How DRTs Work in India: A Complete Guide to Debt Recovery Tribunals and NPA Resolution

India's banking sector has long grappled with the burden of non-performing assets (NPAs), and understanding how DRT works in India is essential for anyone involved in banking, lending, or corporate finance. Debt Recovery Tribunals (DRTs) were established as a specialised judicial mechanism to help banks and financial institutions recover dues from defaulting borrowers — faster and more efficiently than the conventional civil court system would allow. With RBI Governor Sanjay Malhotra recently calling for deeper and more efficient financial markets, and the Finance Ministry actively holding talks to push for quicker disposal of cases by DRTs, these tribunals have never been more relevant to India's financial stability agenda. This article provides a comprehensive, step-by-step breakdown of how DRTs function, the extent of their powers, and the reforms being pursued to make them more effective.

What Is a Debt Recovery Tribunal (DRT) and Why Was It Created?

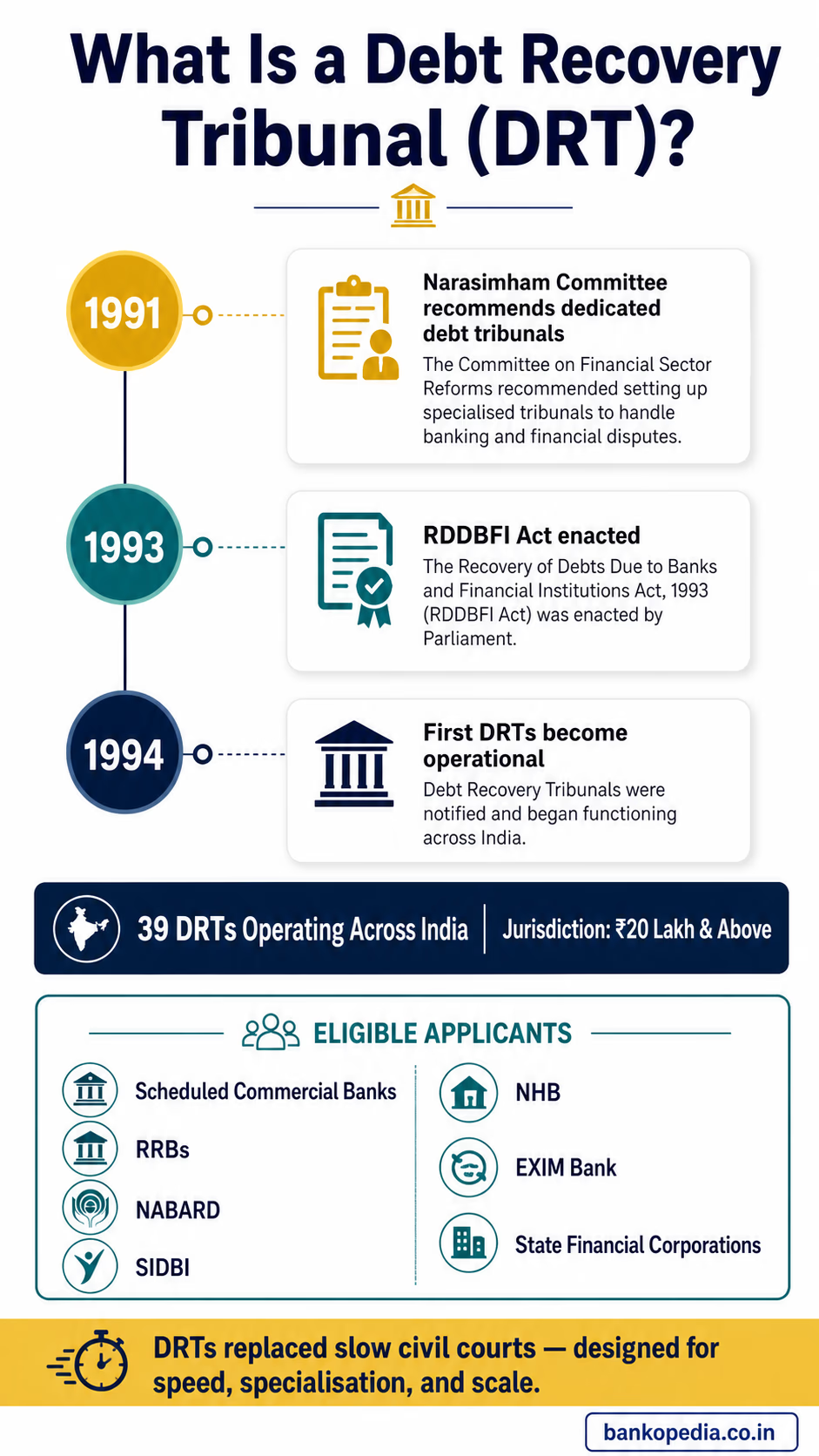

A Debt Recovery Tribunal is a quasi-judicial body established under the Recovery of Debts Due to Banks and Financial Institutions (RDDBFI) Act, 1993. Before DRTs came into existence, banks and financial institutions had to approach regular civil courts to recover dues from defaulting borrowers. Civil courts, already burdened with millions of pending cases, were ill-equipped to handle the specialised, time-sensitive nature of debt recovery. Cases dragged on for years — sometimes decades — leaving banks with mounting NPAs and severely constrained lending capacity.

The Narasimham Committee on Financial System, which submitted its landmark report in 1991, had specifically recommended the creation of dedicated tribunals to address this problem. The government acted on this recommendation, and the RDDBFI Act was enacted in 1993, with the first DRTs becoming operational in 1994.

Currently, there are 39 DRTs operating across India, located in major cities including Mumbai, Delhi, Chennai, Kolkata, Bengaluru, Hyderabad, Ahmedabad, and others. Each DRT is presided over by a Presiding Officer, typically a District Judge-level judicial officer. DRTs have jurisdiction over debt recovery cases where the outstanding amount is ₹20 lakh or more. This threshold was revised upward over time to ensure that only significant debt recovery matters occupy the tribunal's docket.

