Alternative Investment Funds (AIFs) in India: A Comprehensive SEBI Guide

In an evolving financial landscape where traditional investment vehicles are no longer sufficient for sophisticated investors seeking differentiated returns, alternative investment funds AIFs India SEBI has emerged as one of the most consequential areas of modern portfolio management. Alternative Investment Funds represent a structured, regulated universe of privately pooled investment vehicles that channel capital into asset classes beyond conventional equities, bonds, and mutual funds. From venture capital backing India's next generation of technology startups to infrastructure debt funds supporting Viksit Bharat's development ambitions, AIFs have quietly become an indispensable engine of productive capital formation. With SEBI continuously refining its regulatory architecture — most recently through the GARUDA initiative — understanding the mechanics, categories, and compliance requirements of AIFs is essential for any banking professional, wealth manager, or institutional investor operating in India today.

What are Alternative Investment Funds (AIFs)?

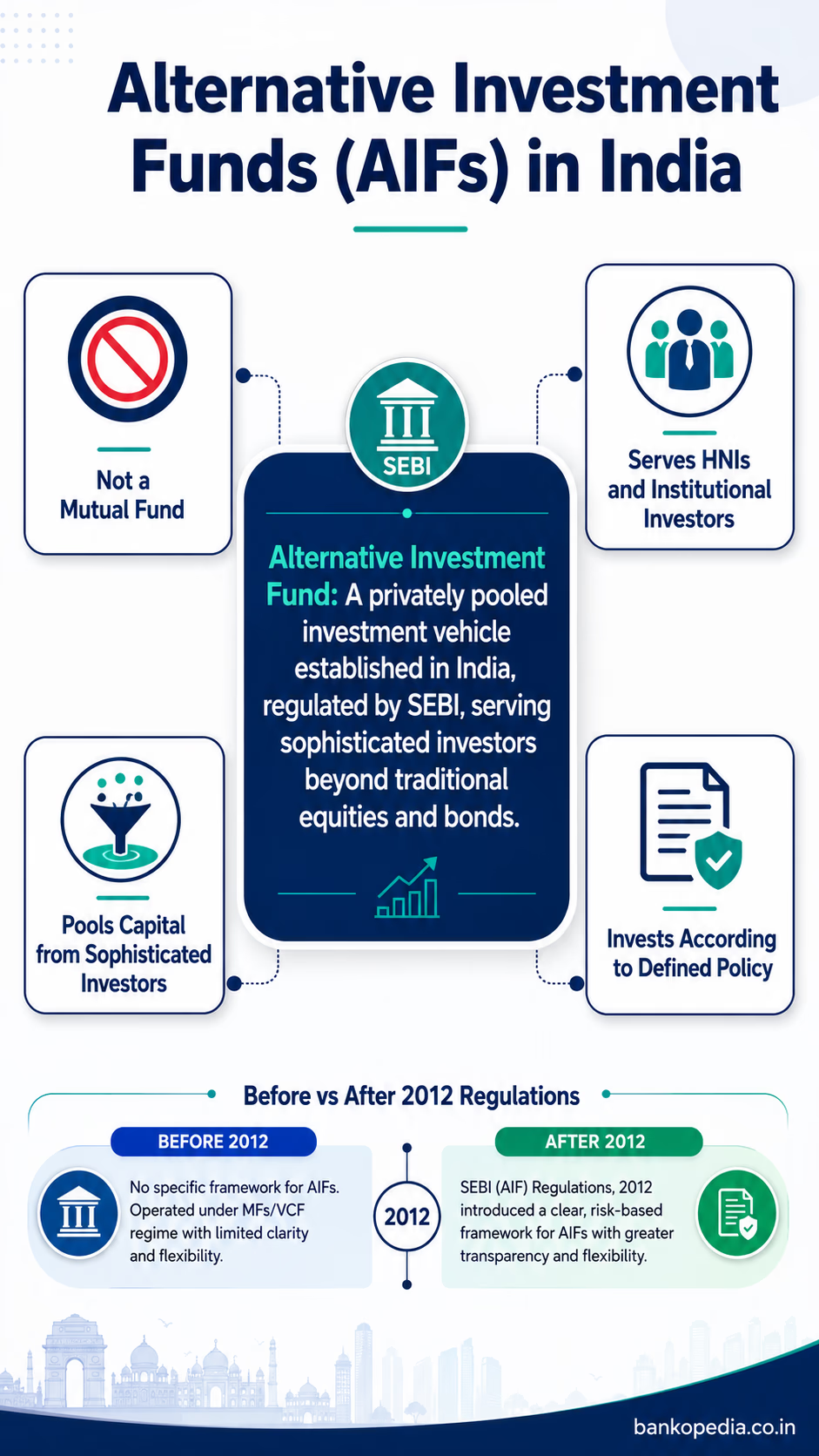

An Alternative Investment Fund, as defined under the SEBI (Alternative Investment Funds) Regulations, 2012, is any fund established or incorporated in India in the form of a trust, a company, a limited liability partnership (LLP), or a body corporate that pools investments from sophisticated investors — whether Indian or foreign — for investing in accordance with a defined investment policy for the benefit of its investors.

