Table of Contents

Introduction: Why Indian MSMEs Can’t Afford to Wait for Payments

For millions of Indian MSMEs, delayed payments are a silent crisis. An MSME supplier delivers goods or services, raises an invoice, and then waits — sometimes 60, 90, or even 120 days — before the buyer pays. Meanwhile, salaries, raw materials, and rent can’t wait.

Two financial instruments — factoring vs invoice discounting in India — directly address this cash-flow gap. Both convert unpaid invoices into immediate working capital. Yet they work very differently, carry different costs and risks, and suit different business situations. Choosing the wrong one can cost you more than the delay itself.

In 2026, with the Trade Receivables Discounting System (TReDS) maturing as a regulated marketplace and large corporates now mandated to onboard as buyers, Indian MSMEs have more choices than ever. This guide explains each instrument clearly, compares them side by side, and helps you decide which option fits your business.

What Is Invoice Factoring in India?

Definition and Legal Framework

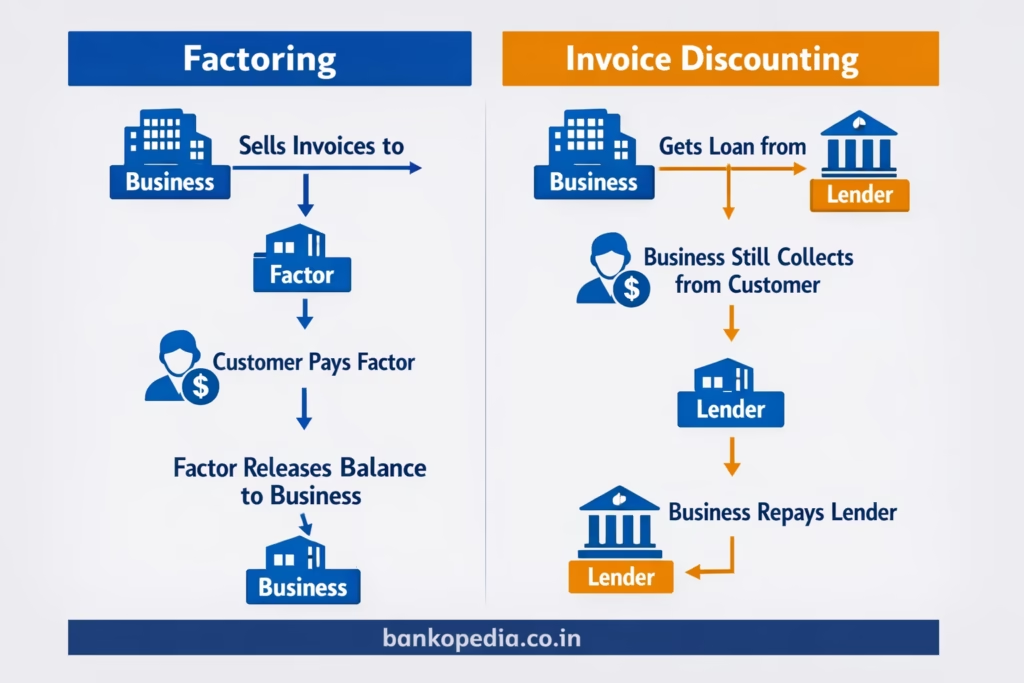

Invoice factoring is the outright sale of trade receivables (invoices) by a business (the assignor) to a registered factor (the assignee) in exchange for immediate funds. The factor then collects payment directly from the buyer (debtor).

In India, factoring is governed by the Factoring Regulation Act, 2011, amended by the Factoring Regulation (Amendment) Act, 2021 to significantly expand the number of entities that can operate as factors. Under the original Act, only banks, NBFCs registered with RBI as factors, and SIDBI could offer factoring services. The 2021 amendment allowed all eligible NBFCs to engage in factoring without a separate registration, improving access for MSMEs. (Source: Reserve Bank of India, 2022 — https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=12267)

How Traditional Factoring Works

- MSME raises an invoice on a buyer (debtor) for goods or services delivered.

- The MSME assigns the invoice to a registered Factor (a bank or NBFC Factor).