The key institutions that can file applications before DRTs include:

Scheduled commercial banks (public and private sector)

Regional Rural Banks (RRBs)

Financial institutions notified by the central government, such as NABARD, SIDBI, NHB, and EXIM Bank

State financial corporations

It is important to note that DRTs operate in addition to, not as a replacement for, the SARFAESI Act, 2002 framework. Banks often use both mechanisms concurrently — the SARFAESI Act for secured asset enforcement and DRTs for obtaining a legal decree for the full outstanding amount.

How the DRT Process Works: Step-by-Step for Borrowers and Banks

Understanding how DRT works in India from a procedural standpoint is crucial for both lenders seeking recovery and borrowers who may find themselves on the receiving end of a DRT application. The process is governed primarily by the RDDBFI Act and the Debt Recovery Tribunal (Procedure) Rules, 1993.

Step 1: Filing an Original Application (OA)

The process begins when a bank or financial institution files an Original Application (OA) before the jurisdictionally competent DRT. The OA must contain details of the debt, the borrower's default history, account statements, the loan agreements, and the security interest (if any) created in favour of the bank. The applicant bank pays a filing fee that is calculated as a percentage of the claimed amount, subject to a maximum cap.

Step 2: Issuance of Summons and Service

Once the OA is admitted, the DRT issues summons to the defendant (the borrower and any guarantors). Service of summons can be effected through registered post, courier, or personal service. If the defendant cannot be located, the DRT may permit publication of summons in newspapers.

Step 3: Filing of Written Statement by the Borrower

After receiving summons, the borrower (defendant) has the opportunity to file a written statement contesting the bank's claim. Crucially, no counterclaim by the borrower is permitted in DRT proceedings — the tribunal's jurisdiction is strictly limited to adjudicating the bank's recovery claim. If the borrower has any grievances against the bank, those must be pursued separately in a civil court or other appropriate forum.

