This article reflects information available as of March 2026. Always verify the latest details directly on www.cgtmse.in before applying.

CGTMSE Guarantee Scheme: Complete Guide for MSMEs

Published: 4 March 2026Updated: 6 March 2026By Prashant

P

PrashantAUTHOR

Prashant is a banking and finance professional with 11 years of industry experience. A qualified JAIIB and CAIIB holder and certified Credit Professional, he has completed the Applied Financial Risk Management programme at IIM Kashipur. He specialises in banking regulation, credit risk, financial technology, and exam preparation for banking professionals across India.

JAIIBCAIIBCredit ProfessionalApplied Financial Risk Management — IIM Kashipur11 Years in Banking & Finance

Bankopedia on Telegram

Never Miss a Banking Update

India's sharpest banking intelligence — RBI policy decoded, market moves, JAIIB & CAIIB prep tips, and one key term every morning. Free, forever.

🏦RBI Updates

📖Daily Vocab

📝Exam Tips

⚡Market Moves

Introduction: Why CGTMSE Is the Most Powerful Credit Tool for Indian MSMEs in 2026

Every year, thousands of promising Indian businesses fail—not because their ideas are weak, but because banks demand collateral they simply don’t have. A first-generation entrepreneur in Ludhiana running a precision parts workshop, or a woman-owned food processing unit in Coimbatore with steady orders and no fixed assets to pledge—these are exactly the businesses the Indian economy needs, and exactly the businesses traditional credit shuts out.

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) was built to break this deadlock. Since its inception in 2000, the scheme has enabled over 65 lakh collateral-free loan accounts worth more than ₹5 lakh crore in cumulative guarantees, standing between millions of entrepreneurs and the collateral trap that has historically stunted MSME growth in India.1

In 2025–2026, CGTMSE has never been more relevant. With the Union Budget 2025–26 expanding the corpus, revised guarantee limits, restructured fee slabs, and a push toward digital onboarding for Member Lending Institutions (MLIs), the scheme is actively being repositioned as India’s frontline credit inclusion tool for the next decade.

This guide gives you everything you need to know—from eligibility and loan limits to the exact application process, recent 2025 revisions, and hard-won practical wisdom—to confidently use CGTMSE to unlock growth capital for your business.

⚠️ Scam Alert: The only official website for CGTMSE is www.cgtmse.in. Do not trust any third-party portals, agents, or WhatsApp groups claiming to process CGTMSE applications for a fee. No fee is payable to intermediaries.

What Is the CGTMSE Guarantee Scheme?

The CGTMSE scheme is a credit guarantee programme jointly established by the Government of India (Ministry of MSME) and SIDBI (Small Industries Development Bank of India) in August 2000. Its core purpose is simple: it guarantees a portion of the loan taken by a micro or small enterprise from an eligible bank or financial institution, so that the borrower does not need to provide collateral or third-party guarantees.

Think of it as a government-backed insurance policy for your lender. The bank lends to you without security. If you default, CGTMSE compensates the bank up to the guaranteed percentage. This de-risks the lender, which is why they’re willing to extend credit without asking you to mortgage your house.

Who runs it? CGTMSE is a trust managed by SIDBI with contributions from the Ministry of MSME. Its governing council includes representatives from SIDBI, the Ministry of Finance, Ministry of MSME, IBA, and independent professionals.

Who are the Member Lending Institutions (MLIs)? Banks, NBFCs, and financial institutions that have registered with CGTMSE to offer guaranteed loans. As of early 2026, there are over 200 MLIs including all scheduled commercial banks, select Regional Rural Banks (RRBs), Small Finance Banks (SFBs), and NBFC-MFIs.2

