Personal Loan Eligibility in India: A Complete Guide to Requirements and Criteria

Unsecured personal loan eligibility criteria in India have undergone a meaningful transformation over the past two years. After a period of aggressive, volume-driven lending that drew regulatory scrutiny from the Reserve Bank of India (RBI), lenders — ranging from large public sector banks to private sector players and non-banking financial companies (NBFCs) — have recalibrated their underwriting frameworks. The resurgence of unsecured personal loans is now being driven not by indiscriminate growth targets, but by a sharper focus on borrower quality and asset health. For any individual planning to apply for a personal loan, understanding how lenders evaluate an application is no longer optional; it is essential to securing competitive terms, avoiding rejection, and maintaining a healthy credit footprint.

What Are the Basic Eligibility Criteria for Personal Loans?

Every lender maintains a base-level eligibility matrix that serves as the first filter in the loan approval process. While specific parameters vary across institutions, the following criteria are broadly standardized across the Indian personal loan market:

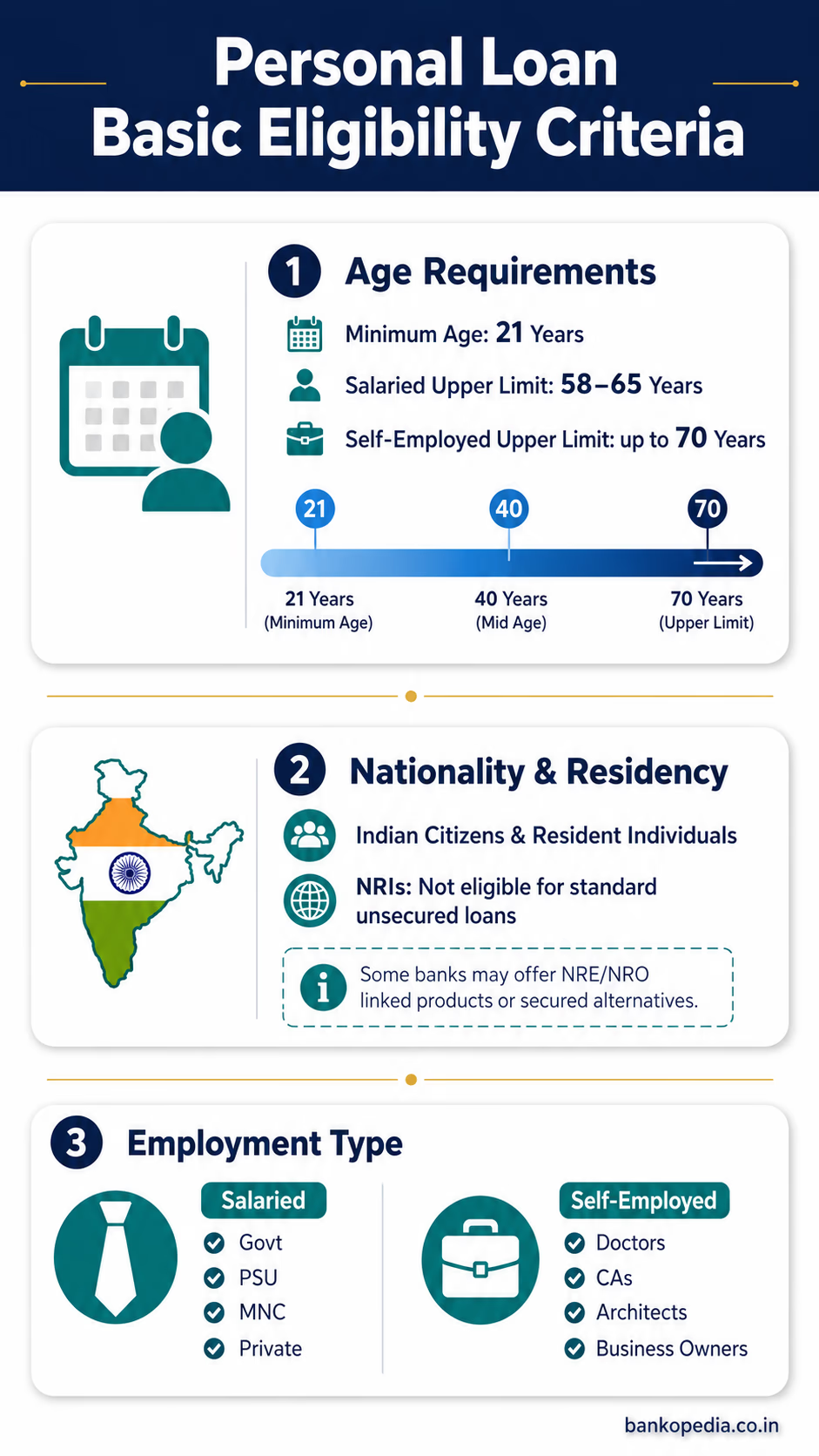

Age Requirements

Most banks and NBFCs require applicants to be at least 21 years of age at the time of application. The upper age limit typically ranges from 58 to 65 years for salaried individuals and may extend to 70 years for self-employed professionals. The logic is straightforward: the loan tenure must end before or at the time of expected income cessation.

Nationality and Residency

Personal loans in the standard domestic category are available to Indian citizens and resident individuals. Non-Resident Indians (NRIs) are generally not eligible for standard unsecured personal loans, though they may access credit through NRE or NRO account-linked products. It is worth noting that Small Finance Banks (SFBs) are currently aggressively competing for NRI deposits through FCNR-B rates, a segment that remains distinct from retail lending to residents.

Employment Type

Lenders broadly classify borrowers into two categories:

Salaried employees: Those employed with central or state government bodies, public sector undertakings (PSUs), MNCs, or reputed private companies. Many banks maintain a list of approved employers, and working for a company on that list can materially improve loan eligibility.