- The Factor advances a percentage of the invoice value to the MSME upfront. (source verification recommended for current advance rates from individual Factors)

- The Factor notifies the buyer that the debt has been assigned and payment must be made directly to the Factor — a key legal requirement under the Factoring Regulation Act, 2011.

- When the buyer pays on the due date, the Factor remits the remaining balance to the MSME, net of fees.

Recourse vs Non-Recourse Factoring

- Recourse factoring: If the buyer defaults, the MSME remains liable to refund the advance to the Factor. More common in India and generally cheaper.

- Non-recourse factoring: The Factor absorbs the credit risk of buyer default. Less common and more expensive in India. (Source: SBI Factors and Commercial Services Pvt. Ltd., n.d. — https://www.sbifactors.in/products)

Notified vs Non-Notified Factoring

Under the Factoring Regulation Act, 2011 (as amended), the assignment of a receivable must be registered with CERSAI (Central Registry of Securitisation Asset Reconstruction and Security Interest) to create a legally enforceable interest. Factoring without CERSAI registration is referred to as “non-notified” and carries greater legal risk for the Factor. (Source: RBI Master Direction on Factoring, 2022 — https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=12267)

What Is Invoice Discounting in India?

Definition

Invoice discounting is a short-term borrowing arrangement where a business uses its unpaid invoices as collateral to obtain a loan or credit facility from a lender. Unlike factoring, the business retains ownership of the invoice and typically continues to manage collections from the buyer.

The key distinction: in discounting, the lender finances the invoice but the seller-customer relationship — including payment follow-up — remains with the MSME.

How Invoice Discounting Works

- MSME raises an invoice on a buyer.

- The MSME presents the invoice to a lender (bank, NBFC, or TReDS platform).

- The lender disburses funds against this security — a percentage of the invoice value.

- The buyer is often not notified (confidential discounting), preserving the MSME’s commercial relationship.

- On the due date, the MSME collects payment from the buyer and repays the lender.

The Role of TReDS Platforms in Invoice Discounting

The Trade Receivables Discounting System (TReDS) is a regulated electronic platform authorised by the Reserve Bank of India under the Payment and Settlement Systems Act, 2007. TReDS enables MSMEs to discount invoices raised on corporates and government entities through a transparent, competitive bidding process among multiple financiers.

Approved TReDS platforms in India as of 2026:

- RXIL (Receivables Exchange of India Ltd.) — a joint venture of NSE and SIDBI. (https://www.rxil.in)

- M1xchange — operated by Mynd Solutions. (https://www.m1xchange.com)

- Invoicemart — operated by A.TReDS Ltd., promoted by Axis Bank and mJunction. (https://www.invoicemart.com)

On TReDS, once an MSME uploads an invoice and the buyer approves it, multiple financiers bid competitively. The MSME receives funds — often within 24–48 hours of buyer approval — at the lowest bid rate. Because the buyer has pre-approved the invoice and will pay the financier directly on the due date, the MSME’s own credit risk is largely replaced by the buyer’s credit profile, often resulting in lower financing costs. (Source: RXIL, n.d. — https://www.rxil.in/how-it-works)

Key Differences: Factoring vs Invoice Discounting in India

| Parameter | Invoice Factoring | Invoice Discounting (incl. TReDS) |

|---|---|---|

| Ownership of Invoice | Transferred to Factor (full assignment/sale) | Remains with the MSME (used as collateral) |

| Buyer Notification | Mandatory — buyer notified to pay the Factor | Usually confidential; on TReDS the buyer approves but financier identity varies |

| Collections Responsibility | Factor collects from buyer | MSME collects from buyer; on TReDS, buyer pays financier directly |

| Cost Structure | Factoring fee (% of invoice) + interest; typically higher due to bundled services | Discount rate on advance; competitive on TReDS due to bidding |

| Confidentiality | Low — buyer knows the invoice has been assigned | High for traditional; TReDS involves buyer participation |

| Recourse on Default | Recourse or non-recourse options | Typically recourse in traditional; TReDS is without-recourse |

| Suitability for MSMEs | Useful for MSMEs with weak collections or new buyers | Ideal for established MSMEs with reliable large corporate buyers |

| Regulatory Framework | Factoring Regulation Act, 2011 (amended 2021); CERSAI registration required | RBI TReDS Guidelines (2014, updated); PSS Act, 2007 for TReDS |

| Key Eligibility | Relationship with registered Factor; buyer creditworthiness assessed | Udyam Registration for TReDS; buyer must be corporate or government entity |

| Speed of Funding | Typically 2–7 working days | 24–48 hours on TReDS after buyer approval |

| Balance-Sheet Treatment | Invoice derecognised (true sale) | Invoice remains on balance sheet; advance shown as short-term liability |

