How UPI Works in India: A Comprehensive Guide to the Digital Payment Ecosystem

Understanding how UPI works in India has become essential knowledge for banking professionals, fintech practitioners, and everyday consumers alike. The Unified Payments Interface has fundamentally reshaped the country's financial landscape in less than a decade, evolving from a niche digital tool into the backbone of retail payments. In FY26, UPI transaction value crossed a staggering ₹314 lakh crore, a figure that underscores not just adoption but deep structural integration into how India moves money. From street vendors in Varanasi to corporate treasury teams in Mumbai, UPI has democratised real-time payments in a way that few financial innovations anywhere in the world have managed. This article provides a thorough, technically grounded explanation of UPI's architecture, governance, transaction mechanics, security framework, and how it compares to legacy payment rails like NEFT, IMPS, and RTGS.

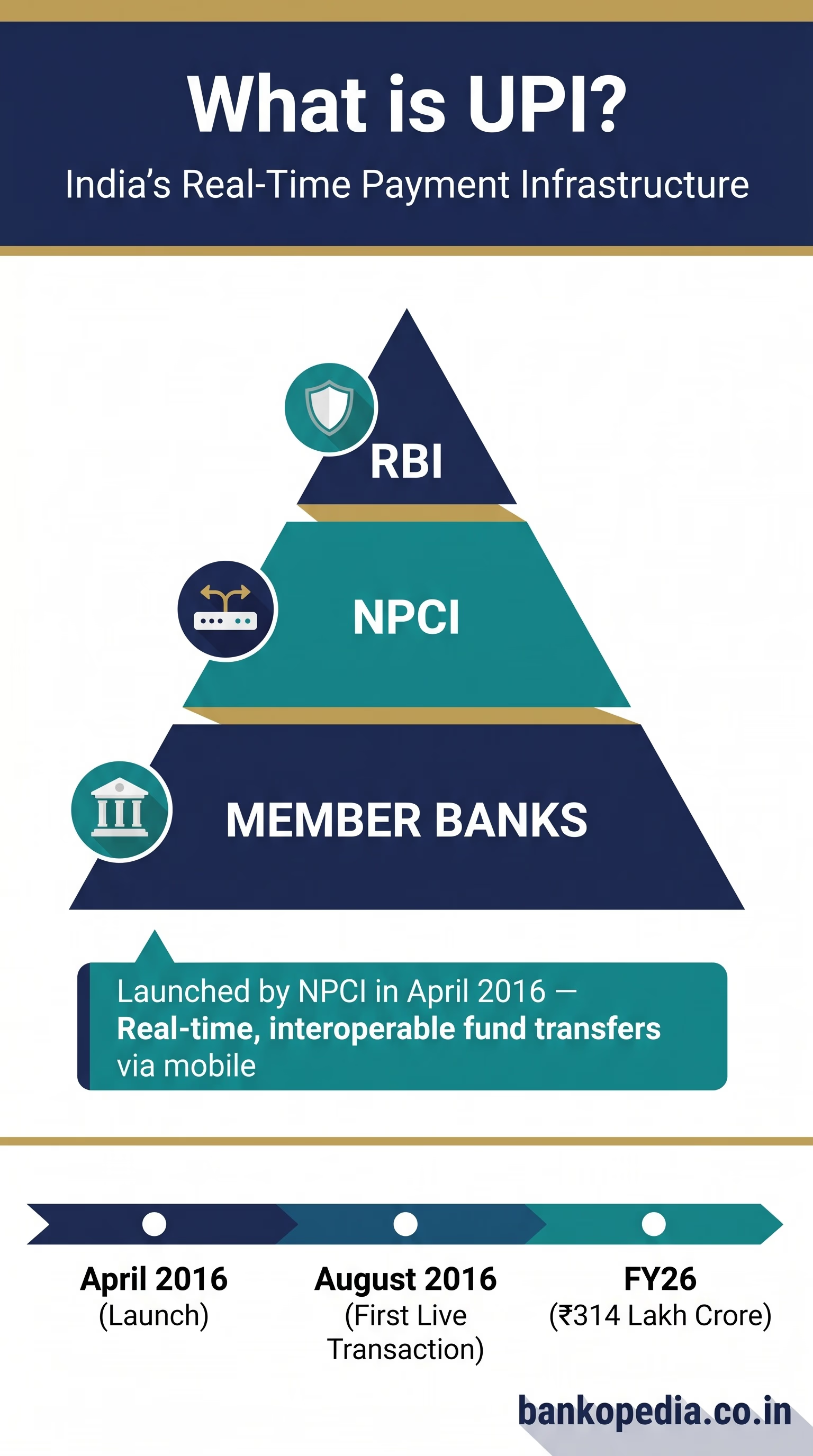

What Is UPI and Who Governs It in India?

UPI, or the Unified Payments Interface, is a real-time interoperable payment system that enables fund transfers between bank accounts through mobile applications. It was conceptualised and launched by the National Payments Corporation of India (NPCI) in April 2016, with the first live transaction processed in August of the same year. NPCI, which operates under the aegis of the Reserve Bank of India (RBI) and the Indian Banks' Association (IBA), functions as the umbrella organisation for retail payment systems in the country.

The regulatory oversight of UPI sits clearly with the RBI, which issues guidelines on transaction limits, participant eligibility, interoperability standards, and consumer protection norms. NPCI acts as the technical operator and settlement institution, maintaining the central switch that routes transactions between member banks and payment service providers (PSPs). The Payment and Settlement Systems Act, 2007 provides the legal scaffolding that gives the RBI its authority to regulate and supervise payment systems, including UPI.

The ecosystem involves several key participants:

Issuer Banks: Banks that hold the customer's account and authenticate payment requests (e.g., SBI, HDFC Bank, ICICI Bank).

Acquirer Banks / PSP Banks: Banks that sponsor third-party UPI applications and route transaction requests to NPCI.

Third-Party Application Providers (TPAPs): Non-bank entities like PhonePe, Google Pay, and Paytm that provide the consumer-facing interface.

