These are not coincidences. They are signals. And the message they send to every banker who has never written a line of code is uncomfortable but clear: the industry has moved, and the skills that made you competitive a decade ago are no longer sufficient.

You Cannot Manage What You Cannot Understand

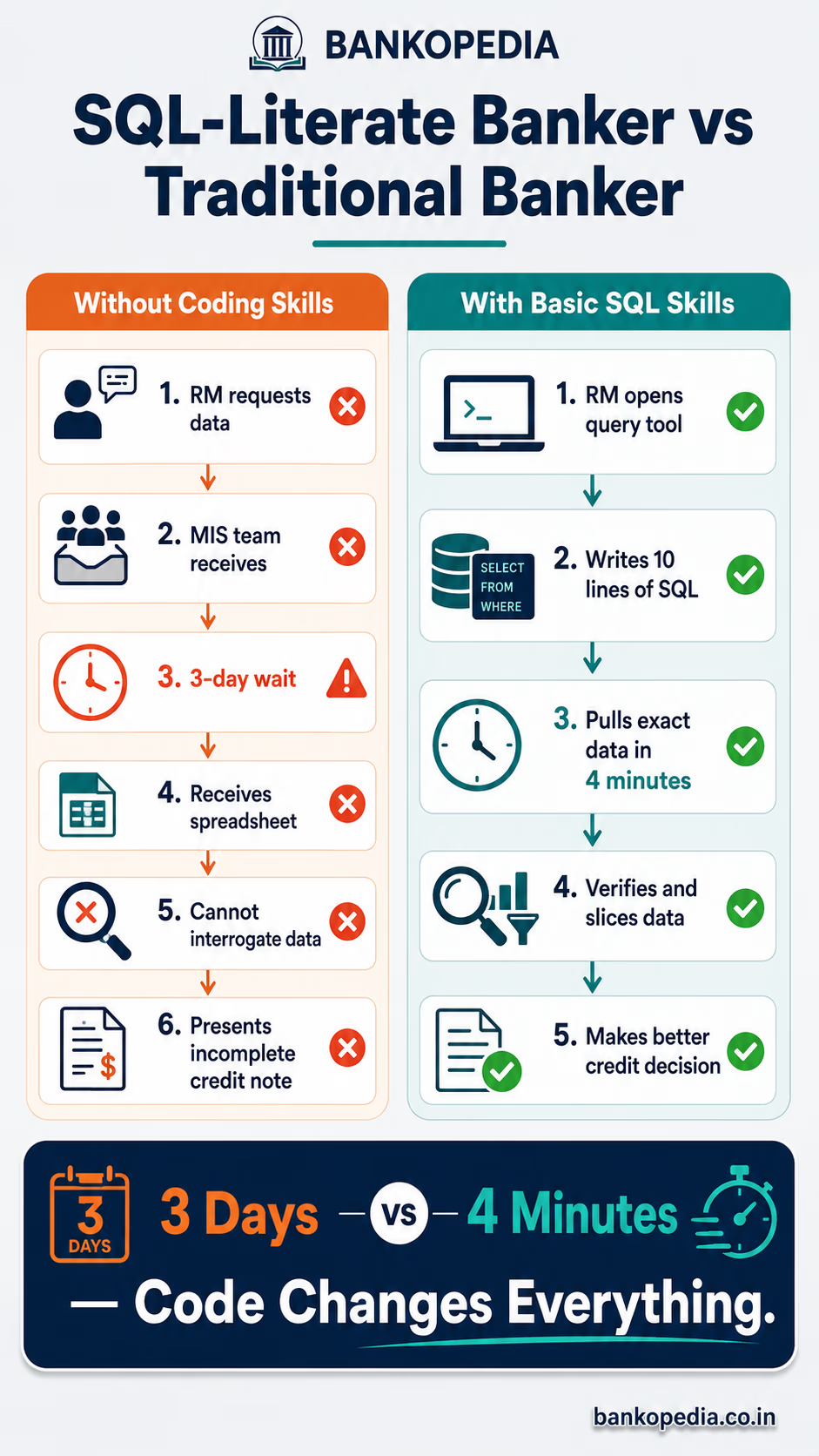

Here is a concrete scenario that plays out every day in Indian banking. A Relationship Manager needs a customer's transaction pattern over the last 18 months to prepare a credit note. She sends a request to MIS. Three days later, she gets a spreadsheet. She cannot interrogate it, cannot change the date range, cannot add a column. She presents the credit note using data she does not fully understand, prepared by a team whose methodology she has never seen.