Step 4: Hearing and Evidence

Both parties present their evidence — documentary and oral — before the Presiding Officer. The DRT is empowered to summon witnesses, call for documents, and examine parties under oath. The proceedings are intended to be expeditious; the RDDBFI Act originally envisioned disposal within 180 days of filing, though this target has rarely been met in practice due to systemic backlogs.

Step 5: Issuance of a Recovery Certificate

If the DRT finds in favour of the bank, it passes a Recovery Certificate (RC) specifying the amount to be recovered from the borrower. The RC has the effect of a civil court decree and is enforceable as such. The Presiding Officer may also direct the attachment and sale of the borrower's properties — both mortgaged and, in some cases, unmortgaged assets — to satisfy the recovery amount.

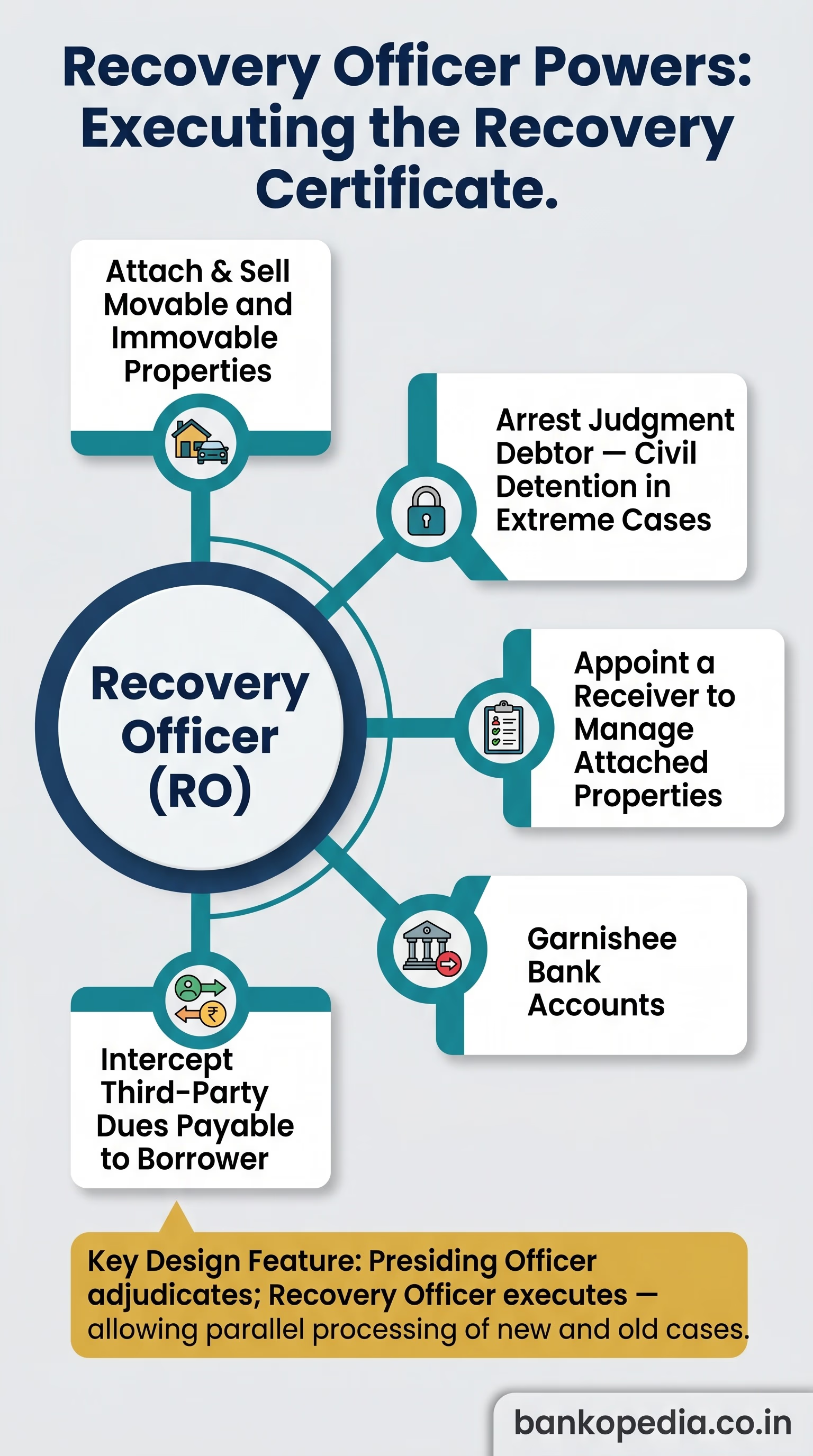

Step 6: Execution by the Recovery Officer

This is a distinctive feature of the DRT system. Each DRT has a designated Recovery Officer (RO) who is responsible for executing the Recovery Certificate. The RO has wide powers, including the authority to:

Attach and sell movable and immovable properties

Arrest the judgment debtor and detain them in civil prison (in extreme cases)

Appoint a receiver to manage attached properties

Garnishee bank accounts and intercept dues payable to the borrower by third parties

The separation of the adjudicatory function (Presiding Officer) from the execution function (Recovery Officer) is a deliberate design feature that allows the Presiding Officer to focus on new cases while the RO pursues recovery on concluded matters.

The Borrower's Right: Counter-Application Under Section 17 of SARFAESI

When a bank initiates action under the SARFAESI Act, borrowers have the right to challenge the bank's actions before the DRT under Section 17 of the SARFAESI Act. This gives DRTs a dual role — not only adjudicating on bank recovery applications but also serving as a check on potential misuse of SARFAESI powers by lenders.

Powers of DRT vs DRAT: Key Differences Explained

A common source of confusion in the DRT framework is the relationship between a DRT and the Debt Recovery Appellate Tribunal (DRAT). These are two distinct tiers in the same adjudicatory hierarchy, with different compositions, powers, and geographic jurisdictions.