NPCI: The central switch responsible for routing, clearing, and facilitating settlement.

Merchants and End Users: The ultimate sender and receiver of funds.

A critical architectural feature of UPI is its use of the Virtual Payment Address (VPA), commonly called a UPI ID (e.g., username@bankname). This abstraction layer maps to a user's actual bank account without exposing sensitive account details, significantly reducing the risk of financial fraud during payment initiation.

UPI also supports multiple payment modes including peer-to-peer (P2P), peer-to-merchant (P2M), collect requests, recurring mandates (UPI AutoPay), and more recently, credit line linkages through the RBI's credit on UPI framework. The system's interoperability — the ability to transact across different banks and apps using a common protocol — is what distinguishes it from closed-loop wallets and makes it a true public digital infrastructure.

How a UPI Transaction Works: Step-by-Step

The apparent simplicity of scanning a QR code or entering a UPI ID belies a sophisticated multi-layered process happening in milliseconds behind the scenes. Here is a granular breakdown of how a standard UPI push transaction (where the sender initiates payment) is processed:

Step 1: Initiation of Transaction

The payer opens a UPI-enabled application — whether a bank's proprietary app or a TPAP like Google Pay — and enters the recipient's VPA, scans a QR code, or selects from a saved contact. The payer specifies the amount and optionally adds a remark or reference number.

Step 2: Authentication via UPI PIN

The transaction request requires the payer to authenticate using their UPI PIN, a 4 or 6-digit numeric code set during onboarding and linked specifically to the bank account chosen for the transaction. This PIN is encrypted on the device and is never transmitted in plain text. The mobile number registered with the bank is also verified at the device level via a one-time SIM binding process during initial registration.

Step 3: Transmission to PSP Bank

The encrypted transaction request travels from the payer's UPI app to the PSP bank's server. The PSP bank packages the request in the NPCI-specified API format and forwards it to the NPCI central switch.

Step 4: NPCI Switch Routing

NPCI's central switch receives the transaction request, validates the format, checks for duplicate transactions, and routes the request to the issuer bank (i.e., the bank holding the payer's account). This routing is based on the VPA-to-account mapping maintained in NPCI's central mapper.

