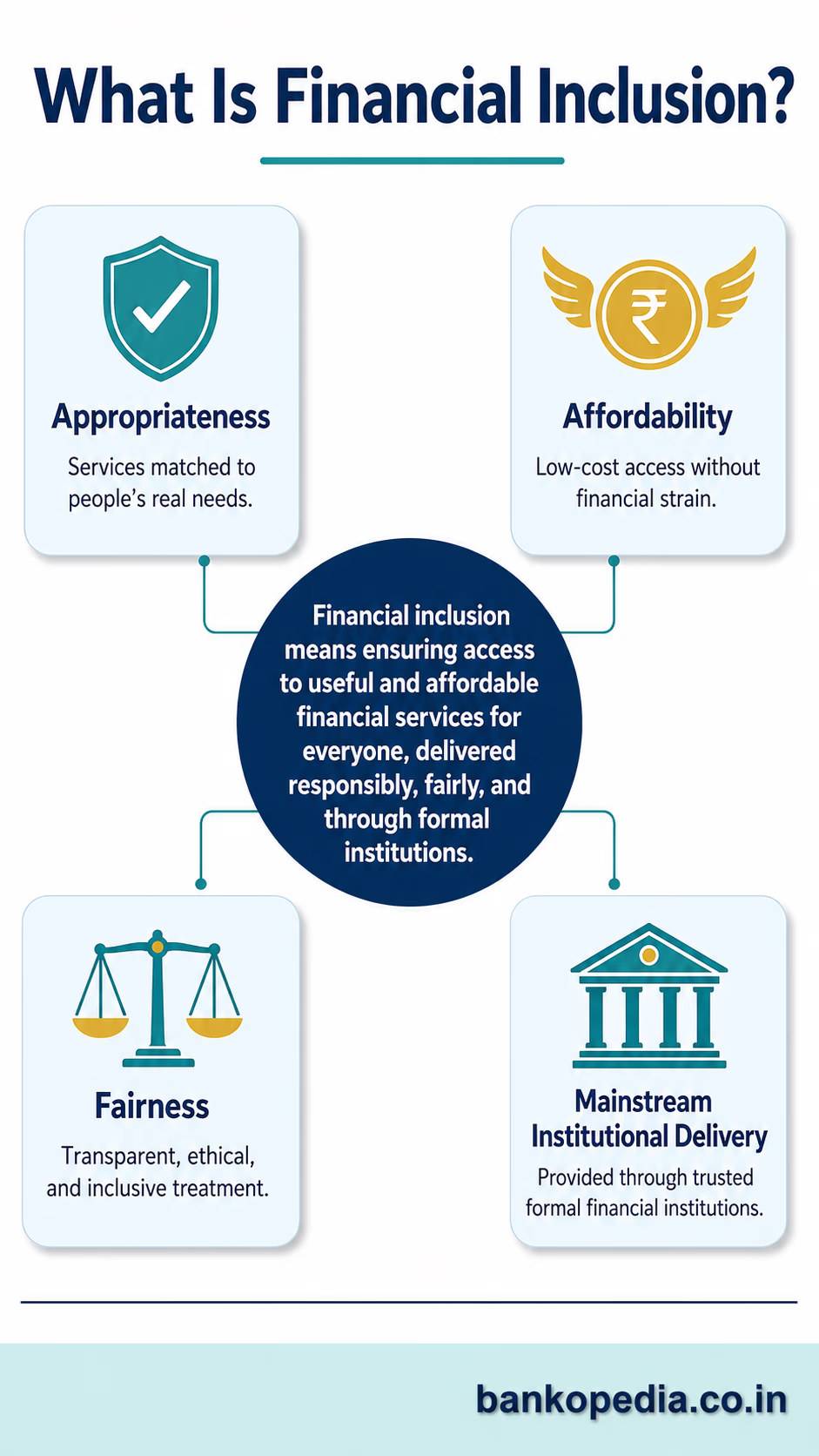

Financial inclusion may be defined as the process of ensuring access to appropriate financial products and services needed by all sections of the society in general and vulnerable groups such as weaker sections and low-income groups in particular, at an affordable cost in a fair and transparent manner by mainstream institutional players." > — Reserve Bank of India (RBI)