1")

Pros and Cons of Each Option

Invoice Factoring — Pros and Cons

Pros:

- Immediate cash without waiting for buyer payment cycles

- Factor takes over collections, saving MSME time and resources

- Non-recourse factoring protects against buyer default

- Factor evaluates buyer’s creditworthiness, helping MSMEs with limited credit history

- True sale cleans up the balance sheet

Cons:

- Buyer is notified, which can feel awkward in some commercial relationships

- Generally costlier than discounting due to bundled services

- Recourse factoring still exposes the MSME to buyer default risk

- Fewer registered Factors in India, especially outside metros

Invoice Discounting — Pros and Cons

Pros:

- Confidential in traditional form — buyer relationship undisturbed

- Lower cost on TReDS due to competitive bidding among multiple financiers

- Fast funding on TReDS (24–48 hours after buyer approval)

- On TReDS, MSME’s own credit profile is secondary — buyer’s creditworthiness drives the rate

- Government mandate requires large corporates to register on TReDS, expanding the buyer pool

Cons:

- MSME manages collections in traditional discounting; cash flow risk if buyer delays

- TReDS requires buyer to be registered and to actively approve invoices

- Not suitable if buyer is a small, unregistered entity

- In traditional discounting, balance sheet shows borrowing as a liability

Role of TReDS in India: A Game-Changer for MSME Financing

The Trade Receivables Discounting System (TReDS) has fundamentally changed how MSMEs access working capital against corporate invoices in India.

How TReDS Works (Step-by-Step)

- MSME uploads an invoice on RXIL, M1xchange, or Invoicemart after free registration.

- The corporate buyer logs in and approves the invoice (confirming delivery and amount).

- Multiple financiers registered on the platform bid competitively, offering discount rates. The MSME selects the best (lowest) rate.

- Funds are disbursed to the MSME’s bank account within 24–48 hours of accepting a bid.

- On the invoice due date, the corporate buyer pays the financier directly. The MSME has no repayment obligation — this is a without-recourse transaction on TReDS. (Source: RXIL, n.d. — https://www.rxil.in/msme)

Corporate Registration Mandate

The Ministry of Corporate Affairs and RBI have directed that companies and CPSEs above specified turnover thresholds must register on TReDS platforms as buyers. (Source verification recommended — refer to https://www.mca.gov.in for the latest circular on exact current thresholds.) This mandate has significantly increased the pool of large corporate buyers on TReDS, making it more accessible for their MSME suppliers.

Key Benefits for MSMEs on TReDS

- Without-recourse — MSME is not liable if the corporate buyer defaults

- No collateral required beyond the approved invoice

- Competitive rates — multiple financiers bidding drives down the discount rate

- Transparent and RBI-regulated — no hidden charges

- SIDBI participates as a financier on TReDS platforms, deepening available liquidity. (Source: SIDBI, n.d. — https://www.sidbi.in/en/products-and-services/treds)

When to Choose Factoring vs Invoice Discounting

[Insert Image Here: Decision-tree graphic tailored for Indian MSMEs — left branch: startup or MSME with multiple buyers and weak collections infrastructure → Traditional Factoring; right branch: established MSME supplier to large corporate registered on TReDS → TReDS Invoice Discounting. Alt text: ‘Which invoice finance option is best for your Indian MSME?’]

Choose Traditional Factoring If:

- You are a startup or early-stage MSME with limited collections infrastructure.

- You sell to multiple buyers of varying creditworthiness and need ongoing receivables management.

- You prefer non-recourse protection against buyer defaults, even at a higher cost.

