Crypto Regulation in India: RBI & Government Stance Explained

The question of crypto regulation in India has become one of the most debated subjects in Indian banking and financial policy circles over the past decade. Despite India being home to one of the world's largest retail crypto trading populations — with estimates suggesting over 20 million active investors — the country still lacks a comprehensive, standalone legislative framework governing cryptocurrencies and digital assets. The Reserve Bank of India (RBI), the Securities and Exchange Board of India (SEBI), and the central government have each taken positions that have evolved considerably over time, often in response to global developments, domestic market pressures, and the rapid pace of technological change. As the global regulatory landscape begins to crystallise — with the European Union's MiCA framework coming into force and the United States inching towards clearer crypto legislation — India's wait-and-watch approach is increasingly coming under scrutiny. The time for a decisive, well-calibrated regulatory architecture may no longer be optional.

Why India Has Struggled to Regulate Cryptocurrency

India's difficulty in arriving at a coherent crypto regulatory framework is not simply a failure of political will. It reflects genuinely complex structural, legal, and philosophical tensions that have no easy resolution. Understanding these challenges is essential for any banking professional or policymaker seeking to make sense of where India stands today.

The Classification Problem

At the heart of India's regulatory paralysis is a fundamental question: what exactly is a cryptocurrency? Is it a currency, a commodity, a security, or an entirely new asset class? The answer determines which regulator has jurisdiction — the RBI, SEBI, the Forward Markets Commission (now merged into SEBI), or an entirely new body. Without statutory clarity on classification, overlapping mandates and regulatory gaps are inevitable.

In many Western jurisdictions, regulators have been forced to resolve this ambiguity through court rulings or legislative intervention. India has so far avoided this reckoning, partly because each classification carries significant implications for existing laws, including the Foreign Exchange Management Act (FEMA), the Securities Contracts (Regulation) Act (SCRA), and the Prevention of Money Laundering Act (PMLA).

The Sovereignty and Monetary Policy Concern

The RBI has long maintained that privately issued digital currencies pose a fundamental challenge to monetary sovereignty. If a significant portion of transactions in the Indian economy were to migrate to decentralised crypto assets — which operate outside the purview of any central bank — it could undermine the RBI's ability to implement monetary policy, manage liquidity, and maintain financial stability. This concern is not unique to India, but it carries special weight in a developing economy where the central bank's transmission mechanisms are still being strengthened.

Investor Protection and Retail Vulnerability

India's retail investor base is large, often under-informed, and frequently attracted to high-yield, speculative instruments. The crypto boom of 2020–2021 saw millions of Indians — many of them first-time investors — pour money into digital assets without adequate disclosure frameworks, grievance redressal mechanisms, or any formal investor protection net. The absence of regulation left them exposed to exchange failures, rug pulls, and extreme volatility. Unlike equity markets, where SEBI's investor protection norms provide a baseline of safety, crypto investors in India operate in a regulatory vacuum.

The Global Coordination Challenge

Cryptocurrencies are inherently cross-border. An Indian investor can hold Bitcoin on a foreign exchange, move funds through decentralised finance (DeFi) protocols, and exit through peer-to-peer channels — all of which are difficult to monitor under existing domestic regulations. Effective crypto regulation requires international coordination, and India's regulatory response has partly been constrained by the absence of a global consensus. The G20 presidency that India held in 2023 offered an opportunity to push for coordinated global standards, and while some progress was made in framing common principles, binding international rules remain elusive.

RBI's Historical Stance on Crypto and Digital Assets

The RBI's position on cryptocurrencies has been one of deep, institutionalised scepticism — and understanding this trajectory is critical to understanding where crypto regulation India RBI dynamics currently stand.

The 2018 Banking Ban and Its Aftermath

In April 2018, the RBI issued a circular directing all entities regulated by it — banks, NBFCs, and payment service providers — to cease providing services to individuals or businesses dealing in virtual currencies. This effectively cut off the banking lifeline of India's nascent crypto industry, forcing many exchanges to shut down or pivot to peer-to-peer trading models.