Now imagine the same RM who knows basic SQL. She opens a query tool, writes ten lines, and pulls exactly what she needs in four minutes. She can see the raw data. She can verify it. She can slice it differently if the credit committee asks a follow-up question. She has turned a three-day dependency into a four-minute task — and more importantly, she has made a better credit decision because she actually understood the data behind it.

This is not a hypothetical. It is the daily reality of data-literate bankers in every progressive institution. The principle applies across roles: a risk analyst who cannot read a Python script cannot audit the model scoring his portfolio. A product manager who does not understand APIs cannot meaningfully brief the engineering team building the next version of her app. A branch manager who does not understand how digital journeys are tracked cannot improve them. Comprehension drives influence, and influence drives career progression.

Automation Is Coming for Your Workflow — Not Your Seat

The popular fear is that programming will make bankers redundant. The reality is precisely the opposite. Bankers who understand programming will be the ones deciding which workflows get automated, how they get automated, and whether the output can be trusted.

Loan processing, KYC verification, EMI reconciliation, interest calculation, regulatory reporting, exception flagging — all of this is being automated at an accelerating pace. Robotic Process Automation (RPA) tools are already handling enormous volumes of back-office work that used to require teams of clerks. GenAI tools are drafting credit memos, summarising borrower financials, and flagging covenant breaches in real time.

The banker who understands the logic behind these processes and can communicate that logic to a machine — or to the developer building the tool — shapes the outcome. The banker who cannot is handed the output of someone else's decisions and asked to sign off on it. One of these roles has institutional power. The other does not.

Beyond job security, there is a productivity argument. A banker who can write a Python script to automate her monthly reporting saves roughly two to three days per month. Over a year, that is nearly a month of working time reclaimed. Compounded across a team, the impact on throughput is enormous. The banks that figure this out first — by building armies of citizen developers among their banking staff — will have a structural cost and speed advantage that is very difficult to replicate.

RegTech and FinTech Now Speak in Code

SEBI mandates, RBI guidelines, Basel III compliance frameworks, FATF recommendations — all of these are increasingly delivered as structured data standards, API specifications, and automated reporting pipelines. The era of printing regulatory returns and submitting them manually ended years ago. The era of understanding what those automated pipelines actually do is just beginning.

RBI's Account Aggregator framework is a pure technology construct — a consent-based data-sharing architecture built on APIs. If you are a banker who does not understand what an API is, you cannot meaningfully participate in building products on top of Account Aggregator. You are dependent on someone else's interpretation of a regulatory framework that directly affects your customers.

FinTech partnerships now run on webhooks, sandbox environments, and technical due diligence exercises, not just MoUs and relationship meetings. When a FinTech wants to embed lending into a platform, the negotiation is as much about data schemas and latency requirements as it is about commercial terms. A banker who cannot participate in that conversation at a technical level is leaving the most important decisions to be made by people whose primary loyalty is not to the bank's risk framework.

This is not an argument for bankers becoming engineers. It is an argument for bankers having enough technical literacy to be credible counterparties in technical negotiations. You do not need to build the API. You need to understand what you are agreeing to when you sign the integration agreement.

AI Tools Already Reward the Programmatically Literate

ChatGPT, Microsoft Copilot, Claude, Gemini — these tools are already embedded into bank workflows, internal productivity suites, document review pipelines, and customer service systems. But the gap between how a programmatically literate banker uses these tools and how an average banker uses them is enormous.

An average user types a question and accepts the first answer. A programmatically literate user writes a structured prompt with clear input specifications, output format requirements, constraint definitions, and example outputs. The first gets a paragraph of generic text. The second gets exactly what she needs, formatted the way she needs it, with the caveats she asked for.

More importantly, a banker who can write even basic Python can automate entire workflows using AI APIs. She can pull a batch of customer complaints from a database, send each one to an AI model for classification, aggregate the results, and load them into a dashboard — automatically, overnight, every night. That is not a technology team project. That is one banker with three hundred lines of Python doing what a five-person team used to do manually over a week.