- Your buyers are not registered on TReDS (e.g., SME-to-SME transactions or buyers below mandated thresholds).

- You want to clean up your balance sheet through a true sale of receivables.

Example: A ₹2 crore turnover garment MSME in Surat sells to 15 retail chains of varying sizes. None are on TReDS. A Factor takes over collections across all buyers, provides advance funds, and frees the owner to focus on production.

Choose TReDS Invoice Discounting If:

- You are an established MSME supplier to large corporates, PSUs, or government entities.

- Your corporate buyers are already registered on TReDS (or are mandated to be).

- You want the lowest possible cost — competitive bidding on TReDS results in rates driven by the buyer’s credit profile, not yours.

- You want fast, without-recourse financing with no collateral beyond the invoice.

- You are Udyam-registered, a prerequisite for onboarding as a seller on TReDS platforms.

Example: A precision auto-components manufacturer in Pune with ₹12 crore turnover supplies a large OEM (₹10,000 crore turnover, TReDS-registered). The OEM’s strong credit profile drives the discount rate — the MSME accesses funds at rates it could not command on its own creditworthiness alone.

Additional Considerations

RBI Regulations

Both factoring and TReDS-based discounting are regulated activities. Factors must comply with the Factoring Regulation Act, 2011, and TReDS platforms are authorised and monitored by the RBI under the Payment and Settlement Systems Act, 2007. Always verify that your Factor or TReDS platform has valid RBI authorisation. (Source: RBI — https://www.rbi.org.in)

GST and TDS Implications

- GST on fees: Factoring and financial services charges attract GST at 18% on the fee component. Ensure your agreement clearly defines the fee and GST treatment. (Source verification recommended — refer to CBIC at https://www.cbic.gov.in for current SAC codes.)

- TDS: In certain arrangements, TDS under Section 194A of the Income Tax Act may apply on interest-like charges. Consult your CA for advice specific to your transaction structure.

- Invoice accuracy for TReDS: The invoice uploaded on TReDS must reflect the correct GSTIN, invoice number, and HSN/SAC code. Mismatches can delay buyer approval.

Udyam Registration Advantage

Udyam Registration is a prerequisite for onboarding on TReDS platforms as an MSME seller. It also unlocks priority-sector lending benefits, lower interest rates under SIDBI schemes, and protection under the MSMED Act, 2006 for delayed payment recovery (the 45-day payment rule). Register at https://udyamregistration.gov.in.

Balance-Sheet Treatment

In traditional factoring (true sale), the receivable is derecognised from the MSME’s books, improving working capital ratios. In invoice discounting, the invoice remains on the balance sheet and the advance appears as short-term borrowing. Your CA can guide you on the appropriate treatment under Ind AS or IGAAP.

Credit Checks

- Factoring: The Factor primarily evaluates buyer creditworthiness. The MSME’s own credit history matters less in non-recourse arrangements.

- TReDS: Since the buyer pays the financier directly and the transaction is without-recourse, buyer approval is the primary gateway. This significantly benefits MSMEs with limited credit history.

Conclusion and Next Steps

Both factoring and invoice discounting are powerful tools for solving India’s MSME delayed-payment crisis. The right choice depends on your buyer profile, business maturity, need for confidentiality, and cost tolerance.

Quick decision guide:

- Selling to large corporates or PSUs registered on TReDS → Start with TReDS Invoice Discounting.

- Need collections support, or your buyers are not on TReDS → Explore Traditional Factoring with SBI Factors, Canbank Factors, or SIDBI.

- Many established MSMEs use both simultaneously for different buyer segments.

Actionable Next Steps:

- Register on Udyam: https://udyamregistration.gov.in (prerequisite for TReDS)

- Onboard on TReDS (free for MSMEs): RXIL — https://www.rxil.in | M1xchange — https://www.m1xchange.com | Invoicemart — https://www.invoicemart.com

- Ask your corporate buyers if they are registered on TReDS — if not, nudge them toward compliance with the MCA mandate.

- Contact a registered Factor for traditional factoring: SBI Factors (https://www.sbifactors.in) | SIDBI (https://www.sidbi.in)

- Consult your CA about GST, TDS, and balance-sheet treatment before signing any agreement.