Key Features & Benefits

FeatureDetailsNo Collateral RequiredBorrower does not need to pledge any fixed asset or personal propertyNo Third-Party GuaranteePromoter guarantee not required (personal guarantee of borrower is generally accepted)Wide Eligible Loan TypesTerm loans, working capital, composite loans (term + WC), retail trade loansCoverage up to ₹10 CroreGuarantee cover available for credit facilities up to ₹10 croreEnhanced Cover for Women/SC/ST/NEHigher guarantee percentage for priority borrower categoriesOne-Time + Annual FeeTransparent fee structure (Annual Guarantee Fee charged annually)Digital Claim ProcessClaims processed digitally through MLI portalBroad Sector CoverageManufacturing, services, retail trade (as revised), and select new sectorsWorks Alongside TReDSCGTMSE covers term loans & WC limits; pair it with TReDS invoice discounting for a complete liquidity stack

Top Benefits for MSME Owners

Access credit on the strength of your business idea, not your ancestral property

Preserve family assets—no risk of losing your home if business hits a rough patch

Faster loan approval since banks have a backstop guarantee

Eligible for bank credit from Day 1, including startups (with caveats—see eligibility section)

Women entrepreneurs and SC/ST/NE borrowers get higher coverage, making banks more willing to lend

Eligibility Criteria

Who Can Apply?

ParameterRequirementEnterprise TypeMicro and Small Enterprises as defined under MSMED Act 2006 (and as revised in 2020)RegistrationValid Udyam Registration Certificate (Udyam Aadhaar) mandatoryActivityManufacturing or Service sector (retail trade up to prescribed limits also included post-2023 revision)Loan TypeNew term loan, working capital, or composite loan (fresh sanctions only; top-ups covered with conditions)Credit FacilityUp to ₹10 crore per borrower (per enterprise, not per promoter)Existing LoansNot eligible if borrower has an existing NPA with any bank/FI at the time of applicationSelf-Help GroupsEligible under certain sub-schemesStartupsEligible if they hold Udyam Registration and meet DPIIT recognition criteria (select MLIs)

Who Is NOT Eligible?

Medium Enterprises (above Small Enterprise threshold under MSMED Act 2020) — note: certain medium enterprise sub-schemes may exist; verify on cgtmse.in

Agricultural activities (primary farming, horticulture as a standalone activity)

Educational institutions and training institutes (except skill development linked to MSME activity)

Retail trade loans above the revised ceiling (check current MLI guidelines)

Borrowers with wilful default history or any active NPA account

Loans already covered under any other government credit guarantee scheme for the same facility (no double guarantee cover)3

Practical Tip: Many rejections happen because the bank doesn’t check the borrower’s Udyam Registration status carefully. Ensure your Udyam certificate clearly reflects the correct enterprise size (Micro or Small). If you’ve recently crossed the Medium threshold due to turnover revision, confirm classification before applying.

Loan Limits, Guarantee Coverage & Categories (2025–2026)

This is the section most borrowers get confused about. The coverage percentage depends on your borrower category, loan amount slab, and whether your enterprise is in a priority geography or segment.

Guarantee Coverage Structure (Post April 2025 Revision)

Borrower CategoryLoan AmountGuarantee CoverMicro Enterprises (general)Up to ₹5 lakh85%Micro Enterprises (general)Above ₹5 lakh – ₹50 lakh80%Micro Enterprises (general)Above ₹50 lakh – ₹10 crore75%Small Enterprises (general)Up to ₹50 lakh75%Small Enterprises (general)Above ₹50 lakh – ₹10 crore75%Women Entrepreneurs / AgniveersUp to ₹10 crore90%SC / ST / PwD / Transgender borrowersUp to ₹10 crore85%NE Region / J&K / Ladakh / Aspirational DistrictsUp to ₹10 crore85%Startups (DPIIT Recognised)*Up to ₹10 crore85%ZED Certified MSMEsUp to ₹10 crore85%Retail & Wholesale TradeUp to ₹10 crore75% (or higher, depending on Micro slab/category)

Note on Startups: While CGTMSE covers up to ₹10 crore, the separate Credit Guarantee Scheme for Startups (CGSS) recently had its limit enhanced to ₹20 crore.