Self-employed individuals and professionals: Includes doctors, chartered accountants, architects, and business owners. This segment faces more rigorous documentation scrutiny due to variable income streams.

Minimum Income Thresholds

Income eligibility benchmarks differ by geography. In metropolitan cities such as Mumbai, Delhi, Bengaluru, and Chennai, the minimum net monthly income requirement is typically ₹25,000 to ₹30,000 for salaried borrowers. In Tier 2 and Tier 3 cities, this threshold may be lower, often around ₹15,000 to ₹20,000. For self-employed borrowers, lenders look at annual net profit — usually a minimum of ₹2 to ₹3 lakh per annum — as evidenced by Income Tax Returns (ITRs).

Minimum Work Experience

Salaried applicants are typically required to have a minimum of one to two years of total work experience, with at least six months in the current organization. Self-employed individuals usually need to demonstrate two to three years of business continuity in the same profession or trade.

How Banks Assess Credit Profile and CIBIL Score

In the current lending environment, the credit bureau report has become the single most influential document in personal loan underwriting. The CIBIL Score — generated by TransUnion CIBIL, one of four RBI-licensed credit information companies in India — is a three-digit number ranging from 300 to 900. A score of 750 and above is widely regarded as the threshold for accessing the best personal loan interest rates and higher loan amounts.

What Constitutes a Good Credit Profile?

Lenders do not merely look at the score in isolation. The full CIBIL report is parsed for multiple qualitative signals:

Repayment history: Any default, settlement, or consistent delay on past or existing loans and credit cards is treated as a serious negative signal. A "written-off" account can disqualify a borrower entirely.

Credit utilization ratio: For borrowers with credit cards, lenders examine what percentage of the sanctioned credit limit is being used. A utilization above 30–35% on revolving credit is viewed unfavorably.

Credit vintage: How long an individual has held credit accounts matters. A longer credit history with consistent repayment behavior significantly strengthens the profile.

Enquiry density: Multiple hard enquiries — generated each time a borrower applies for a new loan — within a short period signal credit hunger. This is a red flag that lenders take seriously.