Debt Recovery Tribunal (DRT)

DRTs are the trial-level forums in the debt recovery hierarchy. They hear Original Applications filed by banks, applications filed by borrowers under Section 17 of SARFAESI, and execute Recovery Certificates through their Recovery Officers. There are 39 DRTs spread across the country, each with a territorial jurisdiction covering specific states or districts.

Debt Recovery Appellate Tribunal (DRAT)

DRATs are the appellate-level forums, established under Section 8 of the RDDBFI Act. There are currently five DRATs in India, located in Mumbai, Delhi, Chennai, Kolkata, and Allahabad. A DRAT is presided over by a Chairperson who holds the rank equivalent to a High Court judge.

Key distinctions between DRT and DRAT include:

Jurisdiction: DRTs have original jurisdiction; DRATs hear appeals against DRT orders.

Deposit requirement for appeals: Under Section 21 of the RDDBFI Act, a person aggrieved by a DRT order must deposit 75% of the amount ordered to be paid before the DRAT will hear the appeal. This provision — known as the pre-deposit condition — is intended to discourage frivolous appeals, though courts have read in some flexibility for genuine hardship cases.

Further appeal: Orders of a DRAT can be challenged only before the High Court under Article 227 of the Constitution or through a writ petition — there is no further tribunal-level appeal.

Stay of execution: A DRAT can grant a stay of recovery proceedings initiated by a DRT, but only after the pre-deposit condition is satisfied.

The pre-deposit requirement under Section 21 has been a contentious provision — courts have had to balance the need to prevent dilatory tactics by borrowers against the constitutional right to an effective appeal.

From a strategic perspective, lenders prefer DRTs because recovery certificates obtained here can be executed relatively quickly. For borrowers, the DRAT route — while expensive due to the pre-deposit requirement — remains an important safeguard against erroneous DRT orders.

Challenges Facing DRTs in India and Recent Reform Efforts

Despite the sound legislative framework, DRTs have consistently fallen short of their intended purpose of providing swift debt recovery. Several deep-rooted challenges have diminished their effectiveness over the years.