The productivity multiplier from combining banking domain expertise with basic programming skills and modern AI tools is genuinely extraordinary. The bankers who access that multiplier in the next five years will compound their output — and their careers — at a pace that their peers will find very difficult to explain.

Credit, Risk, and Treasury Are Quantitative Disciplines — It Is Time to Treat Them That Way

Credit underwriting has always been quantitative. Risk management is built on probability theory, correlation matrices, and stress testing. Treasury operations run on yield curves, duration matching, convexity calculations, and derivative pricing models. These are not soft skills dressed up in spreadsheets. They are applied mathematics, and banking is one of the largest employers of quantitative thinking in the world.

But most bankers in these roles work through proxies. They use spreadsheets handed down from predecessors, models they did not build, dashboards they cannot interrogate, and reports they did not design. When the model gives a counterintuitive answer, they often cannot determine whether it is wrong or whether they are. That uncertainty is not just intellectually uncomfortable — it is a source of risk.

Python has become the default language of quantitative finance. Libraries like pandas, NumPy, scipy, statsmodels, and sklearn are used daily by credit risk teams, ALM desks, and treasury functions at every major institution. You do not need to become a quant to benefit from understanding this ecosystem. But understanding how a logistic regression model works — what its inputs are, what assumptions it makes, what it cannot capture — will make you a dramatically better credit analyst than one who treats the model as a black box.

The same applies to market risk. A treasury dealer who understands how a Value at Risk model is constructed can challenge it intelligently when it gives an implausible result during a stress event. One who cannot is dependent on the risk team's interpretation, which may itself be unreliable. The ability to go one level deeper — to see the mechanism, not just the output — is what separates the practitioner from the technician.

The Data Advantage in Relationship Banking

One of the counterintuitive benefits of programming literacy for bankers is what it does for relationship management — traditionally the most human part of the job. A Relationship Manager who can pull and analyse her own data about a client's account behaviour, payment history, and product usage is simply a better RM than one who cannot. She walks into client meetings knowing things the client sometimes does not know about themselves.

Cross-selling becomes more intelligent when it is driven by behavioural data rather than intuition. Retention calls become more timely when the RM can identify early warning signals in transaction patterns rather than waiting for the quarterly review. Client conversations become more substantive when the RM arrives with analysis, not just pleasantries.

Banks are sitting on some of the richest customer datasets in the world. Every transaction, every product interaction, every call centre touchpoint, every digital journey — all of it is logged. The bankers who can access and interpret that data are playing a fundamentally different game than those who cannot. And right now, the ability to access that data yourself, without waiting for a team to process it for you, is almost entirely determined by whether you know SQL.

What "Learning to Code" Actually Means for a Banker

The most common objection from bankers is that they are not tech people. This objection misunderstands what learning to code means in a banking context. You do not need to become a software engineer. You do not need to understand operating systems, memory management, or distributed systems architecture. The bar is much lower and much more practical.

SQL basics (2–3 weeks): Pull your own data; stop waiting on MIS; verify reports independently. Within two weeks you will be writing queries that answer most of the questions you currently wait three days to get answered.

Python fundamentals (4–6 weeks): Automate repetitive Excel work; process large datasets; build simple tools. Focus on reading, cleaning, and reshaping data — not software engineering.

pandas and data analysis (3–4 weeks): Replace 80% of your complex Excel use cases with reproducible, auditable scripts that run in seconds on any dataset size.

API literacy (1–2 weeks): Understand what an API call does, what a JSON response looks like, and how integration agreements translate to technical requirements. You will never sign a FinTech contract the same way again.

Prompt engineering (1 week): Learn to write structured prompts that extract consistent, formatted, reliable output from AI models. This alone will save you hours every week.

Basic data visualisation (2 weeks): Build dashboards and charts that tell a story rather than dump numbers. The ability to present your own analysis visually is an enormous professional advantage.

A committed 90-day evening programme covering these areas will permanently change how you work. The investment is roughly 45 to 60 hours of focused learning. The return on that investment, measured in hours saved and decisions improved, is typically realised within the first three months after completion.

A Practical 90-Day Roadmap

Month 1 — SQL. Start with Mode Analytics' free SQL tutorial or Khan Academy's SQL track. Within the first week you will be writing SELECT queries. By the end of the month you will be joining tables, filtering, grouping, and aggregating — covering 90% of what you will ever need as a banker. Practice on real data: download public RBI datasets, SEBI disclosure files, or your bank's sandbox data if available.