This definition is critical for JAIIB/CAIIB candidates because it establishes the foundational pillars of the RBI’s mandate: appropriateness, affordability, fairness, and mainstream institutional delivery. It recognizes that India’s informal economy, which constitutes a massive portion of the workforce, historically relied on usurious moneylenders charging exorbitant interest rates (often exceeding 36–60% per annum). Addressing this requires a systemic response, not ad-hoc interventions.

Evolution and Foundational Committees: The Road to Modern Inclusion

The journey of financial inclusion in India did not begin in the 21st century. It has roots in the nationalization of banks (1969 and 1980) and the introduction of the Lead Bank Scheme (1969). However, the modern, targeted approach to financial inclusion was shaped by key RBI committees.

The Rangarajan Committee (2008) The Committee on Financial Inclusion, chaired by Dr. C. Rangarajan, was instrumental in providing a comprehensive framework for inclusion. It defined financial inclusion formally and highlighted that exclusion was largely concentrated among marginalized groups: marginal farmers, landless laborers, oral lessees, self-employed, unorganized sector enterprises, urban slum dwellers, migrants, and socially backward castes. The committee emphasized the need for a targeted approach, recommending the widespread use of the Business Correspondent (BC) model.

The Nachiket Mor Committee (2014) The Committee on Comprehensive Financial Services for Small Businesses and Low-Income Households, headed by Dr. Nachiket Mor, was a watershed moment. Its recommendations laid the groundwork for the modern differentiated banking system.

Key Mandate: It proposed that every Indian resident should have an electronic bank account.

Differentiated Banks: It recommended the creation of specialized entities—Payment Banks (PBs) and Small Finance Banks (SFBs)—to target specific niches (payments/remittances and micro-credit, respectively) without exposing the systemic banking network to undue risk.

Aadhaar Integration: It strongly advocated for the use of Aadhaar as the primary KYC infrastructure to lower customer acquisition costs.

Regulatory Enablers: KYC Relaxation and the BC Model

Before mass account opening could occur, the RBI had to dismantle structural barriers. The two largest barriers were the cost of servicing rural areas and the stringent Know Your Customer (KYC) norms.

Simplified KYC and e-KYC Historically, documentary proof of identity and address barred millions from banking. The RBI introduced "Small Accounts" where accounts could be opened with a self-attested photograph and signature, subject to limitations (maximum balance of ₹50,000, aggregate credits of ₹1 lakh in a year, and maximum withdrawal of ₹10,000 per month). Furthermore, the introduction of Aadhaar-based e-KYC allowed banks to authenticate customers digitally, dropping the cost of customer acquisition from an estimated ₹1,000 to less than ₹15.

The Business Correspondent (BC) / Business Facilitator (BF) Model Introducated in 2006, the BC/BF model allows banks to provide financial services at locations other than a bank premises/ATM.

Business Facilitators (BFs): Can engage in non-financial services like borrower identification, application processing, and post-sanction monitoring.

Business Correspondents (BCs): Are permitted to conduct cash transactions (deposits and withdrawals) on behalf of the bank.

Scale: Today, the BC network operates through micro-ATMs connected to the bank's Core Banking Solution (CBS), providing critical last-mile connectivity in India's 6.5 lakh villages where brick-and-mortar branches are economically unviable.

The PMJDY Revolution: Features, Phases, and Impact

Launched on 28 August 2014, the Pradhan Mantri Jan Dhan Yojana (PMJDY) is the cornerstone of India’s modern financial inclusion narrative. Conceived as a national mission, PMJDY shifted the paradigm from "village-centric" inclusion to "household-centric" inclusion.