Credit mix: A balanced mix of secured loans (home loan, vehicle loan) and unsecured credit (credit card, personal loan) is viewed positively.

The Role of CRIF High Mark, Equifax, and Experian

While CIBIL remains the dominant bureau, lenders increasingly pull reports from multiple bureaus — CRIF High Mark, Equifax India, and Experian India — to get a more complete picture. Discrepancies between bureau reports can sometimes flag identity issues or unreported liabilities, both of which can delay or derail an application.

"Unsecured personal loans are making a strong comeback, but lenders are no longer chasing volume. The focus has decisively shifted to borrower profile integrity and asset quality — a structural correction that the RBI's risk-weight revision for consumer credit catalyzed in late 2023."

RBI's Role in Shaping Lending Standards

In November 2023, the RBI increased risk weights on consumer credit from 100% to 125%, making it more capital-intensive for banks and NBFCs to disburse unsecured loans indiscriminately. This regulatory intervention directly tightened underwriting standards across the sector and is a primary reason why lenders today apply more granular scrutiny to credit profiles before sanctioning personal loans.

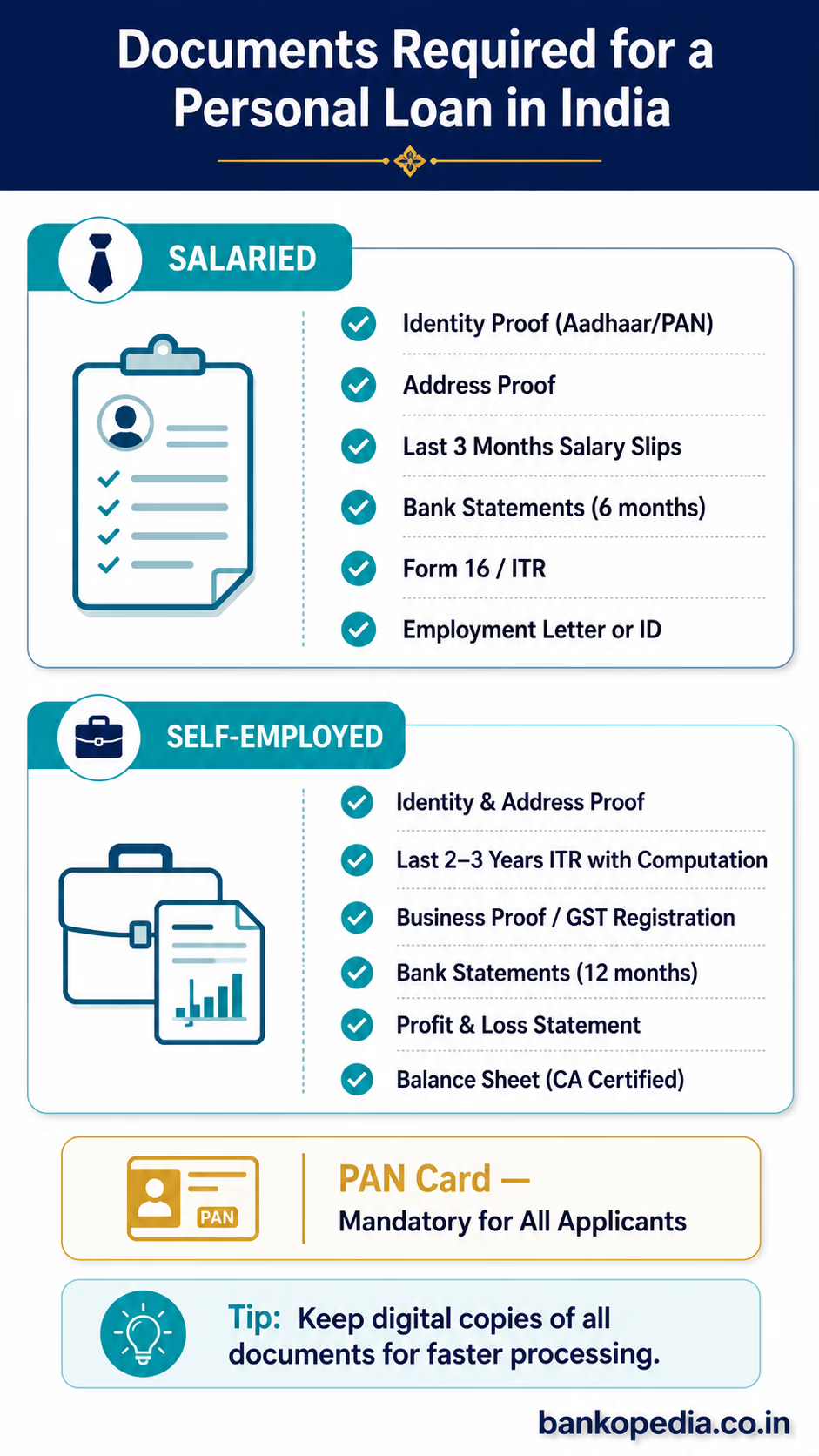

Income Documentation and Employment Verification Requirements

Documentary evidence of income is the backbone of personal loan underwriting. The nature and volume of documentation required depends on whether the applicant is salaried or self-employed.

For Salaried Individuals

Salary slips: The most recent two to three months' salary slips are mandatory. Lenders scrutinize components such as basic pay, house rent allowance (HRA), and deductions to calculate net take-home income.

Bank statements: Six months of bank statements from the salary account are typically required. Lenders look for regular salary credits, the absence of cheque bounces, and overall transactional behavior.

Form 16: Issued by the employer, Form 16 confirms tax deducted at source and is treated as corroborating evidence of declared income.

Employment letter or ID: Some lenders request a current employment verification letter, particularly for applicants working with lesser-known private companies.

For Self-Employed Individuals