The crypto industry challenged this circular in the Supreme Court of India. In March 2020, the Supreme Court delivered a landmark verdict in the Internet and Mobile Association of India v. Reserve Bank of India case, setting aside the RBI's circular on the grounds that it was disproportionate and failed to demonstrate actual harm to the financial system. The ruling was a significant blow to the RBI's hardline position and temporarily reopened the banking channels for crypto businesses.

"The Supreme Court's 2020 ruling made clear that the RBI could not impose sweeping restrictions without demonstrating proportionate harm — a precedent that continues to shape the regulatory debate."

Post-2020: Cautious Engagement, Persistent Opposition

Despite the Supreme Court's verdict, the RBI did not soften its philosophical opposition to private cryptocurrencies. Senior RBI officials, including successive Governors and Deputy Governors, have consistently described cryptocurrencies as having no underlying value, posing macroeconomic risks, and being instruments of speculation rather than genuine financial innovation. The RBI has repeatedly called for a complete ban on private cryptocurrencies, arguing that partial regulation is insufficient to address systemic risks.

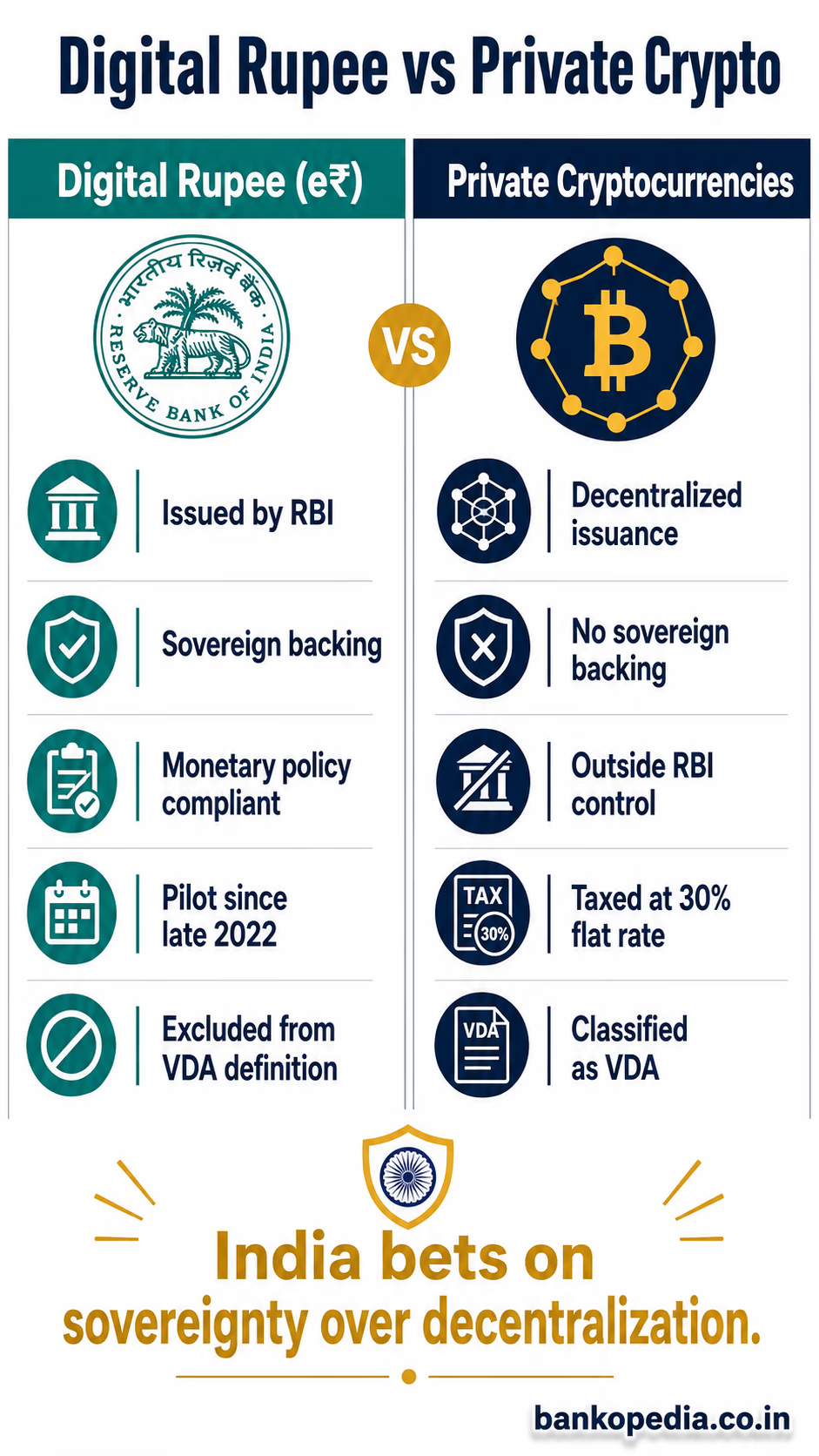

Simultaneously, the RBI has channelled its digital currency ambitions into the development of the Digital Rupee (e₹) — India's Central Bank Digital Currency (CBDC). Pilot programmes for both the wholesale and retail versions of the e₹ have been underway since late 2022. The RBI's logic is transparent: a sovereign digital currency can deliver the efficiency and programmability benefits of blockchain-based money without ceding monetary control to decentralised, privately issued tokens.

The PMLA Extension: A Regulatory Foothold