Key Revisions Applied:

The ₹10 Crore Ceiling: Every row that previously capped out at ₹5 crore has been updated to ₹10 crore (as per Circular No. 250/2024-25).

Women Entrepreneurs: Coverage was enhanced from 85% to an unprecedented 90% to aggressively push women-led MSME credit.

ZED Certified MSMEs: Coverage was bumped up from 80% to 85%, alongside a 10% concession on the annual guarantee fee.

Retail/Wholesale Trade Parity: Trade activities are no longer heavily restricted. They have been fully aligned with manufacturing and services, meaning they are now eligible for the full ₹10 crore ceiling instead of the old ₹1 crore cap.

⚠️ Important: The above table reflects the structure as understood from CGTMSE revisions announced through 2024–2025. Specific sub-slab rates and category definitions are subject to revision. Always confirm the applicable rate with your MLI and on www.cgtmse.in before relying on these figures.

What does “guarantee cover” mean in practice? If your loan is ₹20 lakh and the guarantee coverage is 80%, then CGTMSE guarantees ₹16 lakh to the bank. If you default, the bank can claim up to ₹16 lakh from CGTMSE. The remaining ₹4 lakh (20%) is the bank’s risk. This is why banks still evaluate creditworthiness—they do carry residual risk.

Guarantee Fees & Charges

CGTMSE charges an Annual Guarantee Fee (AGF), which is typically paid by the borrower (sometimes absorbed by the MLI, depending on the bank’s policy and scheme linkage). There is no one-time upfront guarantee fee for most categories—the fee is annual.

Annual Guarantee Fee Structure (Indicative — Verify on cgtmse.in)⁵

Credit Facility AmountAGF Rate (Standard Rate % p.a.)Up to ₹10 lakh0.37%Above ₹10 lakh – ₹50 lakh0.55%Above ₹50 lakh – ₹1 crore0.60%Above ₹1 crore – ₹2 crore0.85%Above ₹2 crore – ₹5 crore1.00%Above ₹5 crore – ₹8 crore1.10%Above ₹8 crore – ₹10 crore1.20%

Concessional rates apply for:

Women / SC / ST / PwD / NE Region / Aspirational Districts / ZED-certified MSMEs: Reduced AGF (typically a 10% concession on the standard rate — verify current slabs).

Note: The final fee may also vary based on your bank’s risk premium; banks with better portfolios pass on additional discounts to borrowers.

Practical Tip: The AGF is generally charged on the guaranteed amount for the first year and on the outstanding amount for the remaining tenure of the loan. However, computation practices can still vary slightly by bank. Ask your bank explicitly: “How do you compute the CGTMSE fee—on sanctioned or outstanding?” This difference can significantly affect your effective borrowing cost, especially in the early years of a term loan.

Who pays the AGF?

Most banks pass the AGF to the borrower as part of the loan processing/servicing charges

Some government-linked schemes (like PM SVANidhi top-ups or Jan Samarth linked loans) may have the AGF subsidised

Always ask: “Is the CGTMSE fee included in my stated interest rate or charged separately?”

