Introduction

Table of Contents

Every business needs fuel to run its daily operations — and for MSMEs (Micro, Small and Medium Enterprises), that fuel is working capital finance for MSMEs. Whether it’s buying raw materials before an order is confirmed, paying wages while waiting for a customer payment, or bridging the gap between dispatching goods and receiving payment, the need for short-term finance is constant and often urgent. Working capital finance for MSMEs is essential for ensuring liquidity and operational efficiency.

In my 10+ years of working directly with MSME borrowers — from textile manufacturers in Erode to auto-component suppliers in Pune — I have seen one pattern repeat itself: businesses with strong order books and good margins still struggle purely because of cash flow timing mismatches. This is not a sign of business failure; it’s the nature of trade credit in India.

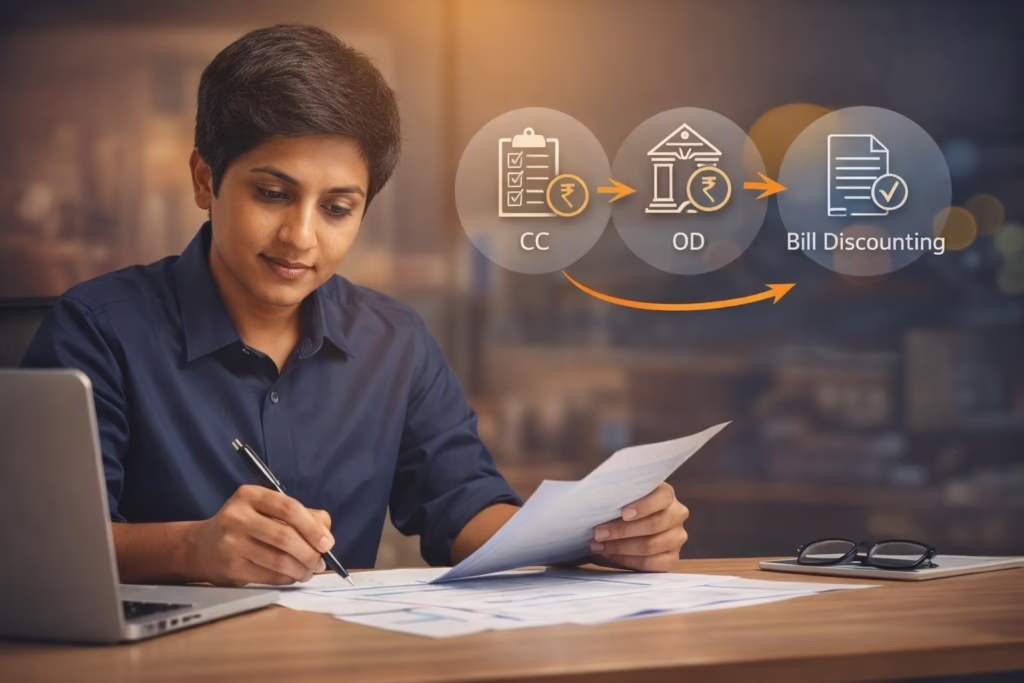

The Indian banking system offers three primary instruments to address this: Cash Credit (CC), Overdraft (OD), and Bill Discounting. Each has a distinct structure, purpose, and risk profile. Understanding these differences is not just academic — choosing the wrong facility can cost your business lakhs in unnecessary interest and limit your future credit appetite.

This article explains all three products in plain language, backed by RBI guidelines and standard banking practice as of 2025–2026, so you can make an informed decision.

Why MSMEs Need Working Capital Finance

The significance of working capital finance for MSMEs cannot be overstated, as it directly influences business stability and growth.

The role of working capital finance for MSMEs directly influences their capacity to manage cash flows and sustain growth amidst fluctuating demands.

Understanding how working capital finance for MSMEs operates helps owners make informed decisions that align with their financial needs.

Access to working capital finance for MSMEs is vital for addressing cash flow mismatches caused by delayed payments from buyers.

Many MSMEs rely on working capital finance for MSMEs to manage their cash flow effectively, especially in sectors with longer payment cycles.

The working capital cycle — also called the operating cycle — is the time between spending money to produce goods and receiving money from customers. For Indian MSMEs, this cycle often stretches 60 to 120 days or more, particularly in sectors like textiles, construction materials, pharmaceuticals, and engineering goods.¹

According to SIDBI’s MSME Pulse report, delayed payments from buyers remain the single largest stress factor for small businesses, with nearly 40% of MSME respondents citing receivables blockage as a key constraint.² The Micro, Small and Medium Enterprises Development (MSMED) Act, 2006, and subsequent RBI guidelines mandate that payments to MSME suppliers be made within 45 days,³ but enforcement remains uneven in practice.