A significant regulatory development came in March 2023, when the Government of India brought Virtual Digital Asset (VDA) service providers under the Prevention of Money Laundering Act (PMLA). This required crypto exchanges and VDA intermediaries to register with the Financial Intelligence Unit (FIU-IND), conduct Know Your Customer (KYC) checks, and report suspicious transactions. Several offshore exchanges that failed to comply were subsequently blocked by the government. While not a comprehensive regulatory framework, the PMLA extension provided the first meaningful regulatory foothold over the crypto ecosystem and signalled that the government was moving — however cautiously — towards oversight rather than outright prohibition.

How India Taxes Crypto: TDS, 30% Flat Tax, and VDA Rules

In the absence of a standalone crypto law, India's most concrete regulatory intervention to date has come through the tax framework. The Union Budget 2022-23 introduced a dedicated tax regime for Virtual Digital Assets, which took effect from April 1, 2022. While the taxation rules do not constitute full-spectrum regulation, they represent formal state recognition of crypto as an asset class — a point of considerable legal and policy significance.

The 30% Flat Tax on VDA Gains

Under Section 115BBH of the Income Tax Act, any income from the transfer of a Virtual Digital Asset is taxed at a flat rate of 30%, irrespective of the investor's income slab or holding period. This is among the steepest crypto tax rates in the world and is at par with the tax treatment of lottery winnings and gambling income — a categorisation that many in the crypto industry have found philosophically objectionable, arguing it signals that the government views crypto as speculative rather than as a legitimate investment asset.

Key features of the VDA tax regime include:

No deduction for losses: Losses from one VDA cannot be set off against gains from another VDA or any other income head. Each transaction is evaluated independently.

No benefit of indexation: Unlike equity or real estate, there is no inflation adjustment available on the cost of acquisition.

Cost of acquisition only: The only deduction permissible is the cost of acquiring the VDA. Transfer, mining, or staking costs are not deductible.

Gifted VDAs: The recipient of a gifted VDA is liable to pay tax on its fair market value at the time of receipt, subject to applicable gift tax exemptions.