Step-by-Step Application Process

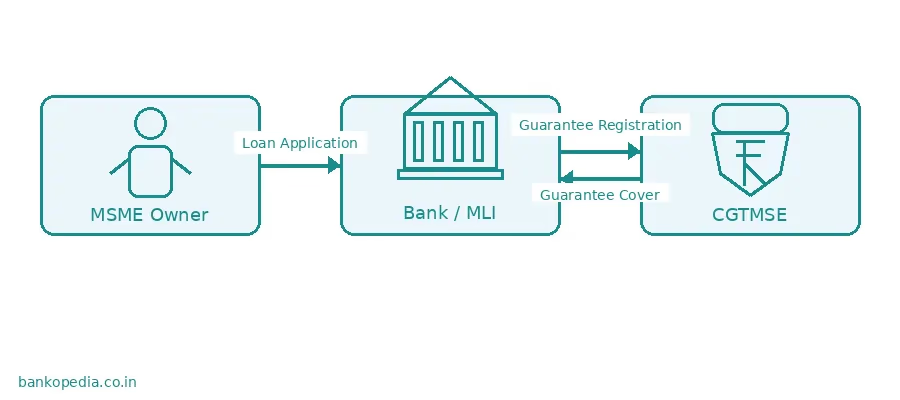

CGTMSE guarantees are not applied for directly by the borrower. The bank (MLI) files the guarantee application on the borrower’s behalf after sanctioning the loan. Here is the full process from the borrower’s perspective:

Step 1: Identify and Approach an MLI

Visit the CGTMSE website → Member Lending Institutions section to find registered banks and NBFCs. All major PSU banks, most private banks, SFBs like AU, ESAF, and Jana Bank, and select NBFCs are registered MLIs.

Step 2: Submit Your Loan Application to the Bank

Apply for a term loan, working capital, or composite loan. Clearly mention that you want the loan covered under the CGTMSE scheme. Banks are obligated to consider CGTMSE coverage for eligible MSME borrowers.

Step 3: Bank Credit Appraisal

The bank evaluates your business based on:

Financial statements (P&L, Balance Sheet, ITR, GST returns)

Business vintage, projections, and repayment capacity

Credit bureau score (CIBIL/Experian/CRIF)

Udyam Registration status

Step 4: Loan Sanction & CGTMSE Guarantee Filing

Once the bank sanctions the loan, the MLI logs in to the CGTMSE portal and registers the guarantee cover for your account. The bank pays the first year’s AGF to CGTMSE at this stage (and may recover it from you).

Step 5: Loan Disbursement

After guarantee registration is confirmed by CGTMSE (typically within 1–3 working days for online submission), the bank disburses the loan.

Step 6: Annual Renewal

The CGTMSE guarantee must be renewed annually by the MLI by paying the AGF for each subsequent year. If the bank fails to renew, the guarantee lapses and the bank loses claim rights—but your loan obligation continues unchanged. The renewal is the bank’s responsibility.

Practical Tip: Ask your Relationship Manager to share the CGTMSE guarantee registration number (also called CGN — Credit Guarantee Number). Keep this safely. It proves your loan is covered and is needed if you ever need to raise a dispute or query on the scheme’s portal.

Documents Required (Checklist)

While the exact document list varies by bank and loan type, here is the standard checklist for a CGTMSE-backed MSME loan:

Identity & Registration Documents

Udyam Registration Certificate (mandatory)

PAN Card of enterprise and promoter(s)

Aadhaar Card of all promoters/directors

GST Registration Certificate (if applicable)

Certificate of Incorporation / Partnership Deed / Proprietorship declaration

Financial Documents

Last 2–3 years audited financial statements (Balance Sheet + P&L)

Last 2–3 years ITR (enterprise + promoters)

GST returns for last 12 months

Bank statements for last 12 months (all business accounts)

Projected financials for loan tenure (for term loans above ₹25 lakh, typically)

Business Documents

Business plan / project report (especially for new or expansion loans)

Quotations for machinery / equipment (for capex loans)

Work orders / buyer contracts (if available — significantly improves sanction prospects)

MSME DI / industry registration (if sector-specific)

Property Documents (if offering any security — not mandatory under CGTMSE)

Not required under CGTMSE, but banks may ask for documents of the business premises (leased or owned)

Common Pitfall: Many applicants are rejected because their bank statements show low or irregular Average Monthly Balance, or because GST returns don’t reconcile with bank credits. Spend 2–3 months cleaning up these discrepancies before applying.

Claim Settlement Process

This section is primarily relevant to understand how the scheme protects banks, but MSME owners benefit from knowing how claims work—it explains why banks do take CGTMSE cover seriously.

Loan turns NPA: If a borrower defaults and the loan is classified as Non-Performing Asset (NPA) by the bank, the MLI can initiate the guarantee claim process.