Core Features of PMJDY (Critical Exam Data):

BSBD Accounts: Offers a zero-balance Basic Savings Bank Deposit (BSBD) account.

RuPay Debit Card: Comes with an inbuilt accident insurance cover. Initially set at ₹1 lakh, this was enhanced to ₹2 lakh for new accounts opened after 28 August 2018.

Overdraft (OD) Facility: To provide micro-credit, an OD facility was introduced. Initially ₹5,000, it was doubled to ₹10,000. The upper age limit for availing the OD was also relaxed from 60 to 65 years. Furthermore, ODs up to ₹2,000 are available without any conditions.

Direct Benefit Transfer (DBT): Accounts are linked to Aadhaar to facilitate leak-proof routing of government subsidies.

Quantitative Impact: By mid-to-late 2024, the PMJDY program facilitated the opening of over 53 crore (530 million) accounts, with total deposits crossing ₹2.3 lakh crore.

Approximately 55% of these accounts belong to women.

Over 65% are held in rural and semi-urban areas.

The proportion of zero-balance accounts has plummeted from over 76% in 2014 to under 8% today, signaling a shift toward active usage.

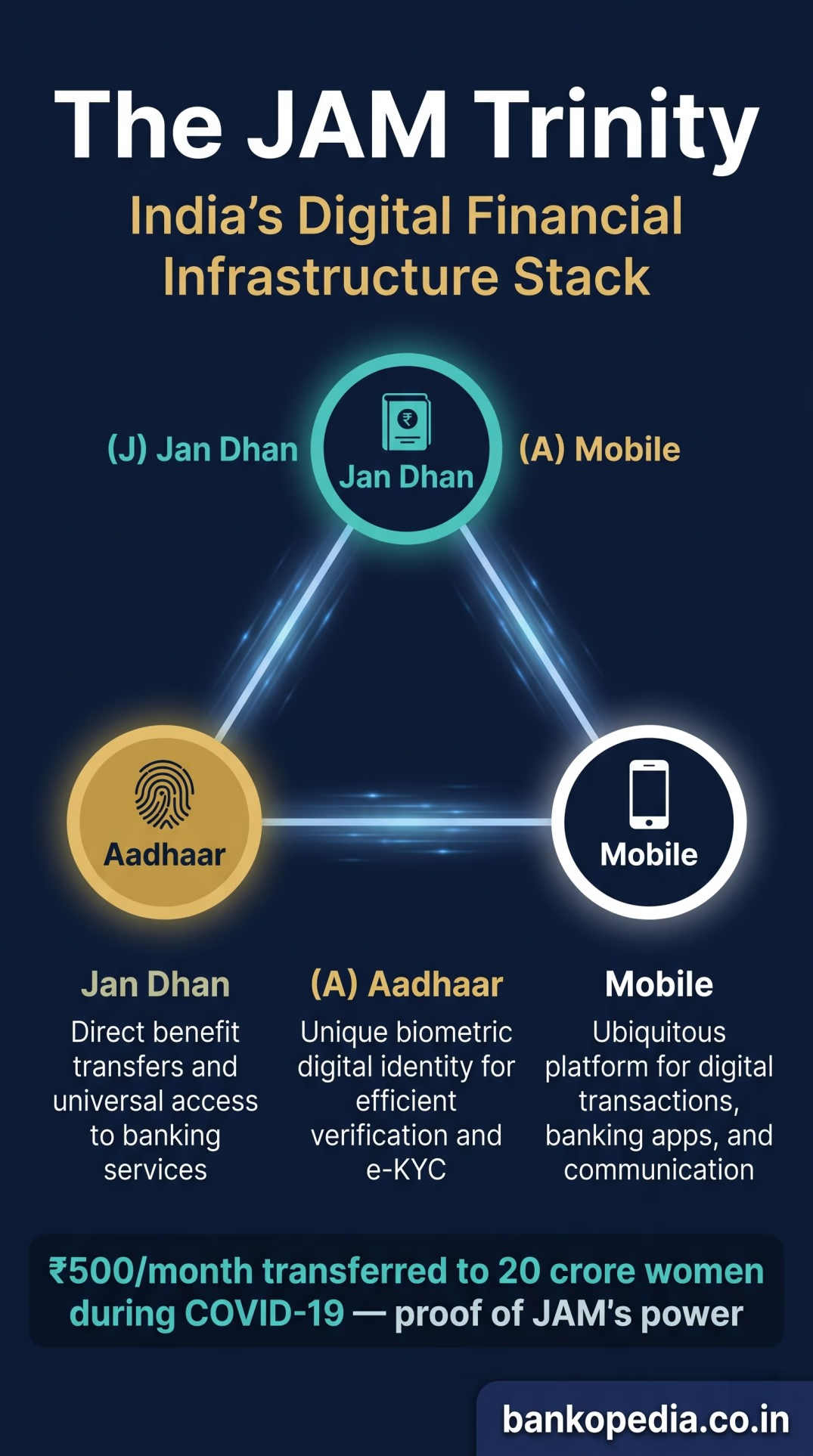

The JAM trinity—Jan Dhan, Aadhaar, and Mobile—has proven to be a formidable infrastructure stack, creating a direct, leak-proof conduit for welfare transfers.

This was visibly demonstrated during the COVID-19 pandemic in 2020, when the government transferred ₹500 per month directly into the accounts of over 20 crore women beneficiaries under the PM Garib Kalyan Yojana.

The Social Security Net: Beyond Basic Banking

True financial inclusion extends beyond savings to risk mitigation. Recognizing this, the government launched three flagship social security schemes in 2015, which are frequently tested in banking examinations.

1. Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) - Life Insurance