Step 5: Issuer Bank Authorisation

The payer's bank verifies the UPI PIN against its records, checks whether the account has sufficient balance, and confirms account status. If all checks pass, the bank debits the payer's account and sends an authorisation confirmation to NPCI.

Step 6: Credit to Beneficiary

NPCI routes the confirmation to the beneficiary's bank (the payee bank), which credits the recipient's account in real time. A success message is sent back through the chain — from payee bank to NPCI to PSP to the payer's app — completing the transaction loop.

Step 7: Settlement Between Banks

While the end-user experience reflects an immediate transfer, the actual net settlement between banks happens on a deferred basis through the RBI-managed settlement account. NPCI calculates multilateral net positions for all member banks at defined intervals and triggers settlement via the RBI's RTGS system.

The entire process — from PIN entry to the receipt of a success notification — typically completes within 2 to 10 seconds, making UPI one of the fastest real-time payment systems globally.

For UPI collect transactions (pull payments), the process is reversed: the payee initiates a collect request to the payer's VPA, the payer receives a notification, and the payer must explicitly authorise the debit using their UPI PIN before any funds move. This explicit consent mechanism is a key consumer protection feature.

UPI Transaction Limits, Settlement Cycles, and Security

Transaction Limits

The RBI and NPCI have prescribed limits on UPI transactions, which vary by use case:

General P2P and P2M transactions: ₹1 lakh per transaction per day for most bank accounts.

Capital markets, IPO subscriptions, and insurance payments: ₹2 lakh per transaction, following RBI's revised guidelines to encourage UPI adoption in financial services.

Verified merchants in healthcare and education: ₹5 lakh per transaction.

UPI Lite: A simplified offline-capable variant for small-value transactions, with a wallet limit of ₹2,000 and a per-transaction cap of ₹500, designed to reduce server load and improve success rates in low-connectivity areas.

Individual banks may set lower limits based on their internal risk frameworks, and certain payment categories — such as tax payments to government — may carry enhanced limits as permitted by the RBI from time to time.

Settlement Cycles

A common point of confusion, even among banking professionals, is the distinction between real-time credit and actual interbank settlement. When a UPI transaction succeeds, the beneficiary sees the credit immediately because the beneficiary's bank credits the account on a provisional basis, backed by NPCI's guarantee. However, the actual exchange of funds between banks occurs through deferred net settlement (DNS).

NPCI typically runs multiple settlement batches throughout the day. Net positions are calculated and settled through RBI's RTGS in defined settlement cycles. This model manages systemic risk while maintaining the real-time experience for end users. Banks must maintain adequate pre-funded settlement accounts to honour their net obligations.

Security Architecture

UPI's security model is multi-layered and addresses threats at each stage of the transaction:

Device Binding: During registration, the UPI app sends a silent SMS to verify that the mobile number matches the SIM in the device. This links a VPA to a specific device-SIM combination, preventing remote access attacks.

End-to-End Encryption: All transaction data — including the UPI PIN — is encrypted using asymmetric cryptography before leaving the device. Banks use NPCI-certified HSMs (Hardware Security Modules) to process decryption.

Two-Factor Authentication: Every transaction requires both device possession (something you have) and the UPI PIN (something you know), fulfilling the RBI's two-factor authentication mandate for digital payments.

Transaction Monitoring: NPCI and member banks run real-time fraud monitoring engines that flag anomalies such as unusual transaction velocity, atypical geolocation, or mismatched device fingerprints.

Dispute Resolution: NPCI operates a structured dispute management system (UPI Dispute and Complaint Management System) through which failed or disputed transactions are investigated and resolved within defined TATs.

It is worth noting that the RBI's regulatory framework for payment system operators also requires TPAPs and PSP banks to comply with data localisation norms, storing all UPI payment data exclusively on servers located in India — a requirement with significant implications for global tech companies operating in the Indian payments space.

UPI vs NEFT vs IMPS vs RTGS: Key Differences Explained

India's retail and wholesale payment systems each serve distinct purposes, and comparing them clarifies where UPI sits in the broader payments architecture.