Frequently Asked Questions (FAQ)

1. What is the main difference between factoring and invoice discounting in India? In factoring, the invoice is sold to the Factor who collects from the buyer. In invoice discounting, the invoice is used as collateral for a loan; the MSME retains ownership and manages collections. On TReDS, the buyer pre-approves the invoice and pays the financier directly on the due date.

2. Is TReDS the same as invoice discounting? TReDS is a platform that facilitates invoice discounting in a regulated, competitive-bidding environment. Traditional invoice discounting is a bilateral arrangement with a single lender. TReDS is generally cheaper and faster.

3. Who can use TReDS in India? MSMEs registered on Udyam can register as sellers. Buyers must be companies, CPSEs, or government departments. Financiers must be banks or NBFCs registered on the platform. (Source: RBI TReDS Guidelines — https://www.rbi.org.in)

4. Is invoice factoring regulated in India? Yes. Invoice factoring is governed by the Factoring Regulation Act, 2011 (amended 2021) and RBI’s Master Direction on Factoring. Factors must be RBI-regulated entities. (Source: RBI, 2022 — https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=12267)

5. What advance percentage can an MSME expect? Advance rates vary by platform, Factor, and buyer creditworthiness. On TReDS, the advance is essentially the full invoice value minus the agreed discount. In traditional factoring, rates vary by arrangement. (Source verification recommended — check current rates directly with individual Factors or TReDS platforms.)

6. Is TReDS invoice discounting without recourse? Yes. TReDS transactions are structured as without-recourse — the MSME is not liable if the corporate buyer defaults. This is a significant advantage over traditional recourse factoring. (Source: RXIL, n.d. — https://www.rxil.in)

7. Does GST apply on factoring fees? Factoring services attract GST at 18% on the service fee component. Verify current SAC codes and applicability with your CA or refer to CBIC at https://www.cbic.gov.in.

8. What is the 45-day payment rule for MSMEs? Under the MSMED Act, 2006 (Sections 15–16), buyers must pay MSME suppliers within 45 days of delivery (or within the agreed credit period, not exceeding 45 days). Non-payment entitles the MSME to compound interest at three times the RBI bank rate. Both factoring and TReDS help MSMEs avoid this wait entirely.

References

Reserve Bank of India. (2022). Master Directions — The Factoring Regulation Act, 2011: Notification. https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=12267

Reserve Bank of India. (2014, updated). Guidelines on Trade Receivables Discounting System (TReDS). https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=9222

Receivables Exchange of India Ltd. (RXIL). (n.d.). How TReDS works for MSMEs. https://www.rxil.in/how-it-works

Receivables Exchange of India Ltd. (RXIL). (n.d.). MSME onboarding on TReDS. https://www.rxil.in/msme

M1xchange. (n.d.). Trade Receivables Discounting System — M1xchange. https://www.m1xchange.com

Invoicemart. (n.d.). Invoice discounting for MSMEs — Invoicemart. https://www.invoicemart.com

SBI Factors and Commercial Services Pvt. Ltd. (n.d.). Factoring products and services. https://www.sbifactors.in/products

Small Industries Development Bank of India (SIDBI). (n.d.). TReDS — SIDBI as financier. https://www.sidbi.in/en/products-and-services/treds

Ministry of Corporate Affairs, Government of India. (n.d.). Notifications on TReDS mandatory registration. https://www.mca.gov.in (source verification recommended for exact current threshold circular)

Udyam Registration Portal, Government of India. (n.d.). Register your MSME. https://udyamregistration.gov.in

Central Board of Indirect Taxes and Customs (CBIC). (n.d.). GST on financial services. https://www.cbic.gov.in

Ministry of Micro, Small and Medium Enterprises, Government of India. (n.d.). MSMED Act, 2006 — Delayed payment provisions. https://msme.gov.in

This article is for informational purposes only and does not constitute financial or legal advice. Consult a qualified CA, financial advisor, or registered Factor/TReDS platform for advice specific to your business.

1 thought on “Factoring vs Invoice Discounting: Key Differences in India (2026 Guide)”