Eligibility: Individuals in the age group of 18 to 50 years having a savings bank account.

Coverage: ₹2 lakh in case of death due to any reason.

Premium: ₹436 per annum (auto-debited from the bank account).

Administered via: Life Insurance Corporation of India (LIC) and other willing life insurers.

2. Pradhan Mantri Suraksha Bima Yojana (PMSBY) - Accidental Insurance

Eligibility: Individuals in the age group of 18 to 70 years having a bank account.

Coverage: ₹2 lakh for accidental death or full disability, and ₹1 lakh for partial disability.

Premium: ₹20 per annum.

Administered via: Public Sector General Insurance Companies or other willing general insurers.

3. Atal Pension Yojana (APY) - Pension Scheme

Eligibility: Unorganized sector workers aged 18 to 40 years.

Coverage: Guaranteed minimum monthly pension ranging from ₹1,000 to ₹5,000 after attaining the age of 60 years, depending on the contributions made.

Administered via: Pension Fund Regulatory and Development Authority (PFRDA) through the National Pension System (NPS) architecture.

Institutional Delivery Mechanisms: Differentiated Banks

To deepen inclusion, the RBI operationalized the Nachiket Mor Committee’s vision by issuing guidelines for Differentiated Banks in 2014. These entities operate under the Banking Regulation Act, 1949, but with restricted or targeted mandates.

Payment Banks (PBs) Designed to serve low-income households, small businesses, and migrant labor.

Capital Requirement: Minimum paid-up equity capital of ₹100 crore.

Operations: They can accept demand deposits (current and savings). Crucially, the maximum balance per customer was increased by the RBI in April 2021 from ₹1 lakh to ₹2 lakh to cater to MSMEs and unorganized workers.

Restrictions: They cannot undertake lending activities or issue credit cards. They can issue ATM/debit cards and distribute third-party products (mutual funds, insurance).