Banks and NBFCs (Non-Banking Financial Companies) have developed working capital products specifically to bridge this gap. The three most widely used are:

- Cash Credit (CC): A revolving credit limit against stock and debtors.

- Overdraft (OD): A revolving credit limit typically against property or fixed deposits.

- Bill Discounting: A facility to convert trade receivables (invoices/bills) into immediate cash.

Cash Credit (CC) Account – How It Works

Utilizing working capital finance for MSMEs can provide the necessary liquidity for ongoing operations and growth initiatives.

A Cash Credit account is a running credit facility — meaning it works like a current account that can go into a negative balance up to a pre-sanctioned limit.⁴ The bank sanctions a CC limit based on your business’s working capital requirement, typically assessed through a method called the Turnover Method or the MPBF (Maximum Permissible Bank Finance) method, depending on the loan amount and bank policy.⁵

How the Limit Is Calculated

For limits up to ₹5 crore, banks commonly use the Nayak Committee Turnover Method, which allows CC finance up to 20% of the projected annual turnover.⁶ For larger limits, banks use detailed balance sheet analysis including:

- Current assets (stock + debtors + advances)

- Less: Current liabilities (creditors + other short-term payables)

- The resulting Net Working Capital (NWC) requirement is then funded at 75–80% by the bank, with the balance to be contributed by the borrower as margin.

Security and Drawing Power

The defining feature of a CC account is the concept of Drawing Power (DP). You can withdraw only up to the drawing power, which is calculated based on the value of eligible stock and debtors — not the full sanctioned limit. Banks require you to submit a monthly stock and debtors statement (also called Stock Statement or DP Statement) to recompute this figure.⁷

In my experience, many MSME owners are surprised to learn that their CC limit is ₹50 lakh, but they can only draw ₹32 lakh because their stock levels have dropped after a busy season. Understanding drawing power is critical to managing liquidity.

Interest and Charges

Interest is charged only on the amount actually utilised (the debit balance), not the full sanctioned limit. This makes CC cost-efficient compared to term loans for working capital purposes. Interest rates are typically benchmarked to EBLR (External Benchmark Lending Rate) or MCLR (Marginal Cost of Funds Based Lending Rate), plus a spread based on your credit risk profile.⁸ As of 2025, most public sector banks price CC facilities in the range of EBLR + 1% to EBLR + 3% for eligible MSMEs, though the actual rate varies with the borrower’s credit rating.

Primary Collateral

Interest rates on working capital finance for MSMEs can vary, largely depending on the financial health of the business and the banking relationship.

CC facilities are primarily secured by a hypothecation of stocks (raw material, work-in-progress, finished goods) and book debts (trade receivables).⁹ Banks also typically insist on a collateral security — usually a mortgage of property — unless the facility is covered under the CGTMSE (Credit Guarantee Fund Trust for Micro and Small Enterprises) scheme, which provides collateral-free coverage up to ₹5 crore.¹⁰

Overdraft (OD) Facility – How It Works

An Overdraft facility is structurally similar to Cash Credit — both allow you to withdraw more than what is available in your account, up to a pre-agreed limit, and interest is charged only on the amount used. The critical difference lies in the primary security and the basis for limit assessment.

While CC limits are primarily secured against current assets (stock and debtors), OD facilities are typically secured against:

- Fixed assets (mortgage of property — residential or commercial)

- Fixed Deposits (FD-backed OD — usually available up to 80–85% of FD value)

- Life Insurance policies or other liquid securities

- Book debts alone (in some bank-specific OD variants)

Because OD limits are assessed against the value of a specific asset rather than the business’s trading cycle, they do not require monthly stock statements or drawing power computation. This makes them simpler to operate.¹¹

Types of OD Facilities Relevant to MSMEs

- Property-backed OD (Dropline OD): The limit reduces progressively over time — similar to a term loan structure but with OD flexibility. Commonly used for business expansion or top-up needs.

- FD-backed OD: Instant sanction, minimal documentation. Best for MSMEs needing emergency liquidity without disturbing their FD.

- Current account OD: Extended by banks to established customers with good account conduct, based on average balance or account turnover.

In my experience, property-backed OD is frequently misused. I have advised many MSME owners who used OD against property to fund day-to-day working capital — only to find the limit insufficient and the interest cost high compared to a structured CC facility. OD against property is more appropriate for medium-term capital needs or when formal CC limits are not available.