Invocation of Guarantee: The MLI must invoke the guarantee within the prescribed period (typically within 1 year of the NPA date or 3 years of the guarantee expiry, whichever is earlier—verify current rules on cgtmse.in).

75% Payout (First Instalment): Upon receipt of a valid claim, CGTMSE releases 75% of the eligible claim amount to the bank.

Recovery Proceedings by Bank: The bank must continue recovery proceedings against the borrower.

Final Settlement: After recovery (or after a prescribed period), CGTMSE settles the balance 25% of the claim.

No Impact on Borrower’s Legal Obligation: The claim settlement does not extinguish the borrower’s debt. The bank (and/or CGTMSE via subrogation) continues recovery action.

For Borrowers: Don’t assume that CGTMSE cover means you can walk away from a default consequence-free. Your CIBIL score will be impacted, the bank will pursue recovery, and CGTMSE can also initiate recovery against you after paying the bank.6

Recent Updates & Revisions (2024–2026)

Union Budget 2023–24 (February 2023)

Corpus infusion of ₹9,000 crore announced to revitalise CGTMSE, enabling additional guaranteed credit of ₹2 lakh crore

Guarantee limit enhanced to ₹2 crore (later progressively raised)

Reduced cost of credit through fee reduction for micro enterprises

CGTMSE Revisions — April 2023 onwards

Retail trade formally included for guarantee coverage up to ₹1 crore (major expansion from earlier service-only coverage)

Introduction of sub-schemes targeting women entrepreneurs, SC/ST, startups, and aspirational districts with enhanced coverage

Digital MLI onboarding and API-based guarantee registration introduced to speed up turnaround

2024 Revisions

Loan limit enhanced to ₹5 crore per borrower (from the earlier ₹2 crore cap), bringing larger working capital and expansion loans under the scheme’s ambit7

ZED (Zero Defect Zero Effect) certified MSMEs offered differential (better) guarantee coverage

DPIIT-recognised startups received dedicated CGTMSE coverage track

Union Budget 2025–26 (February 2025)

Limit Enhancement: The general CGTMSE credit guarantee cover limit was officially doubled from ₹5 crore to ₹10 crore. The government projects this will unlock an additional ₹1.5 lakh crore in MSME credit over the next five years.

Expanded MSME Definition: To bring more businesses under the scheme’s umbrella, MSME classification thresholds were drastically widened. Investment limits were increased by 2.5x and turnover limits were doubled (e.g., a Micro Enterprise can now have up to ₹2.5 crore in investment and ₹10 crore in turnover).

Supercharged Covers for Startups & Exporters: The guarantee cover limit for DPIIT-recognised startups was doubled from ₹10 crore to ₹20 crore (with a moderated 1% fee for 27 priority sectors). Well-managed exporting MSMEs also received a dedicated term loan guarantee cover up to ₹20 crore.

Micro-Enterprise Credit Card: A new customised, guarantee-backed credit card was announced, offering a seamless ₹5 lakh working capital limit for micro-enterprises registered on the Udyam portal.

Manufacturing Mega-Loans (MCGS): While separate from the core CGTMSE, the budget heavily promoted the newly approved Mutual Credit Guarantee Scheme (MCGS). This provides 60% guarantee coverage on massive term loans up to ₹100 crore for manufacturing MSMEs purchasing plant, machinery, and equipment.

⚠️ Note: Policy announcements in budgets take time to be operationalised by CGTMSE. Always confirm the effective date of any revision with your bank and on the official CGTMSE circular archive at www.cgtmse.in/Scheme/Circulars.

Real-World Success Stories

Case 1: From Rejection to ₹35 Lakh — Textile Trader, Surat

Details anonymised

A first-generation entrepreneur running a fabric trading business in Surat had been rejected twice by two nationalised banks for a ₹35 lakh working capital loan—both times for “lack of collateral.” His GST turnover was ₹1.8 crore per year. After learning about CGTMSE from his CA, he approached a Small Finance Bank that was aggressively growing its MSME book. Within 28 days of application, the loan was sanctioned under CGTMSE coverage at 12.5% interest. Today, his turnover is ₹4.2 crore and he has successfully renewed the facility twice.

