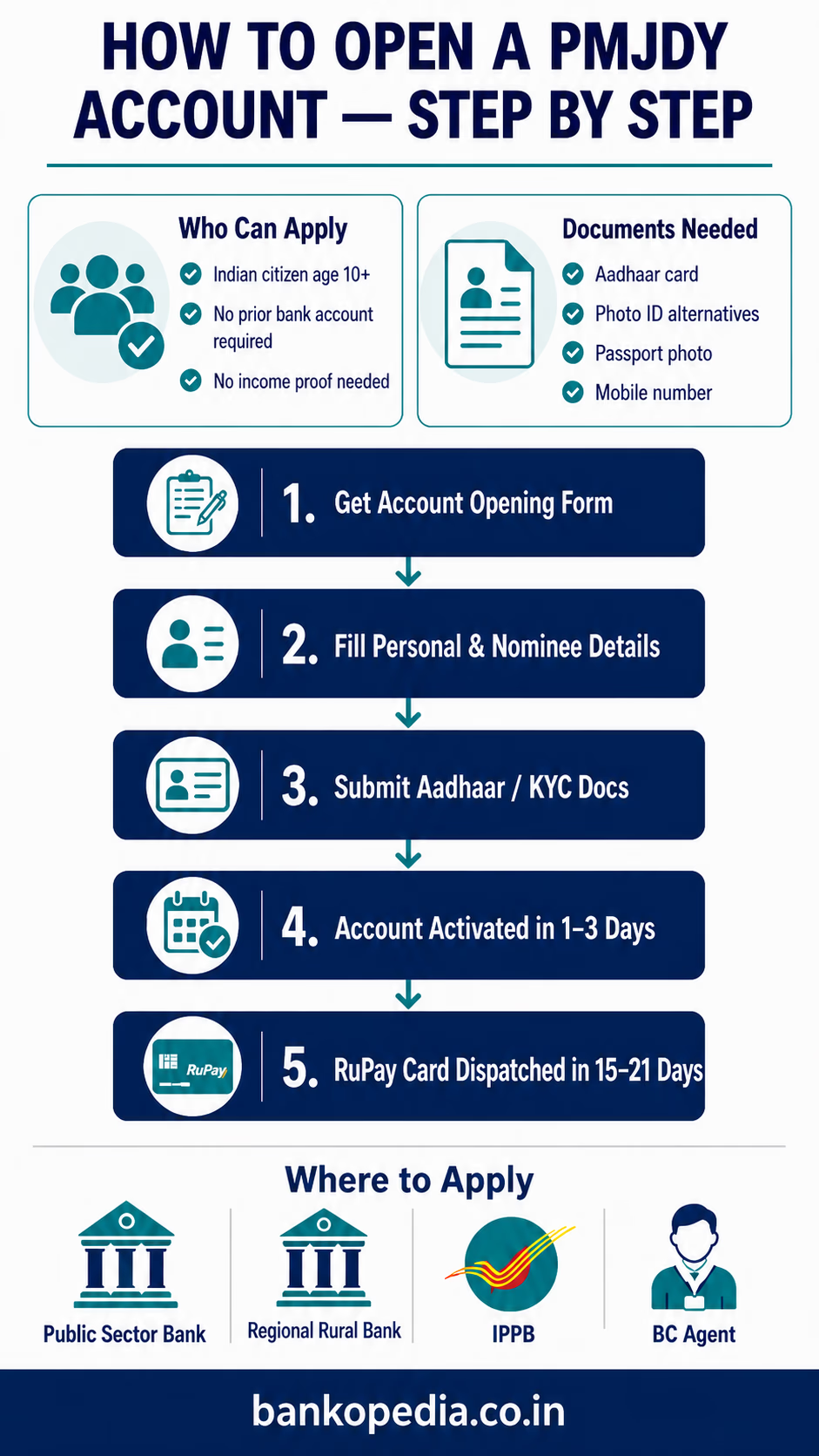

Who Can Open a PMJDY Account?

Any Indian citizen above 10 years of age (minors need guardian supervision).

Individuals with no existing bank account — those already banked can open accounts too but may need to close existing savings accounts at the same bank.

No income proof required — the scheme is open regardless of income level.

Documents Required

Aadhaar card (primary KYC document — simplifies the process significantly)

If no Aadhaar: Voter ID, driving licence, PAN card, NREGA job card, or any government-issued photo ID

Passport-size photograph

Mobile number (for SMS alerts and USSD banking)

Where to Open the Account

Any public sector bank branch (SBI, PNB, Bank of Baroda, Canara Bank, etc.)

Any Regional Rural Bank (RRB) or cooperative bank

India Post Payments Bank (IPPB) — especially useful in remote villages

Business Correspondent (BC) agents — bank mitras operating in villages where no branch exists

Account Opening Process

Obtain the PMJDY account opening form from the bank, BC agent, or download from the bank's website.

Fill in personal details — name, address, mobile number, nominee details.

Submit with Aadhaar or alternative KYC document.

Provide a self-attested photograph.

The account is typically activated within 1–3 working days.

The RuPay debit card is dispatched by post (usually within 15–21 days).

Practical Tips and Common Mistakes to Avoid with Your PMJDY Account

Practical Tips to Maximise PMJDY Benefits

Keep the RuPay card active: Use your card at least once every 45 days to maintain eligibility for the accidental insurance cover. Even a small ATM withdrawal or purchase qualifies.