Bill Discounting (Invoice/Bill Purchase) – How It Works

Bill Discounting — also known as Invoice Discounting or Bills Purchase — is fundamentally different from CC and OD. Rather than creating a running credit limit, it is a transaction-based facility where the bank purchases your trade receivable (an invoice or accepted bill of exchange) at a discount and gives you immediate cash.¹²

The Basic Mechanism

Here is the typical process:

- You supply goods/services to a buyer (your customer) and raise an invoice, say for ₹10 lakh, payable in 60 days.

- You present the invoice (or an accepted bill of exchange) to your bank.

- The bank advances approximately 80–90% of the invoice value immediately — say ₹8.5 lakh — after deducting a discount charge (the bank’s effective interest for 60 days).

- When the buyer pays on the due date, the bank recovers the full ₹10 lakh. The remaining amount (after adjusting the advance and charges) is credited to your account.

The discount rate applied is essentially the bank’s annualised interest rate for the credit period. This makes bill discounting particularly cost-effective when your invoice tenure is short (30–90 days) and your buyer has a good credit profile.

Key Variants

- Demand Bill Discounting: The buyer is required to pay on demand (sight). Less common in trade finance.

- Usance Bill Discounting: The bill is payable after a specified number of days (30, 60, 90 days). Most common in B2B trade.

- Invoice Discounting on TReDS (Trade Receivables Discounting System): RBI-regulated digital platforms (M1xchange, RXIL, Invoicemart) where MSME invoices are auctioned to multiple financiers competitively. MSMEs registered on TReDS often get lower discount rates.¹³

When Bill Discounting Is Ideal

Bill discounting is most effective when:

- You have large, creditworthy corporate buyers (PSUs, listed companies)

- Your receivables are concentrated in a few large invoices

- You want finance specifically tied to confirmed sales, not general-purpose credit

CC vs OD vs Bill Discounting – Comparison Table

| Parameter | Cash Credit (CC) | Overdraft (OD) | Bill Discounting |

|---|---|---|---|

| Nature | Revolving credit limit | Revolving credit limit | Transaction-based finance |

| Primary Security | Hypothecation of stock & debtors | Property / FD / liquid assets | Trade receivables (invoices/bills) |

| Basis of Limit | Working capital assessment (turnover/MPBF) | Asset value / banking relationship | Invoice value (case-by-case) |

| Interest Charged On | Actual daily debit balance | Actual daily debit balance | Discount deducted upfront |

| Drawing Power Concept | Yes — changes monthly with stock/debtors | No (fixed or dropline limit) | Not applicable |

| Collateral Required | Yes (or CGTMSE cover) | Yes (asset-backed) | Buyer creditworthiness |

| Monthly Stock Statements | Mandatory | Not required | Not required |

| Typical Tenure | Annual renewal | Annual / 3-year (dropline) | Per invoice (30–180 days) |

| Best For | Manufacturers, traders with inventory | Property owners needing flexible credit | Businesses with strong corporate buyers |

| Collateral-Free Option | Yes (via CGTMSE) | Rare | Yes (on TReDS platform) |

Which Facility Should Your MSME Choose? – A Decision Framework

Choosing the right facility depends on your business model, the nature of your working capital need, and the assets available to you. Here is a practical decision framework:

Choose Cash Credit if:

- You are a manufacturer or trader with significant stock holdings

- Your working capital cycle involves both inventory and receivables

- You want a revolving limit you can draw and repay freely

- You can provide collateral or qualify under CGTMSE

Choose Overdraft if:

- You own property or have liquid assets (FDs) to offer as security

- You need a flexible credit buffer for business emergencies or seasonal spikes

- You are in a service business with minimal inventory (where CC is not applicable)

- Your need is for general liquidity, not tied to specific invoices or stock

Choose Bill Discounting if:

- Your customers are large corporations, PSUs, or government bodies

- You have confirmed invoices with credit periods of 30–90 days

- You want finance specifically linked to your sales, not general credit

- You want to explore TReDS for potentially lower financing costs

Hypothetical example based on typical MSME scenarios: A textile manufacturer in Tiruppur with ₹3 crore annual turnover, supplying to domestic retail chains, would typically benefit from a CC facility of approximately ₹60 lakh (20% of turnover under Nayak methodology), supplemented by bill discounting against retail chain invoices for additional liquidity during peak festive season production cycles.