Key lesson: PSU banks aren’t always the best first option. SFBs and progressive private banks often have faster CGTMSE processes and more MSME-friendly appraisal teams.

Case 2: Women Entrepreneur, Food Processing Unit, Nashik

Details anonymised

A woman entrepreneur set up a dehydrated vegetable processing unit with a machinery requirement of ₹18 lakh. She had no land to mortgage. Under the CGTMSE scheme’s enhanced 85% cover for women borrowers (Micro category), her bank’s risk was effectively only ₹2.7 lakh on a ₹18 lakh loan. The loan was sanctioned in 21 days against a project report and confirmed buyer (a large spice company). She also received a 25% capital subsidy under PMEGP, making the effective loan outgo minimal.

Key lesson: Stack CGTMSE with capital subsidy schemes like PMEGP or CLCSS wherever applicable. The combination can dramatically reduce your real borrowing cost.

Case 3: IT Services Startup, Hyderabad

Details anonymised

A two-year-old DPIIT-recognised startup providing SaaS-based inventory management to retailers needed ₹50 lakh for product development and sales team expansion. With no physical assets and a lean balance sheet, traditional banks were uninterested. Through a fintech NBFC registered as a CGTMSE MLI, the startup secured the loan under the startup sub-scheme at 85% coverage. The founders retained equity, avoided ESOP dilution, and achieved product-market fit within 14 months.

Key lesson: CGTMSE-linked NBFCs and fintech lenders are increasingly competitive for startup-stage loans. Don’t limit your search to PSU banks.

Common Myths vs Facts

MythFact“CGTMSE is a loan, not a guarantee”CGTMSE provides a guarantee to banks—it does not lend money directly to MSMEs.“I apply directly to CGTMSE for the loan”You apply to a registered MLI (bank/NBFC). The MLI evaluates and registers the guarantee with CGTMSE.“CGTMSE cover means I don’t need to repay if my business fails”You are always liable to repay. CGTMSE compensates the bank; it then has subrogation rights against you, and your CIBIL will be impacted.“Any bank will give me a loan just because CGTMSE exists”Banks still appraise your creditworthiness. CGTMSE reduces their risk but doesn’t eliminate bank discretion or basic financial checks.“CGTMSE is only for manufacturing units”Services and retail/wholesale trade are also fully covered. Since the 2025 revisions, retail trade has been brought completely at par with manufacturing up to the full scheme limit.“The loan limit is ₹2 crore (or ₹5 crore)”As of the April 2025 revisions following the Union Budget, the maximum limit has been enhanced to ₹10 crore per borrower.“Only PSU banks offer CGTMSE loans”SFBs, private banks, and eligible NBFCs that are registered MLIs also actively offer CGTMSE-backed loans.“No documents needed—it’s collateral-free”Collateral-free ≠ document-free. Financial statements, ITR, GST returns, and a valid Udyam registration are mandatory to prove viability.“The CGTMSE fee is paid only once”The Annual Guarantee Fee (AGF) is charged every year the loan is active (typically on the outstanding amount after year one).“A rejected CGTMSE application can’t be reapplied”You can absolutely reapply after addressing the financial deficiencies cited by the MLI—there is no CGTMSE-level blacklist for reapplication.

Frequently Asked Questions

1. What is the maximum loan I can get under CGTMSE in 2026? The maximum credit facility covered under the general CGTMSE scheme is ₹10 crore per borrower (per enterprise), as revised in April 2025 following the Union Budget. This covers term loans, working capital, and composite facilities. Verify the current cap on www.cgtmse.in.

2. Can I get a CGTMSE loan if I already have a home loan or car loan? Yes. Existing personal loans (home loan, vehicle loan) do not disqualify you. However, if you have any business loan that is NPA, you are not eligible for CGTMSE coverage on a new facility.