Update your mobile number: Aadhaar-linked mobile numbers ensure seamless DBT credit and allow you to check balances via the *99# USSD service without internet.

Nominate a family member: Always fill in the nominee column. In case of death, the nominee can claim the balance and the insurance payout without lengthy legal processes.

Upgrade to PMJJBY and PMSBY: The ₹20 + ₹436 annual premium for ₹4 lakh combined coverage is among the best value insurance products available to low-income earners anywhere in the world.

Transition to APY: Once financially stable, link your Jan Dhan account to Atal Pension Yojana for guaranteed pension income post-60. If you are a gig worker or platform employee, also explore [[Link to What Happens If You Stop NPS Contributions?]] to understand how to protect your long-term retirement corpus.

Track dormancy: If no transaction is made for 24 months, the account becomes dormant. Reactivate it by visiting the branch with KYC documents, as DBT transfers may fail into dormant accounts.

Common Mistakes to Avoid

Holding duplicate accounts: Maintaining both a BSBD (Jan Dhan) and a regular savings account at the same bank violates RBI norms and may lead to account freezing.

Ignoring the OD facility: Many eligible holders are unaware of the ₹10,000 OD benefit and turn to moneylenders at exploitative interest rates instead.

Not updating Aadhaar seeding: Unlinked accounts may miss out on DBT credits, particularly LPG subsidies and NREGA payments.

Assuming the account is free forever unconditionally: While there is no minimum balance, charges may apply for additional services beyond the free transaction limits — always verify the bank's fee schedule.

Misunderstanding insurance scope: The RuPay card insurance covers accidental death — not illness, not suicide, not self-inflicted injury. Understand the exact terms before assuming full life insurance protection.

Conclusion: Actionable Takeaways for PMJDY Account Holders

The Pradhan Mantri Jan Dhan Yojana (PMJDY) is far more than a savings account. It is a structured financial inclusion platform that provides zero-balance banking, emergency credit, accidental insurance, and a gateway to India's broader social security architecture — all at minimal or no cost to the account holder.

Here are the key actions every PMJDY account holder or prospective applicant should take:

Open your account today if you or a family member is unbanked — visit the nearest bank branch, IPPB outlet, or BC agent with just an Aadhaar card.

Activate your RuPay card immediately and use it at least once every 45 days to maintain your free ₹2 lakh insurance cover.

Apply for the ₹10,000 overdraft after 6 months of active account use — it is your emergency buffer without pledging any collateral.

Enrol in PMJJBY and PMSBY for an additional ₹4 lakh in combined life and accident coverage at just ₹456/year.

Seed your Aadhaar and mobile number to ensure uninterrupted DBT credit and mobile banking access.

Avoid dormancy — transact at least once every 6 months to keep the account fully active.

For the complete picture of how PMJDY integrates with PMJJBY, PMSBY, APY, NPS, and PM-SYM under India's financial inclusion mission, read our comprehensive guide: [[Link to Government Schemes for Financial Inclusion and Social Security in India 2026: Complete Guide to PMJDY, PMJJBY, PMSBY, APY, PM-SYM & NPS]].

Frequently Asked Questions (FAQs)

1. Can I open a PMJDY account if I already have a savings account at another bank?

Yes. You can open a PMJDY (BSBD) account at a different bank even if you hold a regular savings account elsewhere. However, you cannot hold both a BSBD account and a regular savings account at the same bank simultaneously, as per RBI guidelines. If you open a Jan Dhan account at Bank A, you must not hold a regular savings account at Bank A.

2. What is the current overdraft limit under PMJDY in 2025?

The maximum overdraft limit is ₹10,000 per account, revised upward from the earlier ₹5,000 limit in August 2018. For the first 6 months of account operation, a smaller seed overdraft of up to ₹2,000 may be available without conditions. Eligibility for the full ₹10,000 requires 6 months of satisfactory account activity, age between 18–65, and no history of defaults.

3. What happens if I don't use my RuPay card for more than 45 days?

If your RuPay debit card is not used for at least one transaction in the 45 days prior to an accidental event, the accidental death and disability insurance claim may be rejected. NPCI's insurance partner requires proof of recent card usage to validate claims. Make it a habit to use the card regularly — even a small ATM balance enquiry transaction counts at some banks, but a financial transaction (purchase or withdrawal) is the safest practice.

4. Is the ₹30,000 life insurance cover still available under PMJDY?

The ₹30,000 life insurance cover was a limited benefit available only to those who opened PMJDY accounts between 15 August 2014 and 26 January 2015 and were unbanked at the time. This window is now closed. New account holders do not automatically receive this benefit. Instead, they are encouraged to enrol in PMJJBY (₹2 lakh life cover at ₹436/year) for comprehensive life insurance.

5. Can a minor open a PMJDY account?

Yes. Minors above the age of 10 years can open a PMJDY account independently, but it will be managed by a guardian until the minor attains 18 years of age. For children below 10, a guardian can open the account on their behalf. The overdraft facility is, however, not available to minors — only adults aged 18–65 are eligible.

6. Will DBT payments stop if my PMJDY account becomes dormant?

Yes. If your Jan Dhan account becomes dormant (no transactions for 24 consecutive months), Direct Benefit Transfers (DBT) such as LPG subsidies, NREGA wages, or PM-KISAN instalments may fail to credit. To reactivate a dormant account, visit your home branch with valid KYC documents (Aadhaar, photo ID) and submit a reactivation request. Most banks process this within 1–2 working days. Always keep your account active with at least one transaction every 6 months to avoid dormancy.