Step-by-Step Application Process & Documents Required

Step 1: Assess Your Requirement

Calculate your actual working capital gap — the difference between current assets required and current liabilities naturally available. Many MSME owners overestimate or underestimate this, leading to over-leveraging or under-utilisation.

Step 2: Select Your Bank/NBFC

Evaluate based on: pricing (EBLR/MCLR spread), processing fees, turnaround time, and CGTMSE empanelment if you need collateral-free access.

Step 3: Prepare Your Documentation

Standard documents required for CC/OD/Bill Discounting:

- Identity & Address Proof: PAN, Aadhaar, GST Registration Certificate

- Business Existence Proof: MSME Registration (Udyam Certificate), Partnership Deed / MOA-AOA (for companies)

- Financial Statements: Audited Balance Sheet and P&L for last 2–3 years; ITR acknowledgements

- Bank Statements: Last 12 months of current account statements (primary banker)

- Stock Statement / Debtors List: For CC — current stock and debtors details at the time of application

- Property Documents: For OD or collateral-backed CC — title deed, property valuation report

- Trade Documents: For Bill Discounting — copies of purchase orders, invoices, delivery challans

[Image Suggestion] Placement: After this paragraph Description: A document checklist infographic with icons for each document category: ID proof (Aadhaar/PAN icon), financial statements (balance sheet icon), bank statements (passbook icon), stock statement (clipboard icon), property papers (house icon). Checklist format with tick boxes. Clean, A4-style layout, suitable for printing. Purpose: Provides a quick visual reference for MSME owners preparing their loan application.

Step 4: Submit and Follow Up

Banks are required under RBI guidelines to communicate credit decisions on MSME loan applications within specific timelines — 2 weeks for loans up to ₹25 lakh under the MSME loan policy framework.¹⁴ If declined, you are entitled to a written communication specifying reasons, and you may request a review.

Step 5: Post-Sanction Compliance

After sanction, maintain discipline:

- Submit stock statements monthly (for CC).

- Ensure the CC/OD account shows regular credit turnover — dormant accounts attract regulatory scrutiny.

- Renew the facility annually with updated financials.

Common Pitfalls & How to Avoid Them

In my experience, the following mistakes consistently reduce MSME borrowers’ credit access and increase their cost of funds:

1. Over-stating stock or debtors in statements: Banks verify through concurrent audits and GST data reconciliation. False stock statements can lead to NPA classification and legal action.

2. Treating CC as a term loan: Withdrawing the full CC limit on day one and not rotating it defeats the purpose of a revolving facility. Banks view continuously maxed-out CC limits as a stress signal.

3. Ignoring the annual renewal: CC and OD facilities must be renewed each year. Failure to submit renewal documents on time leads to irregularity classification, which affects your credit score with CIBIL.¹⁵

4. Not exploring CGTMSE: Many eligible MSMEs — particularly in the ₹10 lakh to ₹2 crore range — pay for collateral or get rejected when they could have accessed credit through CGTMSE coverage. As of 2024–25, CGTMSE provides guarantee cover up to ₹5 crore for MSE borrowers.¹⁰

5. Ignoring TReDS for bill discounting: If your buyers are listed companies or PSUs, TReDS registration (it’s free for MSMEs) can significantly reduce your bill discounting cost through competitive bidding by multiple financiers.

Conclusion

Working capital finance is not a one-size-fits-all solution. Cash Credit works best for businesses with physical inventory; Overdraft offers flexibility against assets; Bill Discounting unlocks the value of confirmed trade receivables. The right choice depends on your business model, buyer profile, asset base, and cash flow pattern.

Understanding these products deeply — not just at the surface level — is what separates MSMEs that scale efficiently from those that remain perpetually stressed about cash flow. I have seen businesses transform their growth trajectory simply by switching from an OD against property to a properly structured CC facility aligned with their inventory cycle.

Take the time to discuss your specific situation with your bank’s MSME relationship manager or an independent financial consultant. Compare offers from at least two banks. And most importantly, maintain accurate books and timely filings — because in today’s data-driven credit environment, your GST returns and banking conduct are your most powerful credit credentials.

Frequently Asked Questions

Q1. Can an MSME have both a CC account and an OD facility simultaneously? Yes. Many MSMEs maintain a CC account for working capital against stock and a separate OD against property for emergencies or capital expenditure buffers. Banks assess the combined exposure against the borrower’s repayment capacity and collateral.

Q2. Is bill discounting available to MSMEs without any collateral? Yes, particularly through the TReDS platform, where the finance is backed by the buyer’s creditworthiness rather than MSME assets. Banks may also offer clean bill discounting to MSMEs with strong track records and corporate buyer relationships.