Players: India Post Payments Bank (IPPB) relies on the vast network of 1.55 lakh post offices. Airtel Payments Bank leverages telecom distributors. Fino Payments Bank focuses on merchant banking. Paytm Payments Bank faced severe RBI regulatory action in 2024 over compliance, highlighting the rigorous oversight in this sector.

Small Finance Banks (SFBs) Designed to provide basic banking activities of acceptance of deposits and lending to unserved and underserved sections.

Capital Requirement: Minimum paid-up voting equity capital of ₹200 crore (increased from the initial ₹100 crore).

Lending Mandate: At least 75% of their Adjusted Net Bank Credit (ANBC) must go to Priority Sector Lending (PSL).

Portfolio Requirement: At least 50% of their loan portfolio must constitute loans and advances of up to ₹25 lakh.

The Role of NABARD and Microfinance Models

The National Bank for Agriculture and Rural Development (NABARD) is the apex development finance institution critical to rural financial inclusion.

SHG-Bank Linkage Programme (SHG-BLP) Launched in 1992, this is the largest microfinance program in the world. It organizes rural poor, primarily women, into Self-Help Groups (SHGs) of 10-20 members. These groups pool their savings, lend internally, and are eventually linked to banks for collateral-free loans. This model substitutes physical collateral with social capital and peer pressure.

Joint Liability Groups (JLGs) Introduced for tenant farmers, oral lessees, and sharecroppers who lack land titles and therefore cannot access formal agricultural credit. A JLG is an informal group of 4-10 individuals who come together for the purpose of availing bank loans either individually or through the group mechanism against a mutual guarantee.

Financial Inclusion Fund (FIF) Managed by NABARD, the FIF was created by merging the Financial Inclusion Fund and the Financial Inclusion Technology Fund. It is utilized to support developmental and promotional interventions, such as funding Financial Literacy Centres (FLCs), supporting the rollout of micro-ATMs, and implementing the e-Shakti project (the digitization of SHG records to facilitate faster bank credit).

Digital Public Infrastructure (DPI): The Fintech Multiplier

The broader fintech ecosystem has dramatically expanded the toolkit for reaching underserved Indians, moving beyond physical infrastructure to digital rails.

Unified Payments Interface (UPI) Developed by the National Payments Corporation of India (NPCI), UPI is the backbone of India's digital payments. By the end of 2024, UPI breached the monumental 15 billion transactions per month mark. It has democratized digital payments for tier-3 cities, small merchants, and street vendors.

Aadhaar Enabled Payment System (AePS) AePS allows online interoperable financial transactions at Micro-ATMs through the BC of any bank using Aadhaar authentication. This has been revolutionary for illiterate or tech-averse populations who can now withdraw cash using only their fingerprint.

Account Aggregator (AA) Framework An RBI-regulated framework that enables individuals to securely share their financial data—with explicit consent—across institutions. For financial inclusion, this is a game-changer. It allows lenders to assess the creditworthiness of "thin-file" borrowers (like street vendors or small farmers) who lack conventional credit histories but have digital footprints (like GST filings, UPI transactions, or savings patterns).

Measuring Progress: The RBI Financial Inclusion Index (FI-Index)

To empirically track the progress of these massive initiatives, the RBI constructed the Financial Inclusion Index (FI-Index), first published in August 2021. For banking professionals, the methodology of this index is essential knowledge.

Key Features of the FI-Index:

No Base Year: The index does not have a base year; it captures the cumulative efforts of all stakeholders over the years.

Scale: It is a single-value index ranging from 0 (complete exclusion) to 100 (full inclusion).

Publication: It is published annually in July for the financial year ending in March.

The Three Parameters:

Access (Weight: 35%): Measures the availability of physical and digital infrastructure. Metrics include the number of bank branches, ATMs, BCs, and digital access points per lakh population.

Usage (Weight: 45%): Captures the extent of active utilization. It looks at the volume and value of deposits, credit, insurance, and pension products. It is the most heavily weighted, emphasizing that having a bank account is not enough; using it matters more.