The key distinction of an AIF lies in what it is not: it is not a mutual fund, it is not a collective investment scheme regulated under the CIS Regulations, and it is not any other fund regulated by a financial sector regulator in India such as RBI, IRDAI, PFRDA, or NHB. AIFs operate outside mainstream retail investment channels and are designed to serve high-net-worth individuals (HNIs), family offices, institutional investors, and sophisticated corporate bodies willing to accept higher illiquidity and complexity in exchange for potentially superior risk-adjusted returns.

The AIF ecosystem in India has grown dramatically over the past decade. According to SEBI data released in early 2026, the total commitments raised by AIFs have surged past ₹16.9 lakh crore, reflecting the growing appetite for private markets among India's investor community. This growth is not merely numerical — it signals a structural maturation of India's capital markets, where patient capital is increasingly finding its way into sectors that conventional banking credit and public market instruments have historically underserved.

SEBI's Regulatory Framework for Alternative Investment Funds AIFs: Categories and Requirements

SEBI introduced the AIF Regulations in 2012 to consolidate and bring clarity to a fragmented landscape of private pools that operated with minimal oversight. Before 2012, venture capital funds were regulated under a separate 1996 framework, while hedge funds and private equity vehicles operated in a regulatory grey zone. The 2012 regulations created a unified, three-category framework that has since undergone numerous amendments to address emerging market realities.

The regulatory framework mandates the following foundational requirements for all AIFs:

Registration with SEBI: No entity can launch or operate an AIF in India without a valid SEBI certificate of registration.

Corpus and Investment Restrictions: Each scheme under an AIF must have a minimum corpus of ₹20 crore. Angel Funds, following SEBI's sweeping September 2025 amendments, no longer have a minimum corpus requirement.

Investor Limits: An AIF scheme cannot have more than 1,000 investors (200 for angel funds), preserving the private and sophisticated character of these pools.

Tenure: Category I and II AIFs are close-ended funds with a minimum tenure of three years. Category III AIFs may be open-ended or close-ended.

Disclosure Obligations: AIFs must submit periodic reports to SEBI, including details on investments, performance benchmarking, and compliance with placement memorandum commitments.

Leverage Restrictions: Category I and II AIFs cannot borrow funds or engage in leverage except for meeting temporary shortfalls, whereas Category III AIFs are permitted to use leverage subject to SEBI-prescribed limits.

SEBI also mandates that the manager or sponsor of an AIF must maintain a continuing interest in the fund to ensure alignment with investors and reduce moral hazard. The requirement differs by category: for Category I and II AIFs, the minimum continuing interest is 2.5% of the corpus or ₹5 crore, whichever is lower. For Category III AIFs, the requirement is higher at 5% of the corpus or ₹10 crore, whichever is lower. For Angel Funds, following the September 2025 amendments, the sponsor commitment has been restructured to the investment level — a minimum of 0.5% of the investment amount or ₹50,000, whichever is higher — per investment made by the fund.

Types of AIFs: Category I, II, and III Explained

Category I AIFs

Category I AIFs invest in sectors that the government or regulators consider economically or socially desirable. These include:

Venture Capital Funds (VCFs): Focus on early-stage startups and unlisted companies with high growth potential. Given Prime Minister Modi's emphasis on MSMEs as the "nursery of entrepreneurship" — a sentiment echoed by RBI Governor Sanjay Malhotra — VCFs channelling capital into MSME and startup ecosystems are particularly relevant to India's Viksit Bharat vision.

Angel Funds: A sub-category of VCFs that raise capital from angel investors and invest in early-stage ventures. Following SEBI's 2025 amendments, Angel Funds no longer carry a minimum corpus requirement, making them more accessible as a structured early-stage investment vehicle.

SME Funds: Focused specifically on small and medium enterprises that are listed or proposed to be listed on SME exchanges.

Social Venture Funds: Invest in enterprises with social objectives, including microfinance, affordable housing, and rural development initiatives — areas where NABARD's mandate often intersects.

Infrastructure Funds: Channel capital into infrastructure projects including roads, ports, power, and urban development.

Category I AIFs often receive tax concessions and regulatory incentives, making them a preferred structure for government-aligned capital deployment.

Category II AIFs

Category II AIFs are the most heterogeneous category, covering all funds that do not fall under Category I or III and do not employ leverage or borrowing for investment purposes beyond meeting day-to-day operational needs. Common sub-types include:

Private Equity Funds: The dominant form, investing in unlisted companies at growth or buyout stages.