3. Does CGTMSE cover loans from NBFCs? Yes, select NBFCs registered as MLIs with CGTMSE can offer guaranteed loans. Check the MLI list on the official CGTMSE portal.

4. What is the interest rate on a CGTMSE loan? CGTMSE does not regulate interest rates—each MLI sets its own rate. Rates typically range from 10% to 15% p.a. for MSME loans, depending on the borrower’s credit profile and the lender’s policy. The CGTMSE guarantee fee is charged separately over and above the interest rate.

5. Can a startup apply for a CGTMSE loan? Yes, if it holds a valid Udyam Registration and is DPIIT-recognised. The startup sub-scheme under CGTMSE offers 85% coverage up to ₹10 crore. (Note: Startups needing larger capital can also explore the separate CGSS scheme, which covers up to ₹20 crore). However, banks still rigorously assess repayment capacity and business viability.

6. My bank says CGTMSE is not applicable for my loan. What can I do? First, confirm your Udyam registration is valid and your enterprise is classified as Micro or Small. If you believe the bank is wrong, you can contact the bank’s MSME Nodal Officer, escalate to the Zonal/Regional Office, or approach SIDBI’s Udyam Mitra portal for grievance redressal.

7. How long does it take to get a CGTMSE-backed loan? Turnaround time depends on the MLI, loan amount, and document quality. Typically: 15–45 days from complete application submission for loans up to ₹50 lakh. Larger loans may take 45–90 days. Digital-first lenders and SFBs often have faster TATs.

8. What happens if my bank fails or merges—does the CGTMSE guarantee still hold? Yes. CGTMSE guarantees are registered with the Trust and remain valid regardless of MLI mergers, provided the AGF has been paid and the guarantee is current.

9. Can I prepay a CGTMSE loan without penalty? Prepayment terms are set by the MLI, not CGTMSE. Under RBI guidelines, there is generally no prepayment penalty on floating rate MSME loans. Check your loan sanction letter for the specific terms.

10. Is there a CGTMSE scheme for SC/ST entrepreneurs specifically? Yes, the CGTMSE framework provides enhanced 85% coverage for SC/ST borrowers across both Micro and Small categories. Some MLIs also combine this with National SC-ST Hub (NSSH) support and Stand-Up India scheme loans—explore these combinations.

11. What is the difference between CGTMSE and CGSS (Credit Guarantee Scheme for Startups)? CGSS is a separate SIDBI-managed guarantee fund specifically targeting DPIIT-recognised startups, offering enhanced coverage limits up to ₹20 crore. CGTMSE has integrated startup coverage within its own framework but caps out at ₹10 crore. Both can potentially be relevant—your MLI will advise which scheme best fits your specific funding and capital requirements.

12. How do I check if my loan has been registered under CGTMSE? Ask your bank to share the Credit Guarantee Number (CGN) issued by CGTMSE upon registration. You can also request confirmation through the bank’s written correspondence. CGTMSE does not currently have a public-facing borrower portal to check this independently (verify on cgtmse.in for latest features).

13. What if I’m denied a CGTMSE loan by multiple banks? First, get your CIBIL report (free once a year at cibil.com) and check for errors. Review whether your ITR, GST returns, and bank statements present a coherent financial story. Consider the Udyam Mitra portal (udyammitra.in) or SIDBI’s direct lending products if bank credit remains inaccessible.

14. Is GST registration mandatory for a CGTMSE loan? GST registration is mandatory if your turnover crosses the statutory threshold (₹40 lakh for goods, ₹20 lakh for services in most states). Below the threshold, it is not mandatory—but having voluntary GST registration significantly strengthens your loan application.

15. What is the validity period of a CGTMSE guarantee? The guarantee is valid for the tenure of the loan (subject to annual renewal by the MLI through payment of AGF). Once the loan is fully repaid and closed, the guarantee automatically terminates.