Pendency and Backlog

The most acute problem is the sheer volume of pending cases. As of recent data, DRTs across India have hundreds of thousands of cases pending, with average disposal times running into several years. The Finance Ministry, recognising this as a critical bottleneck, has recently held high-level talks with DRT Presiding Officers and Recovery Officers to push for faster disposal. The DFS Secretary, in recent deliberations on banks' balance sheet constraints, has flagged DRT efficiency as a key lever in reducing NPA overhang on bank books.

Shortage of Presiding Officers and Staff

Many DRTs operate with vacancies at the Presiding Officer level or with officers who are handling additional charge of multiple tribunals. This directly impacts the rate of hearing and disposal. The government has been urged to fill vacancies on a priority basis, and the Law Ministry has been asked to expedite appointments.

Infrastructure Deficiencies

Several DRTs lack adequate physical infrastructure, including courtrooms, document management systems, and digital connectivity. The transition to e-filing and virtual hearings — accelerated by the COVID-19 pandemic — has been uneven across DRTs. Some tribunals have successfully embraced technology, while others continue to struggle with manual processes.

Legal Complexity and Procedural Delays

Borrowers (and sometimes banks) often seek adjournments, file interlocutory applications, and challenge procedural orders at higher courts, contributing to delays. The legal ecosystem around DRT proceedings has become almost as complex as civil court litigation in some cases, defeating the original purpose of the tribunals.

Coordination with Insolvency Proceedings

Since the enactment of the Insolvency and Bankruptcy Code (IBC), 2016, there is sometimes overlap between DRT proceedings and Corporate Insolvency Resolution Process (CIRP) proceedings before the National Company Law Tribunal (NCLT). When a corporate borrower is admitted to CIRP, an automatic moratorium under Section 14 of the IBC halts DRT proceedings. This has created jurisdictional ambiguities that courts are still resolving.

Recent Reform Initiatives

The government and the RBI have undertaken several reform measures to address these challenges:

Digitalisation: The Department of Financial Services (DFS) has been rolling out a National E-Governance Plan for the judiciary, which includes DRT-specific case management software to track filing, hearing dates, and disposal.

Dedicated benches for large-value cases: There is a proposal to designate specific DRT benches exclusively for high-value NPA recovery — cases involving exposures above ₹500 crore — to ensure focused attention on matters that have the greatest systemic impact.

Enhanced coordination with RBI and IBC framework: RBI has been encouraging banks to use a combination of SARFAESI, DRT, and IBC in a coordinated manner, based on the specific profile of the NPA account, rather than treating these as mutually exclusive options.

Amendments to the RDDBFI Act: The RDDBFI (Amendment) Act, 2019 introduced several procedural changes aimed at expediting hearings, including restrictions on adjournments and mandatory timelines for completion of pleadings.

High-level banking panel: DFS Secretary Nagaraju's announcement of a high-level panel to oversee banks' balance sheet constraints signals that NPA resolution — and by extension, DRT performance — will remain under active government monitoring.

Conclusion: The Road Ahead for DRTs in India's Financial Ecosystem

Debt Recovery Tribunals occupy a critical position in India's financial architecture. They serve as the primary judicial forum for banks to enforce their credit rights and are, therefore, directly linked to the health of bank balance sheets, credit availability, and ultimately, India's economic growth story. With India's forex reserves standing at $698.49 billion and the country demonstrating resilience amid global headwinds — as noted by RBI Governor Malhotra — the credibility of domestic credit enforcement mechanisms becomes even more important for sustaining investor confidence.

For DRTs to truly fulfil their mandate, a multi-pronged approach is necessary: timely appointment of qualified Presiding Officers, robust digital infrastructure, strict enforcement of hearing timelines, and better inter-institutional coordination between DRTs, the NCLT, and the RBI. Banks, on their part, must ensure that their legal teams file well-prepared OAs with complete documentation, reducing the scope for procedural delays.

For banking professionals, staying current on DRT jurisprudence — particularly evolving court interpretations on the SARFAESI-DRT interface, the pre-deposit condition, and the interplay with IBC — is no longer optional. It is a core competency in the modern Indian banking environment.

Understanding how DRT works in India is not merely an academic exercise — it is a practical imperative for every lending institution committed to disciplined credit management and sustainable NPA resolution.