Quality (Weight: 20%): Reflects the qualitative aspects, including financial literacy, consumer protection, grievance redressal, and the relevance of the products offered.

The Trajectory: India's FI-Index has shown robust, consistent improvement.

FY 2021: 53.9

FY 2022: 56.4

FY 2023: 60.1

FY 2024: 64.2

The leap to 64.2 in FY2024 was driven largely by significant improvements in the "Usage" parameter, proving that behavioral adoption of financial services is successfully catching up to infrastructure deployment.

Priority Sector Lending (PSL) and Financial Literacy

The RBI enforces financial inclusion structurally through Priority Sector Lending (PSL) norms. Commercial banks are mandated to direct a specific percentage of their Adjusted Net Bank Credit (ANBC) to underserved sectors.

Key PSL Targets (for Domestic Commercial Banks):

Total PSL Target: 40% of ANBC.

Agriculture: 18% of ANBC.

Small and Marginal Farmers (SMFs): Phased increase to 10% by FY 2024.

Weaker Sections: Phased increase to 12% by FY 2024.

Micro Enterprises: 7.5% of ANBC.

These mandates force commercial banks to innovate and reach demographics they might otherwise ignore due to perceived credit risks.

Financial Literacy Initiatives As the FI-Index notes, quality matters. The RBI has established a network of Financial Literacy Centres (FLCs) at the block level and Centres for Financial Literacy (CFLs). The National Strategy for Financial Inclusion (NSFI 2019-2024) laid down specific milestones, including providing banking access to every village within a 5 km radius or a hamlet of 500 households in hilly areas.

Persistent Gaps and the Financial Inclusion 2.0 Roadmap

Despite unprecedented successes, structural limitations persist. The next phase—Financial Inclusion 2.0—must pivot from "access" to "meaningful usage."

1. The Credit Access Deficit: While deposit mobilization (savings) and payments (UPI) have been solved at scale, formal credit remains elusive for the bottom of the pyramid. The PMJDY overdraft facility sees limited uptake because banks remain risk-averse regarding borrowers with no CIBIL scores. The unbanked are now "banked," but they are still largely "under-credit-served."

2. The Double-Edged Sword of AI and Fintech: Fintechs are increasingly using AI and machine learning for underwriting and collections. While this extends credit efficiently, poorly calibrated algorithms risk reinforcing existing biases. The historical IndusInd Bank (Bharat Financial Inclusion Ltd) episode, where aggressive microfinance recovery practices came under severe regulatory scrutiny, serves as a stark reminder. Aggressive collections can push vulnerable, newly-banked populations into debt traps.

3. Consumer Protection: New-to-banking customers are highly vulnerable to mis-selling (e.g., being forced to buy insurance to get a loan) and cyber frauds. The RBI’s Integrated Ombudsman Scheme (2021) is a critical step in providing a unified, cost-free grievance redressal mechanism, but financial literacy remains the best defense.

Conclusion: Moving from Access to Meaningful Usage

India’s financial inclusion journey over the past decade is one of the most ambitious and successful experiments in global development finance. From a country where barely 35% of adults had bank accounts in 2011, India has moved to near-universal account ownership.

Having an account is a necessary but not sufficient condition for financial inclusion. What matters is meaningful, regular, and self-directed usage—savings habits, credit access, insurance adoption—and on those metrics, the journey is still very much in progress.

For banking professionals navigating this landscape, the mandate is clear. The physical and digital infrastructure—the branches, the BCs, UPI, and Account Aggregators—has been built. The defining question of the next decade is whether banks and fintechs can design products that genuinely serve the needs of the rural and low-income demographics, assess their credit risk fairly using digital trails, and earn their sustained trust.

Financial inclusion is no longer a CSR initiative; driven by RBI mandates and technological enablement, it is the core growth engine for India's banking sector as the nation marches toward its goal of becoming a developed economy by 2047.