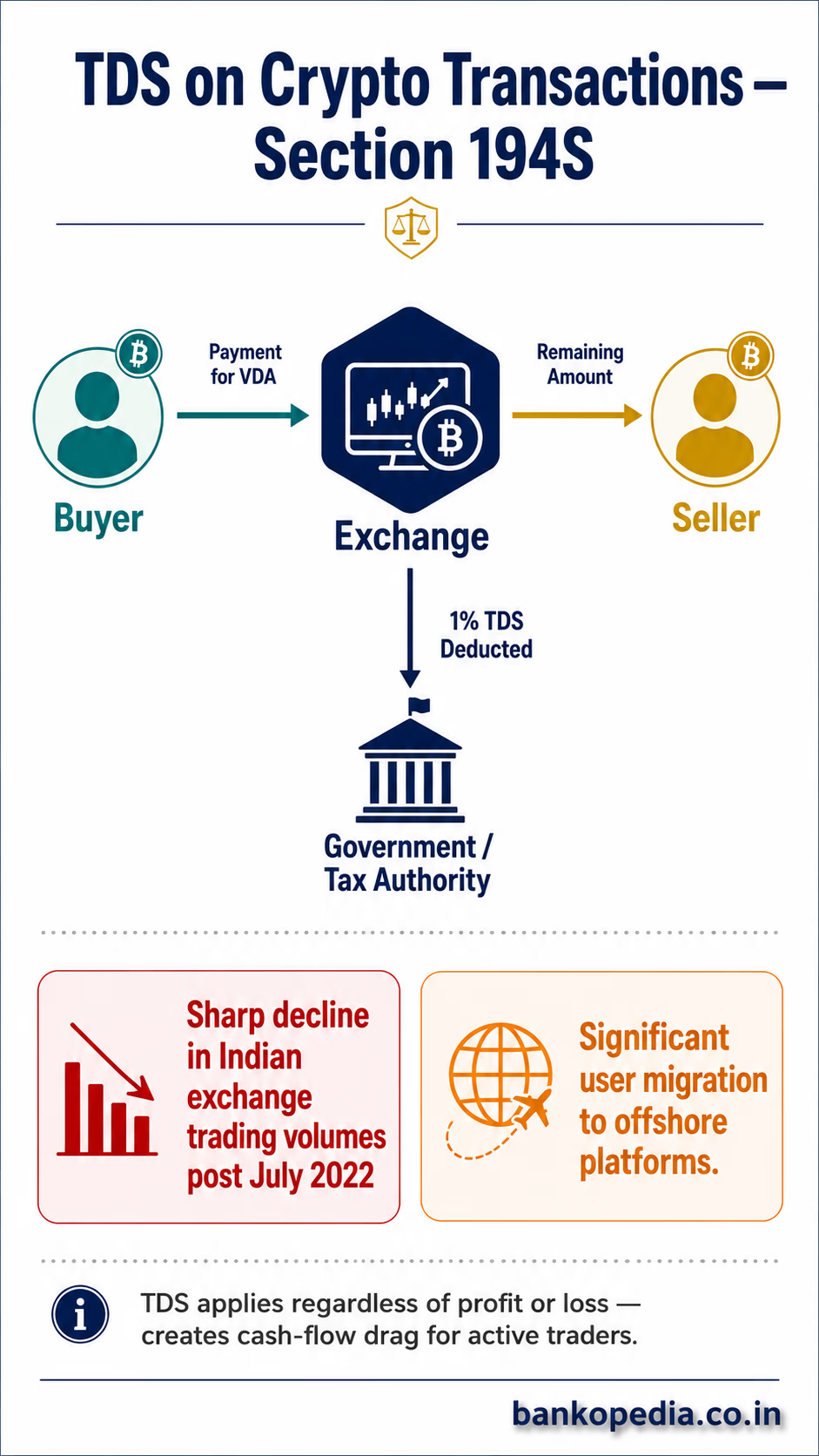

TDS Under Section 194S

Section 194S mandated Tax Deducted at Source (TDS) at 1% on payments made for the transfer of VDAs, effective July 1, 2022. The provision applies to buyers — whether individuals or entities — who make payments to sellers of VDAs. For transactions on recognised exchanges, the TDS obligation generally falls on the exchange itself.

The practical impact of TDS has been significant. The 1% deduction on every transaction — regardless of profit or loss — creates a cash-flow drag for active traders. Industry data following the introduction of TDS showed a sharp decline in trading volumes on Indian exchanges, with a significant migration of users to offshore platforms. This behavioural shift itself underscores the regulatory challenge: excessive taxation without corresponding legitimacy and protection has driven activity underground or offshore, reducing rather than enhancing the government's visibility into crypto transactions.

The VDA Definition Under Indian Law

Section 2(47A) of the Income Tax Act defines a Virtual Digital Asset broadly to include any information, code, number, or token generated through cryptographic means, providing a digital representation of value. Non-Fungible Tokens (NFTs) are also included within this definition. Notably, the RBI's Digital Rupee and any currency issued by a foreign central bank are explicitly excluded from the VDA definition — a distinction that preserves the privileged status of sovereign digital currencies.