Month 2 — Python and pandas. Work through the first four chapters of Python for Data Analysis by Wes McKinney — the creator of pandas. Focus on reading data files, cleaning messy inputs, slicing and filtering dataframes, and summarising with groupby. Do not get distracted by object-oriented programming, decorators, or advanced Python features you do not need yet. The data manipulation layer is what matters for your purposes.

Month 3 — One real automation project. Take something you do manually every month — a report, a reconciliation, a rate comparison, an exception tracker — and automate it completely in Python. This is where the learning solidifies into a permanent skill. The act of solving a real problem forces you to encounter real obstacles and develop the problem-solving instinct that separates people who actually use code from people who took a course and forgot it.

Optional Month 4 — AI API integration. Once you are comfortable with Python, spend a few weeks learning to call AI APIs. Anthropic's Claude API, OpenAI's GPT API, and Google's Gemini API all have free tiers and excellent documentation. Build a small tool that takes a piece of financial text — a balance sheet narrative, a news article about a borrower, a customer complaint — and classifies or summarises it automatically. You will have built something more sophisticated than many banks' AI pilots, and you will understand exactly how it works.

What the Best Banks Are Already Doing

JPMorgan Chase introduced mandatory coding training for its analysts in 2018, framing it as a career development requirement rather than an optional elective. Goldman Sachs built its own internal programming curriculum with modules specifically designed for non-engineers in banking and markets roles. Morgan Stanley deployed Python notebooks across its investment banking teams to standardise financial modelling workflows. HSBC runs a Digital Upskilling programme that has trained over 100,000 employees in data literacy and basic programming concepts.

In India, HDFC Bank's internal technology academy has trained thousands of banking staff in data analysis tools. Kotak Mahindra Bank has made data literacy a criterion for promotion in certain management roles. ICICI Bank's iAspire leadership pipeline includes technology modules as mandatory components. These are not charity initiatives or CSR projects. They are talent strategies built on a clear-eyed understanding of what skills will determine which banks — and which bankers — are competitive in the decade ahead. The signal from institutional behaviour is unambiguous.

The Career Case Is Overwhelming

Bankers who combine deep domain expertise with programming literacy are genuinely rare. There are plenty of excellent credit analysts. There are plenty of excellent developers. But the banker who can do both — who understands the regulatory environment, the customer relationship, and the credit framework, and who can also build the tool to automate the underwriting, pull the data to challenge the model, or interrogate the API specification in a FinTech negotiation — is in a category that commands significantly higher compensation and significantly greater institutional influence.

The compensation premium is real and growing. In a 2024 survey of mid-to-senior banking professionals across Indian private sector banks, those who self-reported proficiency in SQL and at least one programming language earned on average 22% more than peers at equivalent seniority levels who did not. The premium was highest in credit, risk, and product roles — exactly the areas where data literacy has the most direct operational impact.

As banking continues its structural shift toward technology-first delivery, this premium will only increase. The time to build the skill is not when the market has already priced it in and thousands of bankers are competing on the same credential. The time to build it is now, while it is still genuinely differentiating.

The Competitive Moat Has Changed — Here Is How to Build the New One

The competitive moat in banking used to be built on relationship networks, product knowledge, and institutional access. It still is, and it always will be. Those things still matter enormously. Relationships still win mandates. Domain expertise still drives trust. No amount of Python replaces the judgment that comes from twenty years of watching borrowers succeed and fail across economic cycles.

But the banker who adds programming literacy to that foundation is not replacing those advantages. She is compounding them. She brings the same relationships and domain knowledge, and she brings them faster, better-informed, and better-evidenced than the banker without the technical layer. She is playing the same game with a better set of tools, and in a competitive market, better tools win.

The learning curve is shorter than you think. The tools are more accessible than they have ever been. The resources — from free online courses to AI tutors that answer your questions in real time, in plain English, without judgment — have never been better. The only barrier between most bankers and this skill set is the decision to start.

Make that decision. Write your first SQL query this week. Find a public dataset — RBI's weekly statistical supplement, SEBI's monthly bulletin, your bank's published financial statements — and ask it a question. It will feel awkward and unfamiliar, and then suddenly it will feel like the most powerful thing you have done for your career in years.

That is the moment this article is trying to get you to.