Debt Funds: Provide structured debt capital to companies, often filling the gap left by conservative banking credit policies, particularly for mid-market businesses.

Real Estate Funds: Distinct from REITs, these funds invest directly in real estate projects or real estate companies in unlisted form.

Fund of Funds: Invest in other AIFs, providing a layer of diversification for investors.

Category II AIFs do not receive specific tax or government incentives beyond what is available to any domestic investment vehicle, but they offer significant flexibility in investment mandates.

Category III AIFs

Category III AIFs are the most sophisticated and complex, employing diverse and complex trading strategies with the explicit use of leverage. These include:

Hedge Funds: Use long-short equity, arbitrage, and derivatives strategies across listed and unlisted securities.

PIPE Funds: Invest in listed companies through private placements.

Category III AIFs are subject to stricter SEBI oversight given their leverage and complexity. They must comply with investment concentration limits and enhanced reporting norms, and their managers must demonstrate relevant experience in complex strategies.

Minimum Investment and Eligibility Criteria for AIFs

AIFs are not designed for retail participation. SEBI has deliberately set high entry thresholds to ensure that only sophisticated investors — those capable of evaluating risks without regulatory hand-holding — participate in these vehicles.

The minimum investment requirements are as follows:

Standard AIF investors: A minimum commitment of ₹1 crore per investor per scheme.

Angel fund investors: A minimum investment of ₹25 lakh per scheme, subject to the investor qualifying as an accredited investor or meeting prescribed net worth criteria.

Directors, employees, and fund managers: A concessional minimum of ₹25 lakh, recognising their deeper understanding of the fund's risks.

Eligible investors include resident and non-resident Indians, family trusts, corporates, and foreign portfolio investors (FPIs) meeting SEBI's prescribed conditions. SEBI also introduced the concept of Accredited Investors through a 2021 circular, allowing those with net worth above ₹7.5 crore or annual income above ₹2 crore to access customised AIF structures with relaxed norms, further deepening the sophistication of the investor base.

"The growth of AIFs as a proportion of India's total investment ecosystem signals a profound shift — from a savings-dominated culture to one that increasingly embraces structured risk-taking in pursuit of long-term wealth creation."

AIFs vs. Mutual Funds: Key Differences and Tax Treatment

For banking professionals and wealth advisors, understanding the distinction between AIFs and mutual funds is critical to appropriate client suitability analysis.

Structural and Operational Differences

Regulation: Mutual funds are governed by SEBI (Mutual Funds) Regulations, 1996, with a strong retail investor protection mandate. AIFs operate under the 2012 AIF Regulations, designed for sophisticated investors.

Minimum Investment: Mutual funds have no mandatory minimum (SIPs can start at ₹100). AIFs require a minimum of ₹1 crore.

Liquidity: Open-ended mutual funds offer daily liquidity. Most AIFs are illiquid with lock-in periods of 3–10 years.

Transparency: Mutual funds disclose portfolios monthly. AIF disclosures are periodic and not always publicly available.

Investment Universe: Mutual funds are largely restricted to listed securities. AIFs can invest in unlisted companies, real assets, and complex derivatives.

Tax Treatment

Tax treatment varies significantly by AIF category:

Category I and II AIFs: Enjoy pass-through tax status under Section 115UB of the Income Tax Act. Income and losses at the fund level are deemed to arise in the hands of investors in the same proportion as their investment, and taxed as if the investor had made the investment directly. This avoids double taxation.

Category III AIFs: Do not enjoy pass-through status. The fund itself is taxed — at the Maximum Marginal Rate (MMR) for income other than capital gains, and applicable capital gains rates for securities transactions. This creates a tax efficiency disadvantage relative to Category I and II.

Business trusts vs. AIF structures: Certain infrastructure AIFs structured as Category I funds may intersect with InvIT-like structures, requiring careful analysis of applicable SEBI and income tax provisions.

SEBI's GARUDA Initiative and Recent AIF Reforms

SEBI has been particularly proactive in modernising its AIF oversight framework. The most significant recent initiative is GARUDA — Green-Channel: AIF Rollout Upon Document Acknowledgement. Introduced as a landmark 2026 reform, GARUDA is designed to fast-track AIF scheme approvals and dramatically reduce fund launch timelines. Under GARUDA, regular AIF schemes can be approved and launched within 10 working days — down from the previous 30-day window — while schemes open exclusively to accredited investors are eligible for immediate launch, bypassing the mandatory merchant banker due diligence requirement entirely. GARUDA is fundamentally a launch facilitation mechanism, streamlining the path from scheme registration to capital deployment.

Key features and objectives of GARUDA include:

Accelerated Scheme Approvals: Regular AIF schemes benefit from a compressed 10-working-day approval timeline, reducing the administrative burden on fund managers and enabling faster capital deployment.