What a Future Crypto Regulatory Framework in India Could Look Like

Notwithstanding the current regulatory ambiguity, there are credible signals that India will eventually need to move towards a more structured framework. The question is not whether regulation will come, but what form it will take and which institutional architecture will govern it.

A Dedicated Crypto Legislation

The most comprehensive approach would involve a standalone Virtual Digital Assets (Regulation) Bill — a legislative instrument that defines crypto assets, establishes registration and licensing requirements for exchanges and intermediaries, mandates disclosure standards, creates investor grievance mechanisms, and sets capital adequacy norms for crypto service providers. A draft cryptocurrency bill has reportedly been under consideration since 2021, but has not been tabled in Parliament. The legislative approach would provide the clearest legal certainty for businesses and investors.

A Dual Regulatory Model: RBI and SEBI

Given the heterogeneity of the crypto asset ecosystem, a single regulator may not be adequate. A probable model — and one that aligns with international best practices — would involve a split jurisdiction:

RBI oversight for stablecoins, payment tokens, and any crypto assets that function as a medium of exchange or store of value, given their implications for monetary policy and payment systems.

SEBI oversight for crypto assets that function as securities or investment instruments — including utility tokens and potentially certain categories of DeFi protocols — given SEBI's existing expertise in market regulation, disclosure frameworks, and investor protection.

This bifurcated model would require careful statutory demarcation to prevent regulatory gaps and arbitrage, but it would leverage the existing institutional competencies of India's two most sophisticated financial regulators.

Licensing and Exchange Accountability

Any credible framework must address the accountability of crypto exchanges — both Indian and foreign. Exchanges serving Indian users should be required to hold a domestic licence, maintain a minimum level of capital, keep user funds in segregated accounts, and submit to periodic audits. The collapse of global exchanges like FTX, which had a significant Indian user base, demonstrated the catastrophic consequences of unregulated custodial platforms. India's PMLA registration is a first step, but it addresses only AML compliance — not prudential soundness or consumer protection.

International Alignment and the G20 Framework

India's regulatory framework, when it arrives, will need to be compatible with the Financial Stability Board (FSB) and International Monetary Fund (IMF) recommendations on crypto asset regulation — principles that India itself helped shape during its G20 presidency. These principles emphasise the importance of "same activity, same risk, same regulation," meaning that crypto assets performing the same economic function as traditional financial instruments should face equivalent regulatory scrutiny.

Addressing the Offshore Migration Problem

Any domestic regulation must grapple with the uncomfortable reality that Indian users can easily access offshore exchanges. Regulatory arbitrage — where users migrate to less-regulated foreign platforms to avoid domestic taxes or compliance requirements — is already happening. Effective regulation will require a combination of exchange licensing, geofencing requirements for non-compliant offshore platforms, and potentially FEMA amendments that clarify the legality of holding crypto assets in offshore accounts.

Conclusion: The Cost of Regulatory Inertia

India's approach to crypto regulation has been characterised by caution, ambiguity, and periodic interventionism — a combination that has served neither the industry nor investors particularly well. The 30% tax and TDS regime, while providing revenue certainty, has suppressed legitimate domestic market activity and pushed users towards offshore and peer-to-peer channels that are far harder to monitor. Meanwhile, the RBI's CBDC push, while worthy in itself, does not address the reality that millions of Indians are already participating in the broader global crypto economy.

The signals from India's regulatory establishment suggest that a rethink is underway. The extension of PMLA to VDA service providers, the ongoing CBDC pilots, and the increasing global pressure to align with FSB norms all point towards eventual formalisation. What India needs now is the political and institutional will to move from piecemeal interventions to a coherent, comprehensive framework that protects investors, preserves monetary sovereignty, enables innovation, and integrates India's crypto economy into the formal financial system.

For Indian banking professionals, the evolution of this regulatory space will have direct implications — from how banks treat crypto-holding customers, to AML compliance obligations, to the eventual co-existence of the Digital Rupee with private digital assets. Staying informed on this rapidly evolving subject is no longer optional. It is a professional imperative.