Income Tax Returns (ITRs): The last two to three years' ITRs, along with computation of income, are essential. Lenders are wary of ITRs filed belatedly or with significant year-on-year income variation without explanation.

Profit and Loss account and Balance Sheet: Audited financials for at least the past two years are required from proprietors, partners, and company directors.

GST registration and returns: Increasingly, lenders use GST return data (GSTR-1 and GSTR-3B) as a proxy for business turnover validation. This has become especially relevant as the government works on operationalizing GST refund mechanisms, which has increased the system's data reliability.

Business vintage proof: Shop and Establishment certificate, trade license, or professional degree certificate (for doctors, CAs, etc.) as applicable.

Digital and AI-Driven Verification

An important development reshaping income verification is the use of Account Aggregator (AA) framework, operationalized under RBI's regulatory sandbox, which allows lenders to access a borrower's financial data across institutions in a consent-driven manner. This reduces documentation burden while improving verification accuracy. Simultaneously, AI-powered fraud detection tools are being deployed to counter sophisticated document manipulation — a critical safeguard given that AI has made forgery more accessible, requiring lenders to commensurately upgrade their defenses.

Asset Quality Checks: What Lenders Look For

The renewed lender focus on asset quality is arguably the most significant shift in personal loan underwriting in recent years. While personal loans are by definition unsecured — meaning no collateral is pledged — lenders conduct a range of checks to assess the systemic risk of extending credit to a given borrower profile.

Existing Loan Obligations and FOIR

The Fixed Obligation to Income Ratio (FOIR) — also referred to as Debt-to-Income (DTI) ratio — is a critical underwriting metric. It measures what percentage of a borrower's net monthly income is already committed to existing EMI obligations. Most lenders in India cap FOIR at 40% to 50%. A borrower with a net monthly income of ₹60,000 and existing EMIs of ₹25,000 would have a FOIR of approximately 41.7%, leaving limited headroom for additional credit.