Conclusion & Next Steps

CGTMSE is not merely a scheme—it is a fundamental equaliser in India’s credit ecosystem. It places collateral-free credit within reach of the very businesses that drive employment, innovation, and economic resilience: your micro and small enterprise.

In 2026, with the enhanced ₹10 crore limit, full parity for retail and wholesale trade, digital processing, and highly targeted sub-schemes—such as the unprecedented 90% coverage for women entrepreneurs—the scheme has matured into a comprehensive credit guarantee architecture. The building blocks are in place. What you need to do is act.

Your immediate next steps:

Get your Udyam Registration if you haven’t already → udyamregistration.gov.in

Check the MLI list on www.cgtmse.in and identify 3–4 banks or NBFCs to approach

Prepare your documents: ITR (2 years), GST returns (12 months), bank statements (12 months), and a basic project report

Visit Udyam Mitra Portal (udyammitra.in) for handholding support in finding the right lender

Speak to your CA about aligning your financials before application to maximise your sanction probability

Explore complementary financing tools — If your business sells to large corporates or PSUs, consider TReDS (Trade Receivables Discounting System) alongside your CGTMSE loan. CGTMSE covers your capital expenditure and working capital limits; TReDS unlocks your receivables. Together, they eliminate both the collateral gap and the cash-flow gap.

The credit is out there. CGTMSE has made the guarantee available. Your job is to build a compelling, honest, and well-documented case. The rest follows.

Author Bio

I have spent over 11 years at the intersection of banking operations and MSME advisory—starting as a Probationary Officer at a nationalised bank where I personally processed hundreds of MSME loan files, and later moving into credit risk technology and policy advisory. I have conducted CGTMSE awareness workshops for bank staff and MSME clusters across Goa, Maharashtra, and Tamil Nadu, and have guided over 500 entrepreneurs through the process of securing their first collateral-free loan. My work today focuses on making complex financial instruments accessible and actionable for first-generation business owners across India. All views and guidance in this article are drawn from personal experience, official scheme documents, and publicly available regulatory sources.

Important Disclaimer

This article has been prepared for general informational and educational purposes only. While every effort has been made to ensure accuracy as of March 2026, the CGTMSE scheme, its limits, fee structures, eligibility criteria, and processes are subject to revision by CGTMSE, SIDBI, Ministry of MSME, and RBI. This article does not constitute financial, legal, or investment advice. Before making any borrowing decisions, always:

Verify current scheme details on the official CGTMSE website: www.cgtmse.in

Consult a qualified Chartered Accountant or financial advisor

Read your loan sanction terms carefully

The author and publisher accept no liability for any financial loss or adverse outcome arising from reliance on this article.

References & Official Sources

Additional Resources:

Udyam Registration Portal: udyamregistration.gov.in

Udyam Mitra (SIDBI MSME Loan Portal): udyammitra.in

SIDBI Official Website: www.sidbi.in

Ministry of MSME: msme.gov.in

RBI MSME Guidelines: rbi.org.in

CIBIL Free Credit Report: cibil.com

Read About

Government Schemes: MSME & Commercial Credit

Sovereign guarantee schemes, refinance programs, and credit facilitation tools for MSME and commercial lending -- critical for PSL compliance and risk mitigation.

- Empowering Entrepreneurs: How Mudra Bank is Revolutionizing Small Business Financing

- Mudra Loan vs Bank Loan: Which is Better for MSMEs?

- PMEGP – Prime Minister Employment Generation Program – Complete Revised Guidelines

- What is TReDS? How MSME Invoice Discounting Works

- Stand-Up India Scheme: Complete Guide for SC/ST & Women Entrepreneurs

Discussion

Sign in to join the discussion.

No comments yet. Be the first to share your thoughts.

Related Articles

About Bankopedia

Bankopedia is India's trusted knowledge platform for banking professionals — offering in-depth guides on RBI regulations, banking exams, fintech, and financial analysis.