Q3. What is the CGTMSE scheme and who is eligible? CGTMSE (Credit Guarantee Fund Trust for Micro and Small Enterprises), jointly promoted by the Government of India and SIDBI, provides collateral-free credit guarantees to banks for lending to Micro and Small Enterprises up to ₹5 crore. Eligible borrowers include manufacturing and service MSEs with Udyam registration.¹⁰

Q4. How often must I submit stock statements for my CC account? Typically monthly. Most banks require a stock and debtors statement by the 7th or 10th of each month for the previous month’s closing figures. Non-submission leads to reduction of drawing power and may attract penal charges.

Q5. What happens if my CC account remains overdrawn beyond the drawing power? The account is classified as “irregular.” Prolonged irregularity — typically beyond 90 days — can lead to NPA classification under RBI prudential norms.⁷ This severely impacts your credit score and future borrowing ability.

Q6. What is the typical processing time for a CC or OD facility? For facilities up to ₹25 lakh, RBI guidelines encourage disposal within 2 weeks of complete documentation. For larger limits, the process typically takes 4–8 weeks, including property valuation, credit appraisal, and sanction committee approval.

Q7. Can a startup MSME with less than one year of financials get a CC facility? It is difficult to secure a bank CC facility with less than 2 years of audited financials. However, SIDBI and certain NBFCs offer working capital products for newer MSMEs based on GST returns, bank account statements, and projected turnover — particularly under government-backed schemes like the Emergency Credit Line Guarantee Scheme (ECLGS) successor programmes.

Q8. What is the difference between invoice discounting and factoring? Both involve converting receivables to cash, but in factoring the financier also manages collections from your buyers and the buyer is notified. In invoice/bill discounting, collections are typically managed by the MSME, and the buyer may not always be notified. Factoring is more suitable for businesses with high-volume, small-ticket receivables.

References

- Reserve Bank of India – Priority Sector Lending Guidelines: https://www.rbi.org.in/Scripts/BS_ViewMasCirculardetails.aspx?id=12256

- SIDBI MSME Pulse Report (latest edition): https://www.sidbi.in/en/msme-pulse

- Ministry of MSME – MSMED Act, 2006 (Section 16, delayed payment provisions): https://msme.gov.in/sites/default/files/msmedo/msmed-act2006.pdf

- RBI Master Direction – Loans and Advances – Statutory and Other Restrictions: https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=10296

- RBI Report of the Working Group on Flow of Credit to SSI Sector (Nayak Committee): https://www.rbi.org.in/scripts/PublicationReportDetails.aspx?ID=166

- IBA (Indian Banks’ Association) Guidelines on Working Capital Finance: https://www.iba.org.in

- RBI – Income Recognition, Asset Classification and Provisioning (IRACP) Norms Master Circular: https://www.rbi.org.in/Scripts/BS_ViewMasCirculardetails.aspx?id=12278

- RBI – External Benchmark Based Lending Rate (EBLR) Guidelines: https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=48131

- Indian Contract Act, 1872 – Hypothecation (as applicable to secured lending under SARFAESI): https://legislative.gov.in/sites/default/files/A1872-09.pdf

- CGTMSE – Scheme Details and Eligibility: https://www.cgtmse.in/Schemes

- RBI – Master Circular on Loans & Advances to Priority Sectors: https://www.rbi.org.in/Scripts/BS_ViewMasCirculardetails.aspx?id=12256

- RBI – Guidelines on Trade Receivables Discounting System (TReDS): https://www.rbi.org.in/Scripts/BS_ViewMasCirculardetails.aspx?id=10099

- TReDS Platforms (RBI-authorised): M1xchange – https://www.m1xchange.com; RXIL – https://rxil.in; Invoicemart – https://www.invoicemart.com

- RBI – MSME Credit Framework and Timelines: https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52288

- TransUnion CIBIL – Understanding MSME Credit Reports: https://www.cibil.com/business-credit-report

Written by Prashant, Risk Data Engineer at an Investment Banking with 10+ years of hands-on banking experience spanning MSME credit, retail credit, KYC/AML operations, and branch management. He holds an Executive Diploma in Applied Financial Risk Management from IIM Kashipur and is a CFA Institute FRM candidate. He has advised MSMEs on working capital structures and credit access across public sector, private sector, and NBFC lending environments, and is the founder of Bankopedia (bankopedia.co.in) — a financial knowledge platform for banking and MSME finance professionals.