Immediate Launch for Accredited-Investor Schemes: AIFs targeting exclusively accredited investors can launch immediately upon document acknowledgement, recognising the higher sophistication of this investor class.

Elimination of Merchant Banker Mandate: For qualifying accredited-investor-only schemes, the requirement for merchant banker due diligence is removed, reducing costs and procedural friction.

Streamlined Regulatory Process: By standardising the document acknowledgement and review process, GARUDA creates a more predictable and efficient regulatory pathway for AIF managers.

Beyond GARUDA, SEBI has implemented several other significant reforms in recent years:

Valuation Norms (2023): SEBI mandated that AIFs appoint independent valuers for computing Net Asset Values, reducing the risk of inflated self-reported valuations — a persistent concern in private markets globally.

Restrictions on Evergreening: Following RBI's concern about AIFs being used to evergreen Non-Performing Assets (NPAs) — where banks invest in AIFs that then lend to stressed bank borrowers, effectively extending repayment timelines artificially — SEBI and RBI jointly issued guidelines restricting regulated entities from investing in AIFs that have downstream investments in the regulated entity's borrowers.

Dematerialisation of AIF Units: SEBI mandated that AIF units be held in demat form, improving traceability, secondary market potential, and investor record-keeping.

Performance Benchmarking: SEBI required AIFs to disclose performance benchmarks through SEBI-registered benchmarking agencies, enabling investors to compare fund returns against appropriate peer groups — a market practice standard in more mature AIF markets like the US and Europe.

Risks and Returns: Understanding AIF Performance

The allure of AIFs lies in their potential to generate alpha — returns above what public markets can deliver — by accessing illiquid, complex, or niche investment opportunities. However, this potential comes bundled with a distinct and often underappreciated risk profile.

Key Risks

Illiquidity Risk: The most significant structural risk. Capital committed to an AIF may be locked in for 7–10 years with limited exit options. Secondary markets for AIF units are nascent in India, though growing.

Valuation Risk: Unlike listed securities, unlisted investments are valued using models, making NAV calculations susceptible to subjectivity and potential manipulation — a risk SEBI's 2023 valuation norms aim to mitigate.

Manager Risk: AIF performance is heavily dependent on the quality of the fund manager. Unlike mutual funds with standardised benchmarking, manager skill dispersion in AIFs is extremely wide.

Concentration Risk: Many AIFs, especially Category I VCFs, hold concentrated positions in a small number of companies. A single bad investment can significantly impair overall returns.

Regulatory and Tax Risk: The evolving nature of AIF regulations — as evidenced by the RBI-SEBI circular on evergreening — means that regulatory changes can materially impact fund structures and returns mid-tenure.

Return Expectations and Benchmarking

Historically, well-managed Indian private equity and venture capital funds have delivered Internal Rates of Return (IRRs) in the range of 15–25%, significantly outperforming listed equity benchmarks over comparable periods. However, these figures mask substantial variance — the top quartile of funds drives most of the industry's returns, while median performers often barely compensate for the illiquidity premium demanded.

Debt-focused Category II AIFs have typically delivered returns of 12–18% — meaningfully higher than fixed deposits or investment-grade corporate bonds — attracting yield-hungry investors, particularly in a declining interest rate environment where RBI's accommodative stance (experts suggest further rate cuts are likely given declining crude oil prices and benign inflation) compresses returns on conventional fixed income.

Conclusion: AIFs as a Strategic Component of India's Capital Markets

Alternative Investment Funds have evolved from niche vehicles for ultra-wealthy families into a mainstream institutional asset class that is reshaping how productive capital flows through India's economy. With SEBI's increasingly sophisticated regulatory framework — anchored by the GARUDA scheme-launch acceleration initiative, independent valuation mandates, and stricter evergreening controls — the structural integrity of the AIF ecosystem is stronger than ever before.

For banking professionals and financial advisors, the imperative is clear: AIFs can no longer be treated as peripheral or exotic additions to a client's portfolio. They represent a legitimate, regulated, and increasingly transparent avenue for deploying patient capital into India's most promising growth stories — from MSME financing and infrastructure development to early-stage technology ventures that will define the next chapter of Viksit Bharat.

The key is disciplined due diligence: evaluating manager track records, understanding fee structures (management fees typically range from 1.5–2.5%, with performance fees or carried interest of 20% above a preferred return hurdle), and ensuring that AIF allocations are appropriately sized within a diversified portfolio. As India's capital markets continue to deepen and the SEBI-mandated benchmarking infrastructure matures, allocating to AIFs will become an increasingly data-driven, transparent, and defensible investment decision.

For investors, the bottom line is this: AIFs offer access to premium return opportunities unavailable through conventional channels — but only for those who can genuinely afford the illiquidity, complexity, and risk that accompanies them. Regulatory literacy, beginning with the framework outlined here, is the first step toward making that access work in your favour.