Overdue and Default History

Lenders pull Days Past Due (DPD) data from bureau reports. Even a single instance of 30+ DPD within the past 12 months can significantly impair a borrower's eligibility. Accounts flagged as "Doubtful" or "Loss" in the credit report — terms aligned with the RBI's Income Recognition and Asset Classification (IRAC) norms — result in near-automatic rejection.

Loan Stacking

A growing concern for lenders in the unsecured segment is loan stacking — the practice of simultaneously applying for and receiving multiple small loans from different lenders within a short window before credit bureaus update records. Enhanced bureau reporting frequencies and the AA framework are two mechanisms being used to combat this behavior, which had contributed to the earlier deterioration in personal loan asset quality.

Industry and Employer Risk

Beyond individual financials, lenders assess the health of the sector the borrower works in. Employees in industries classified as cyclically vulnerable or under regulatory stress may face additional scrutiny. Banks maintain negative lists of employer sectors during periods of macroeconomic stress, adjusting these lists dynamically.

Improving Your Profile: Tips to Qualify for Better Loan Terms

Eligibility is not a static binary outcome. Borrowers have meaningful agency in strengthening their profile over time. The following are actionable, evidence-based steps:

1. Build and Monitor Your Credit Score Proactively

Register for free credit monitoring through TransUnion CIBIL's consumer portal or through the RBI's mandate that all credit bureaus provide one free report annually. Dispute any inaccurate or stale entries — particularly settled or closed accounts that continue to appear as "active." Even a 20–30 point improvement in CIBIL score can shift you from one interest rate band to a significantly cheaper one.

2. Reduce Existing Debt Before Applying

If your FOIR is close to or above the 40–50% ceiling, consider prepaying smaller loans or closing high-utilization credit card balances before submitting a fresh personal loan application. This mechanically improves your debt serviceability metrics and signals financial discipline to the lender.

3. Avoid Multiple Simultaneous Applications

Each loan application triggers a hard enquiry on your credit report. Multiple hard enquiries within a 30–60 day window will depress your score and signal desperation for credit. Use the RBI's Financial Literacy initiative resources or bank pre-eligibility check tools — which use soft enquiries — to assess your chances before formally applying.

4. Maintain Salary Account Consistency

Lenders place significant weight on the regularity and cleanliness of bank statements. Avoid large unexplained cash withdrawals, maintain average monthly balances, and ensure there are no cheque returns or NACH mandates bouncing in your salary account in the months preceding your application.

5. Leverage Your Existing Banking Relationship

Borrowers who apply for personal loans from banks where they hold existing accounts — savings accounts, fixed deposits, or even previously repaid loans — often benefit from pre-approved offers at preferential rates. Banks price relationship value into their offers, and pre-approved loans may require minimal documentation.

6. For Self-Employed: File ITRs Timely and Accurately

The single most damaging mistake self-employed borrowers make is under-reporting income to minimize tax, only to find that declared income is insufficient to qualify for the desired loan amount. The long-term trade-off — higher loan eligibility, lower interest cost — almost always favors accurate and timely ITR filing.

Conclusion: Navigating the New Underwriting Reality

The personal loan landscape in India in 2024–25 is characterized by a healthy tension between lender appetite for retail credit growth and regulatory imperatives for systemic prudence. The RBI's risk-weight revision, the AA framework's maturation, AI-enhanced fraud detection, and bureau data quality improvements have collectively raised the bar for what constitutes a creditworthy borrower profile.

For borrowers, this is ultimately a positive development. A market that rewards genuine creditworthiness with better pricing is fairer and more sustainable than one that distributes credit indiscriminately. Understanding the unsecured personal loan eligibility criteria in India — from CIBIL score thresholds and FOIR limits to income documentation standards and asset quality checks — positions you not just to qualify for a loan, but to access it on the best possible terms.

Whether you are a salaried professional planning a major expense, or a self-employed individual seeking to manage cash flow, the fundamentals remain unchanged: a clean credit history, documented and stable income, and a reasonable existing debt load are the three pillars on which successful personal loan applications are built. The institutions and tools may evolve, but these principles are durable.