UPI (Unified Payments Interface)

UPI is designed for real-time, low-to-medium value retail payments available 24×7×365. It requires only a smartphone and a UPI-linked bank account, with no need to share account numbers. Its primary strengths are speed, interoperability, and the abstraction provided by VPAs. It is governed by NPCI and regulated by RBI.

IMPS (Immediate Payment Service)

Also operated by NPCI, IMPS was the predecessor to UPI for real-time transfers. It functions 24×7 and allows fund transfers using mobile number and MMID (Mobile Money Identifier) or account number and IFSC. IMPS carries a per-transaction limit of ₹5 lakh and typically involves a small fee for the sender. UPI, in many ways, is an evolution of IMPS, built on top of IMPS infrastructure but with superior usability and interoperability.

NEFT (National Electronic Funds Transfer)

NEFT is a deferred settlement system operated by the RBI. Since December 2019, it operates on a 30-minute settlement batch cycle, 24×7. It requires the sender to know the beneficiary's account number and IFSC code. There is no upper transaction limit for NEFT, making it suitable for larger payments that do not need instantaneous settlement. NEFT is widely used for salary disbursements, vendor payments, and EMI collections.

RTGS (Real-Time Gross Settlement)

RTGS is designed for high-value transactions with a minimum threshold of ₹2 lakh. It is operated by the RBI and settles each transaction individually and in real time, with immediate finality — there is no netting or batching. RTGS is primarily used by corporates, financial institutions, and government entities for large-value interbank transfers. It operates 24×7 since December 2020.

Comparative Summary

Speed: RTGS and UPI offer real-time settlement; IMPS is near-real-time; NEFT settles in 30-minute batches.

Transaction Limits: RTGS minimum ₹2 lakh (no upper limit); NEFT no limits; IMPS up to ₹5 lakh; UPI up to ₹1–5 lakh depending on category.

Availability: All four systems now operate 24×7×365.

Use Case: UPI and IMPS for retail; NEFT for mid-range; RTGS for wholesale/high-value.

Information Required: UPI needs only a VPA or mobile number; IMPS needs mobile+MMID or account+IFSC; NEFT and RTGS require full bank account details.

Cost: UPI is zero-charge for end users (per RBI mandate since January 2020); IMPS and NEFT may carry nominal fees; RTGS may have charges at the bank's discretion.

UPI's Expanding Role and Future Trajectory

UPI's role in India's financial ecosystem continues to expand beyond simple person-to-person transfers. The RBI's push to allow credit lines on UPI — enabling pre-sanctioned credit from banks to flow through the UPI rail — is opening a new chapter in embedded lending. This development aligns with broader financial inclusion goals, including initiatives like the Svamitva scheme, where rural property rights documentation is improving collateral availability and credit access for rural households, as highlighted in recent IIM Ahmedabad research.

NPCI International is also extending UPI's reach globally, with live deployments in Singapore, UAE, France, and several other countries, positioning the VPA-based payment model as a potential global standard. The RBI's dialogue with counterpart central banks on interlinking fast payment systems further elevates UPI's strategic significance.

Meanwhile, with SEBI operationalising new platforms like PaRRVA for the securities market and the broader ecosystem of regulated financial infrastructure maturing, UPI's integration into capital market applications — IPO subscriptions via ASBA+UPI, mutual fund transactions, and insurance premium payments — is deepening the interface between retail banking, capital markets, and insurance regulation.

Conclusion

UPI is not merely a payment application — it is a public digital infrastructure that has redefined financial access, velocity, and inclusion in India. Its architecture, grounded in robust security, regulatory oversight by the RBI, and technical management by NPCI, ensures that real-time payments can be trusted at scale. For banking professionals, understanding the mechanics of UPI — from VPA mapping and device binding to settlement cycles and fraud controls — is increasingly non-negotiable, as the system underpins everything from retail transactions to regulatory reporting in India's evolving digital economy. With transaction values surpassing ₹314 lakh crore in a single fiscal year, UPI's growth trajectory shows no signs of plateauing; if anything, its integration into credit, international remittances, and regulated financial products will only deepen its centrality to India's financial system in the years ahead.